TBL Weekly #180: US Treasury & The Fed, Labor Market, and LiquidityReviewing the latest QRA, labor market prints this week, and TBL Liquidity

You can also get access to our charts and data inside our TBL Pulse Dashboard:

Dear Readers, Before we get into our latest TBL Liquidity analysis at the end of this article, let’s start with what happened in markets this past week. US Treasury DepartmentTreasury Secretary Scott Bessent has taken the market spotlight once again after his involvement in FX markets last week. This week, we had the Quarterly Refunding Announcement (QRA). US rates analysts were closely watching for three things: (1) Changes in Treasury’s forward guidance language, (2) revisions on spending for Q3 given net negative tariff collections + higher defense spending, and (3) borrowing expectations for Q4. First, on forward guidance matters, many were closely watching for changes in the language of coupon issuance. Specifically, in recent QRA announcements, the Treasury has maintained that it will keep nominal coupon and FRN auction sizes as they are “for the next several quarters.” The sentence did not change this time around. Per the QRA, the Treasury “anticipates maintaining nominal coupon and FRN auction sizes for at least the next several quarters.” Given current market conditions, I don’t necessarily believe this surprised anyone. There’s still plenty of T-Bill demand out there (from money market funds as well as the Fed’s own MBS reinvestment into Bills), and coupon yields aren’t looking too pretty right now:

There was, however, one sentence that changed. Back in May’s QRA, the Treasury wrote:

This time around, it wrote:

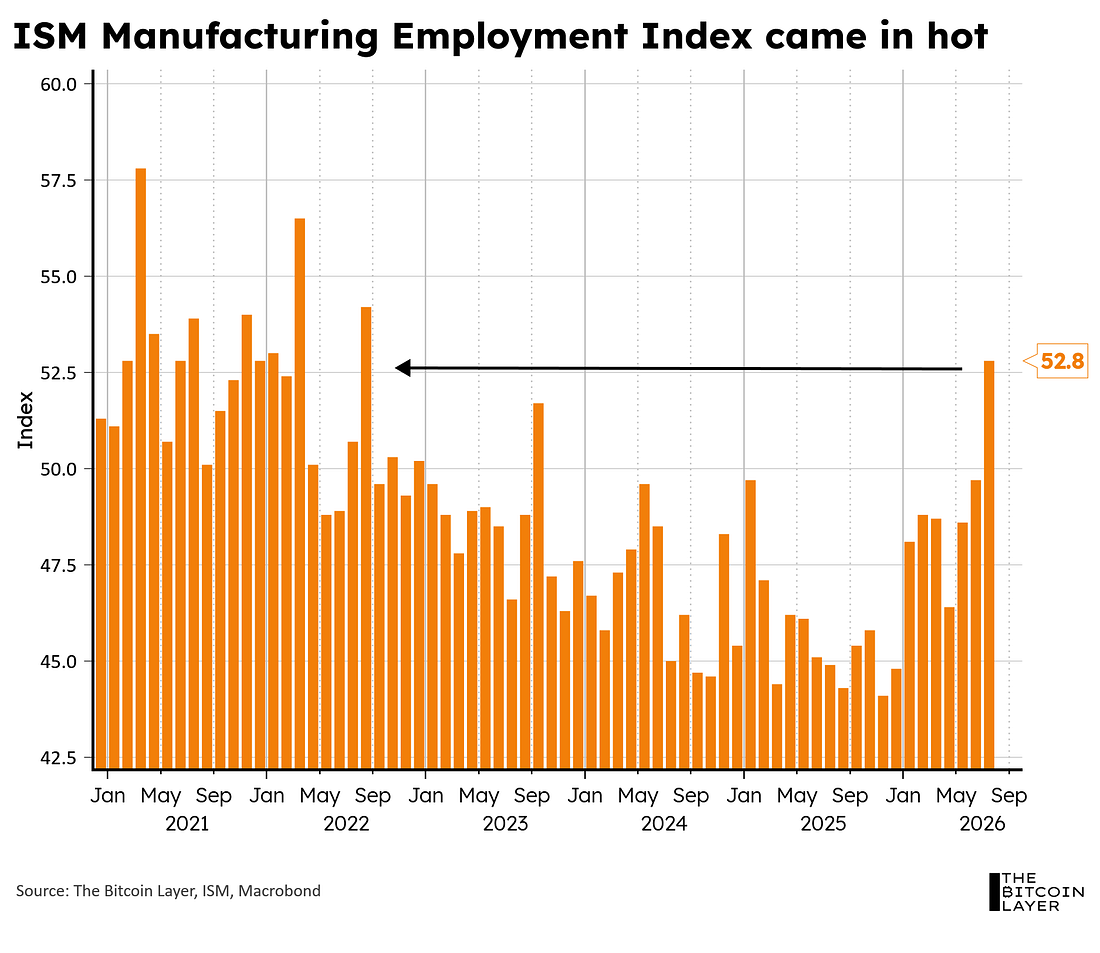

A slight wording change from “increases” to “changes” is dovish forward guidance. Taming volatility and fears of higher rates. Second, the Treasury raised its borrowing expectations for Q3 from $671B to $739B (+$68B from their May Q3 estimate), assuming an end-of-September cash balance of some $950B. This increase was “due to lower projected cash flows.” Third, it expects to borrow $628B during Q4 this year. The takeaways here are that none of this is all that surprising; from the US Treasury side, we shouldn’t expect market-moving events any time soon. Their forward guidance made this clear. Incoming midterm elections warrant more caution around Treasury markets. “T-Bill and chill” is the adage going around right now. The one thing to look out for is, of course, the fact that leaning so heavily on the Bill market raises the sensitivity of financing costs to short-term rates; this, in a time where everyone is screaming that the Fed will go (hike) at some point this year given inflation worries. The Fed and The US EconomyAs I wrote last week, I’m in the camp of no hikes this year. My base case is that, despite sticky inflation, it takes but a few bad labor data prints to shift the Fed’s focus back to the two sides of the dual mandate. Manufacturing employment has been on a tear since April, clawing its way back into expansionary territory in July, and at its highest level since August 2022:

The six largest manufacturing industries in the US are Chemical Products, Transportation and Equipment, Computer and Electronic Products, Food Beverage & Tobacco, Machinery, and Petroleum & Coal. Here’s what ISM wrote about its latest employment print in manufacturing:

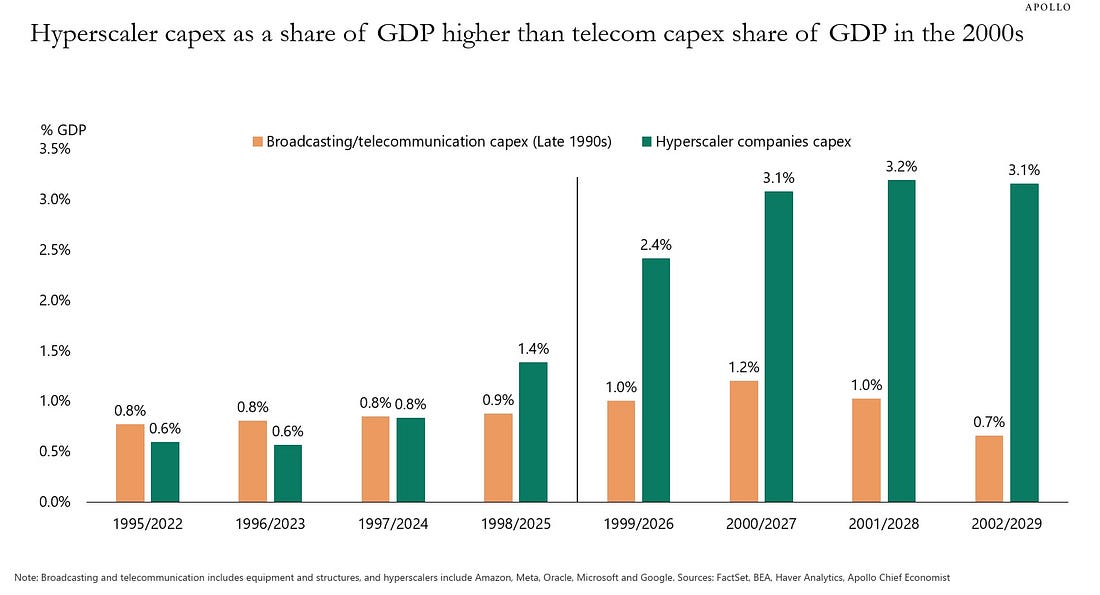

Three of America’s big six industries in manufacturing expanded employment this past month. Overall, a decent print for the US economy. And a decent fundamental print for the narrative that AI CapEx investment has been expansionary for the US economy, with computer & electronics, as well as electrical equipment, appliances, & components growing. Chief Economist at Apollo Global Management shows that current AI investment expectations are “more than twice the peak of the telecom and fiber buildout of the late 1990s.”

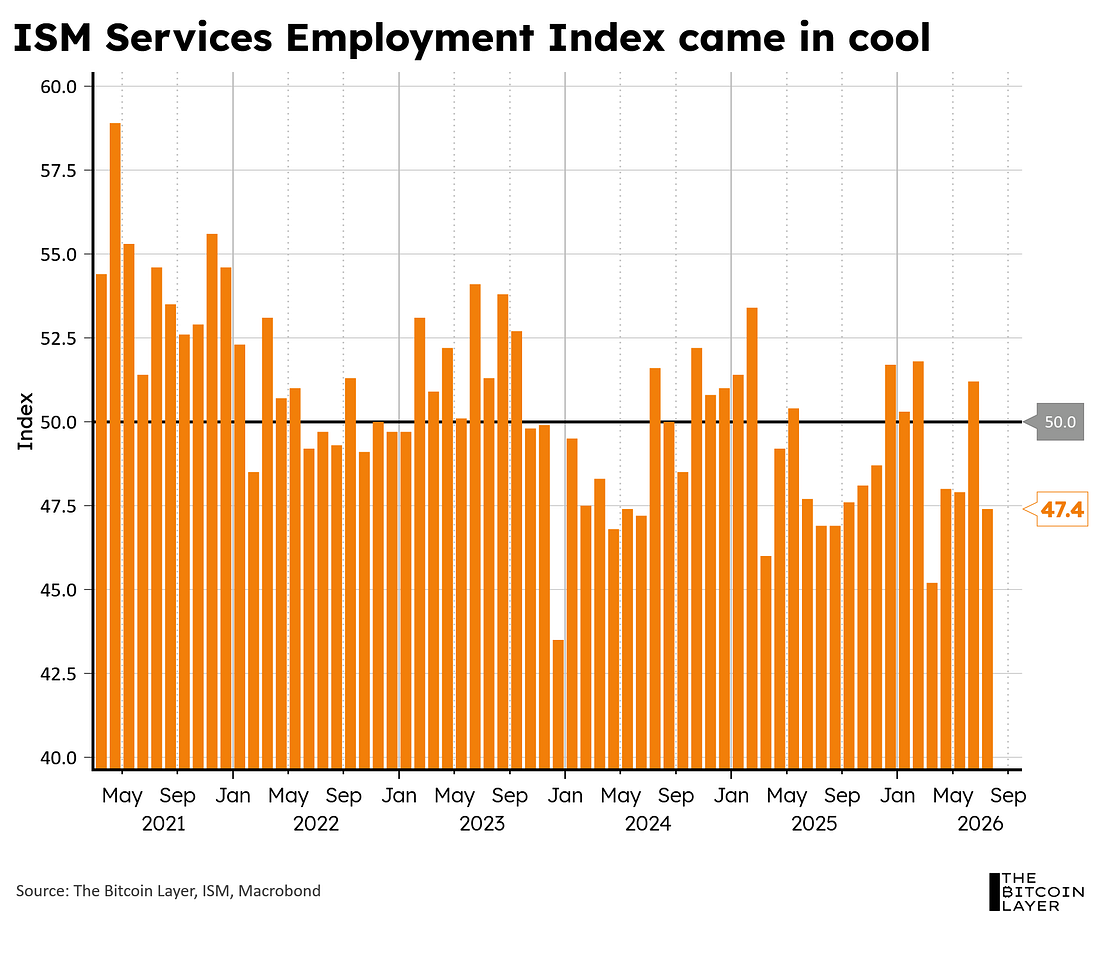

This is surely additive to the US’s job outlook in manufacturing. The caveat is that services is a much larger sector in the US than manufacturing. And this past month, services employment contracted. As per most of 2026, services employment is once again below 50:

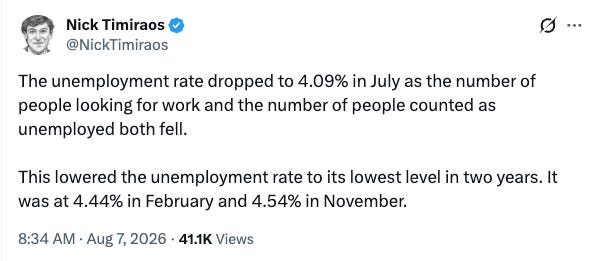

** Here’s what ISM wrote about its latest employment print in services, in case you’re curious about sectors. Where am I going with this? With more industries in the services sector showing employment contraction, there is a case to be made for a resumption of the early-2026 worries of an employment slowdown. Of course, one data print for one month in 2026 shouldn’t paint the entire picture, but it’s the regression below 50 in ISM services employment that I am addressing here. Is AI investment enough to outweigh the negative employment trend in services? I wouldn’t bet against it, but if you’re a US rates watcher, you cannot be certain that AI CapEx will carry the team here. If the Fed was truly going this year, you’d expect markets to be pricing in hikes quicker (as one 25bps hike will hardly do much to inflation). Price is truth. Markets (and the Fed) need more labor prints. And yes, despite the fact that July’s unemployment rate came in lower than expected on Friday (Act. 4.1% versus Exp. 4.2%), the overall print was bearish given 103,000 downward revisions in jobs added over the past two months. Personally, I was expecting a more bearish print in the unemployment rate on Friday, given ISM services employment this past month. That said, the lower-than-expected unemployment rate must be taken with a grain of salt, as Nick Timiraos puts it here:

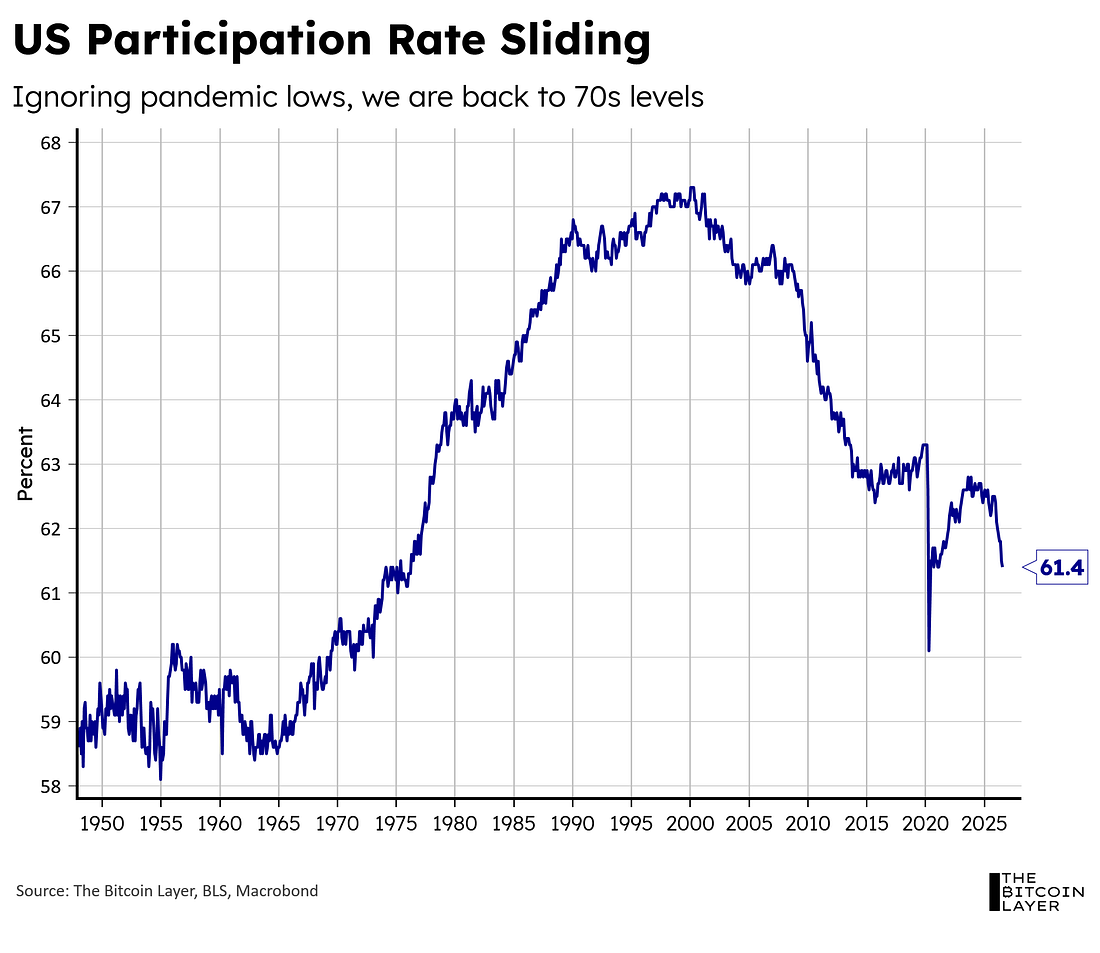

The participation rate simply continues to slide lower, which can strengthen the unemployment rate calculation, even in a labor market slowdown:

And no, I am not saying the US economy and the labor market are both in shambles…or that the Dark Ages are coming (that one’s for Nik)…but I am saying that investors can’t be too certain about inflation dominating both the Fed and yields right now…and price action in yields showed that on Friday. TBL Liquidity ComponentsThis past week, we sent TBL Pros an update regarding a small data bug we found. We have since fixed the issue, and here’s where TBL Liquidity stands today. Let’s break it down by components: MOVE IndexOur TBL Liquidity Index is built looking back at components over a one-year period. Looking at MOVE over the past year, it is lower than it was last August (chart below), which is slightly helping TBL Liquidity:

However, the overall MOVE index has been pretty much consolidating over the past year (vol suppression has been working). US DollarDespite weakness in the dollar, it is still 1.03% higher than where it was a year ago:

Our data correction earlier this week changed what our TBL Liquidity Indicator was signalling, but the correction hasn’t changed our narrative on a weaker dollar helping Liquidity. The latest drop back below 100 in DXY is the culprit for why our indicator has been trending upward lately towards a Green Dot (chart below):

US TreasuriesAdmittedly, my bullish outlook on USTs (given labor market pressures) hasn’t exactly come into fruition (chart below), which is another factor for why our Indicator is still in a Red Dot:

But should the narrative hold, and US Treasuries strengthen soon on labor market issues (as they did on Friday), we would paradoxically end up in a Liquidity-positive environment (weak labor market = stronger UST collateral = strong Liquidity tailwinds for markets …I love this job…it sometimes makes me say paradoxical things that make no sense for the average Joe, but perfect sense for a market watcher). Last note: these three components are exactly why we’ve been closely watching Bessent, the US Treasury Department, the Fed, and the dollar. These bigger macro factors quite literally help us explain TBL Liquidity and our expectations of where it is going. Substack This Week

YouTube This Week

For Podcast ListenersHere are the links to our latest episode: SPOTIFY

APPLE

Our videos are on major podcast platforms—take us with you on the go! Keep up with The Bitcoin Layer by following our social media! Disclaimer The TBL Model Portfolio, TBL Liquidity Indicator, and all TBL research outputs reflect Nik Bhatia and team’s analytical positioning for the macro and bitcoin environment. They are published for educational purposes only and are not investment advice, not a solicitation to buy or sell securities, and not a recommendation tailored to any individual’s portfolio. The Bitcoin Layer is not a registered investment advisor and does not manage client money. Please consult a professional financial advisor and conduct independent due diligence before making investment decisions. Thanks for reading The Bitcoin Layer — for access to all content, upgrade to paid!

|

Saturday, August 8, 2026

TBL Weekly #180: US Treasury & The Fed, Labor Market, and Liquidity

Subscribe to:

Posts (Atom)

Popular Posts

-

Diverging signals across credit markets, equities, and on-chain data suggest Bitcoin may be entering a new phase. ͏ ͏ ͏ ͏ ...

-

Bitcoin failed at the 200-day moving average as rising yields pressured rate-sensitive assets. ͏ ͏ ͏ ͏ ͏ ͏ ...

-

Ten European banks launch a jointly owned settlement network; SoFiUSD goes live in commercial payments; and a card issuer's collaps...

-

Dear Readers, ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ...

-

gm Bankless Nation, America's regulatory regime has spent too long fighting crypto and not enough time embracing how it can im...