Welcome to TBL Weekly #98—the free weekly newsletter that keeps you in the know across bitcoin, rates, risk, and macro. Grab a coffee, and let’s dive in.

River is our Bitcoin exchange of choice. Securely buy Bitcoin with zero fees on recurring orders, have peace of mind thanks to their 1:1 full reserve multisig cold storage custody, and withdraw at any time. Need help? They have US-based phone support for all clients. Now introducing River Link 🔗allowing you to send Bitcoin over a text message that can be claimed to any wallet. Give a gift, pay a friend for dinner, or orange pill your friends, completely hassle-free. Use River.com/TBL to get up to $100 when you sign up and buy Bitcoin. The S&P 500 has achieved its highest daily close of all time for 5 sessions in a row. A full week of advancing higher every single day, moving up 90 points on a week that had no earnings. We are in a bull market, plain and simple. Denying it now has only lost people money, a whole lot of money. The summer analyst at JPMorgan who called for 4200 SPX by the end of the year back in April (at the absolute local bottom) definitely got fired:

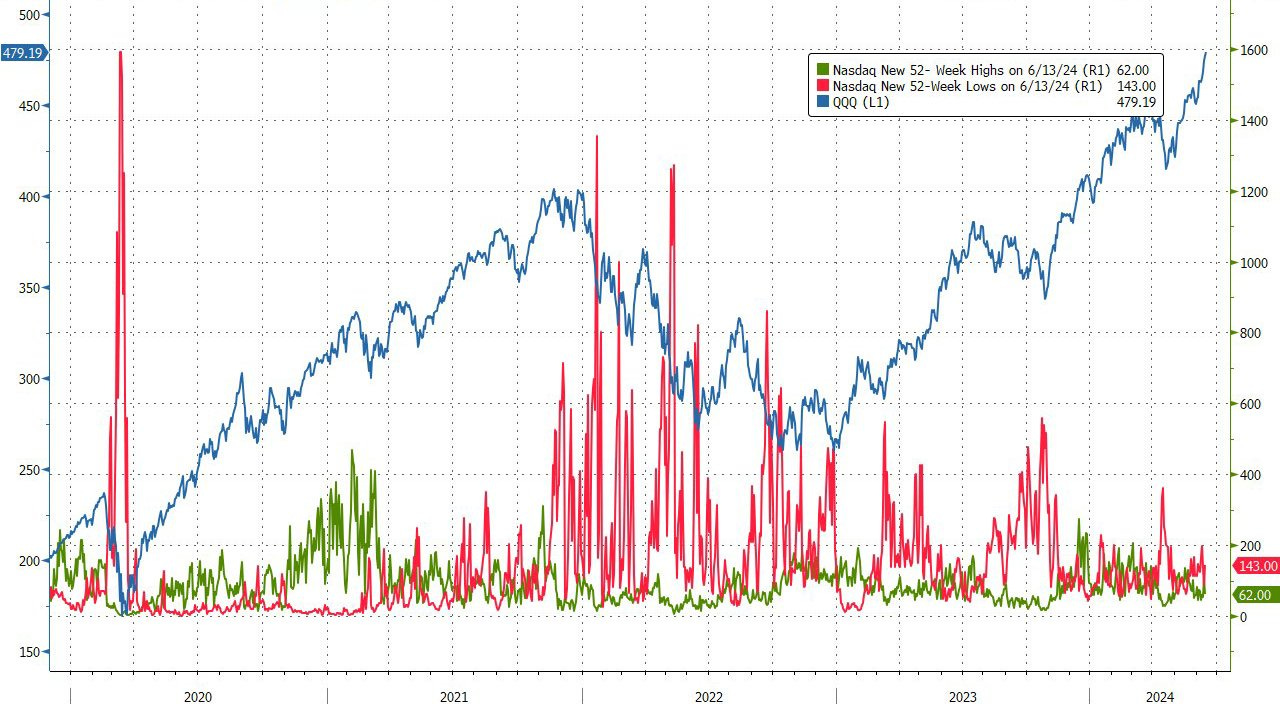

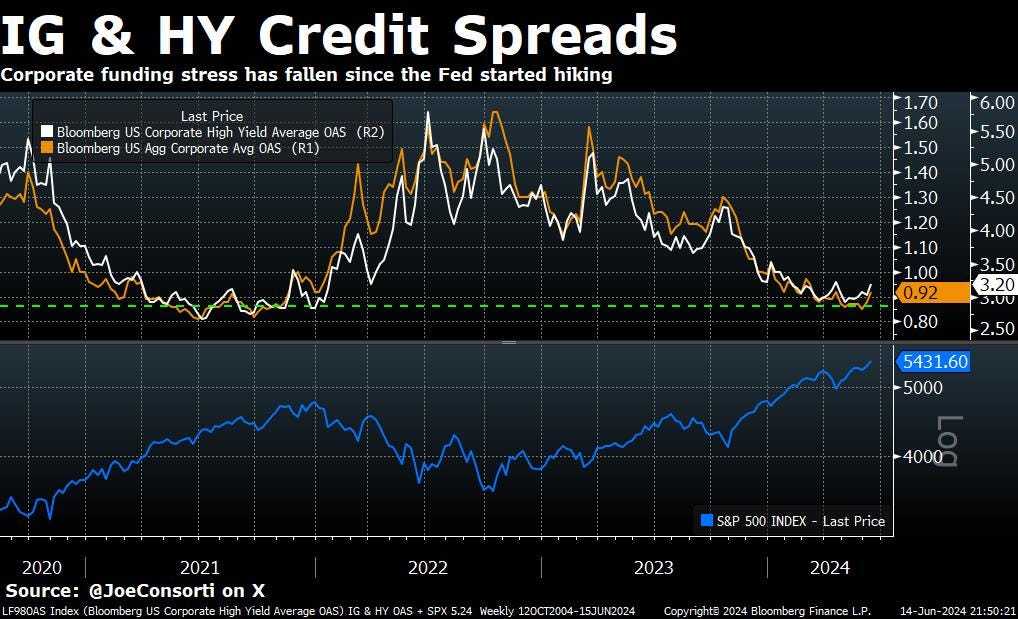

That’s not to say that certain developments don’t give me pause—there are absolutely signs of overextension if you look close enough. And they are becoming more readily available. At TBL, we don’t construct narratives before we read the tape, we take the data as it comes and translate the story it is painting for you, the reader. Where you once needed to search and grasp at straws to find signs of a market top, early signs of overextension are now visible by taking an impartial, tertiary look at the data. The Nasdaq is being dragged up by a smaller and smaller basket of names as the months go by. The Nasdaq advances/declines index adds the advancing stock market caps and subtracts the declining stock market caps to tell us how top-heavy the index is. While this has no predictive power for expected forward returns, it indicates that more companies are struggling, fewer companies are still doing well, and the ones that are doing well are huge companies who are less interest-rate sensitive: Here’s another view of the increasingly top-heavy stock market. The Nasdaq, like the aforementioned S&P 500, hit new all-time highs every day this week despite 72% of Nasdaq stocks closing red, and twice as many stocks hitting new lows than new highs. Big firms who rely less on debt are doing well, and small firms who are in scaling mode and rely on loans and lines of credit are getting pummeled: Taking a look at spreads, and it is starting to confirm the same dynamic. Corporate lending standards are finally tightening up, albeit at the margin, from their cycle tights, for both investment-grade and high-yield (riskier) borrowers. A teeny tiny move for now, but the start of what could become a cyclical reversal to tighter corporate credit—which means the slowing in the labor market will eventually accelerate, unemployment will eventually rise off its bottom, and the economy will contract. We are not there yet, but this could very well be the cycle shift we’ve had an eye on:

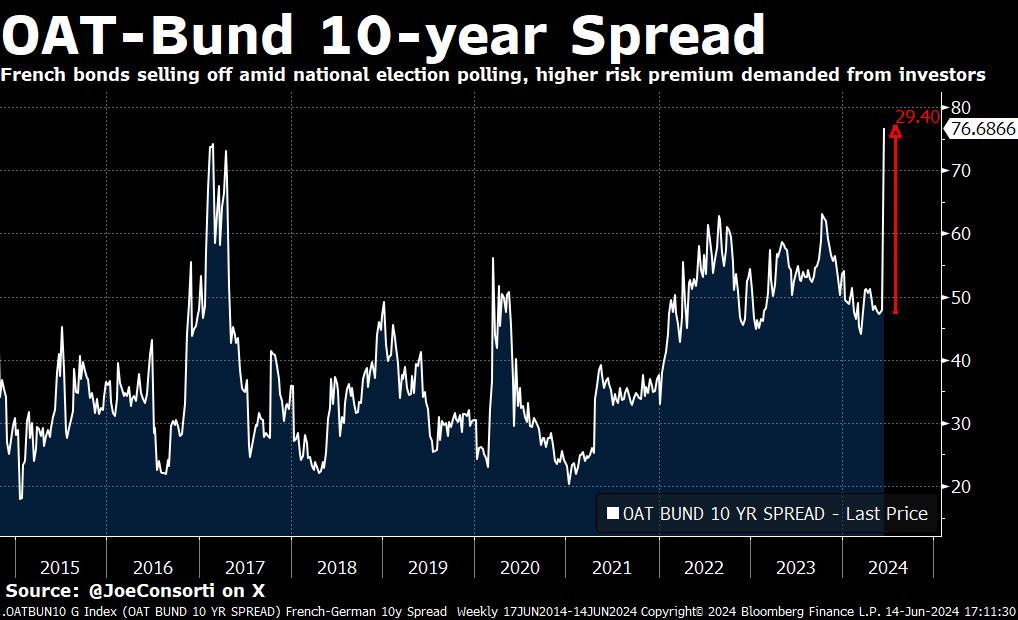

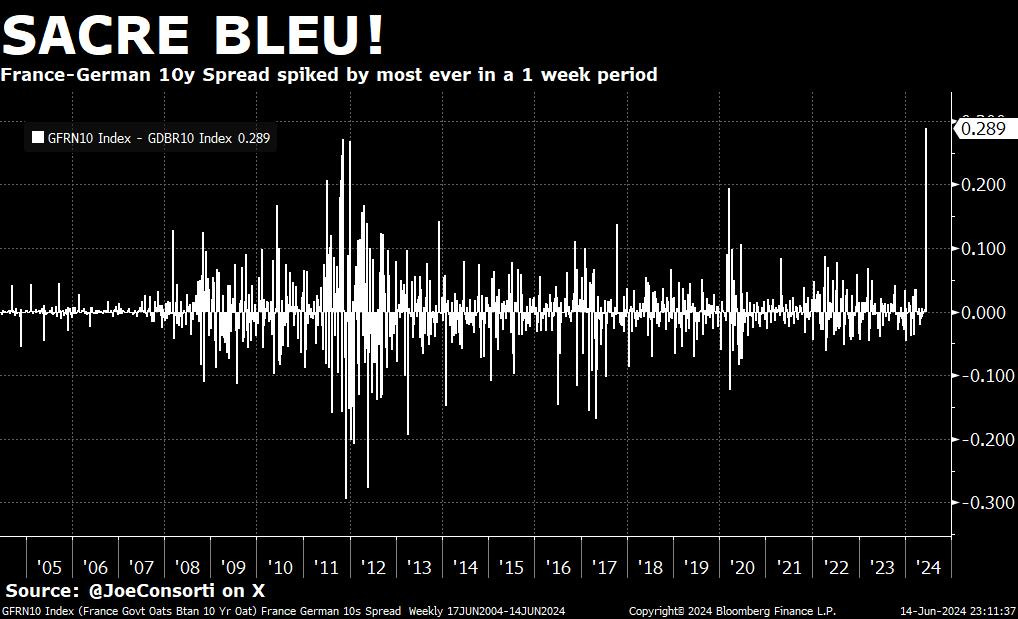

The France-Germany yield spread, a risk gauge for French government debt, widened 29 bps to 77 bps this week—the biggest jump on record for a single week. This gave the markets echoes the of the PIIGS (Portugal, Ireland, Italy, Greece, and Spain) bond panic over a decade ago. A higher risk premium is being demanded from investors of French government bonds after Emmanuel Macron called a snap election amid plummeting polls and an embarrassing showing for his party in EU elections. That is why this spread is blowing out: French government bond risk premium is rising relative to its safer German bund counterpart. French investors are faced with potential tax cuts that might decrease the sanctity of OATs (French Treasuries):

Moves of this magnitude generally don’t precede sunshine and daisies. These types of volatile widenings are par for the course with high-yield corporate bonds, not sovereign debt, the highest-rated bond tranche of them all, since they are backed by a money printer to get out of dodge when things get hairy. The main problem with the French money printer is that it’s located somewhere between Brussels and Frankfurt:

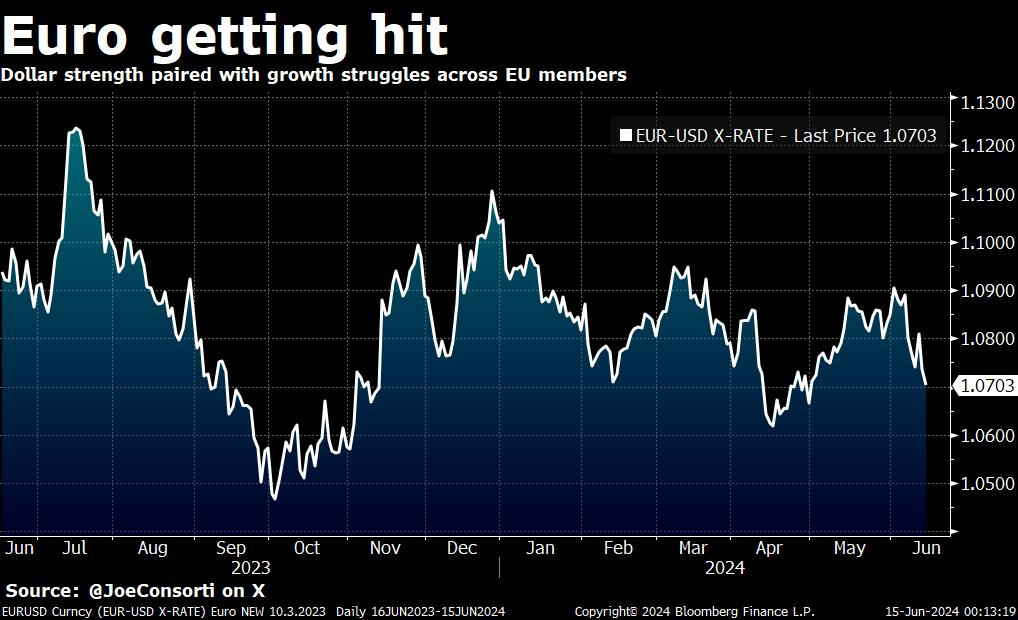

While we’re a long way off from a sovereign debt crisis, large sovereign debt levels and extremely high spending are a hot-air balloon headed for the exosphere. The pilot of the hot air balloon won’t stop fueling it, even with it so high up in the air. Know what happens when we reach the edge of the atmosphere? Nothing good: The US dollar is headed for its highest levels since last November off of the swift growth deceleration in Eurozone countries this month, and comparative strength with the Fed on hold as countries like Canada and G7 members like the Eurozone cut rates:

With the rate cut 10 days ago from Christine Lagarde and the ECB, the euro has not taken a reprieve from its nosedive that began at the start of this month when we got a slurry of bad growth data out of major member nations like Germany and France. Between its own internal economic deceleration and the dollar’s outright strength due to both interest rate differentials and comparative US economic strength, the next floor for the euro if it can’t hold the 1.07 handle, 1.05 is in play. This is a big problem for US policymakers, who don’t want to see the dollar get too strong. We can expect a weakening euro to materially factor in when the Fed ultimately decides to cut rates. It must help to prevent a very strong dollar which threatens the world economy. We wonder how long it will take for Powell to mention global conditions in a press conference—for now, the Fed chair cannot appear to focus on anything besides American cost of living increases:

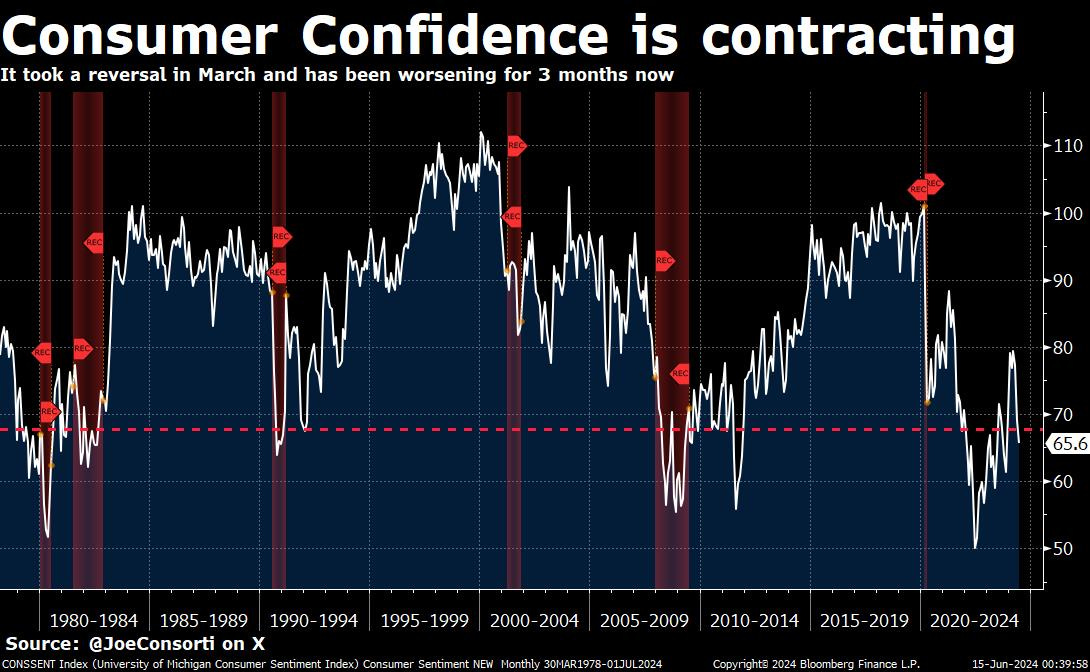

And finally, the advance consumer survey data from the University of Michigan massively disappointed analyst expectations today, causing a transient rout in stocks during the morning, before they rallied and closed higher on the day, likely on falling long-term yields. Consumer sentiment dropped from 69.1 to 65.6 in June, missing the expectation of a rise to 72:

This is yet another massive miss relative to what analysts were expecting—the frequency and magnitude of which both rise as cycles inflect into contraction. This was a 3-sigma miss, or 3 standard deviations below the mean analyst estimate. Look how far to the left of the estimate bell curve consumer sentiment came in. Consumers are weakening harder and faster than analysts are predicting: Add that to the PPI data we got on Thursday that missed analyst expectations by a pretty wide margin—in line with Wednesday’s CPI data that was also cool:

Taking it all into account, rates are reflecting cooling prices, consumer sentiment on the decline, and a growth story that is rocky at best, if not reflecting downward. Tens had their first close below a trendline that has been intact for 2.5 years—down from 450 to 422 bps in 2 weeks. Heading even lower? If data keeps coming in as it is now, looks like it:

Next Week with NikIn the week ahead, markets will focus on exactly what Joe wrote about—the slowing consumer. Tuesday brings the monthly retail sales data that shocked us last month by contracting 0.3% for the control group. Expectations are for a strong rebound to 0.4% growth, but we are certain that a material miss as what happened with University of Michigan and PPI will further the Treasury rally. Severe anxiety is palpable from bond bears of late—completely silent are the folks ranting about too much Treasury supply, replaced by a growing chorus of analysts telling the Fed to just get on with rate cuts already. We certainly have sympathy for the argument that inflation is stuck well above 3% which should demand continued tighter conditions. However, I can’t help but draw on my experience of watching the Fed completely pivot on its mandate when markets demand it, such as what might happen over the coming months with dollar strength. A dollar wrecking ball will immediately cause the Fed to stutter over its desire to bring inflation to 2%, leading to rate cuts that might boost stocks and prevent prices from coming back down. The Fed is leaning on the economy weakening, though, as it has, to subdue inflation. Producer prices back in contraction give us a sign that restrictive policy is working, despite other more stubborn inflation readings. Finally, jobless claims data from last week caught our eye, bringing the weekly Thursday data print back into focus. Earlier this week, Powell curiously admitted the BLS is fudging jobs data. Immediately after, initial claims, which were practically pegged at 215,000 since January, spiked to 242,000. Does this mean the BLS has to stop its “magic adjustments” for other corners of labor market data? Does the Fed need more justification for the labor market to cut by September? These are the questions we’ll be asking ourselves as markets open back up on Monday. We’ll stick with our call for a September cut for now, mostly because market yields are telling us one is likely—10 and 30-year Treasury auctions went very well this week, and Treasury bulls are indeed back.

If you’re enjoying today’s analysis, consider supporting us by becoming a paid subscriber. As a paid subscriber, you get full access to all research as it drops. Here are some quick links to all the TBL content you may have missed this week: MondayIn this episode, Nik delivers a full explainer on Treasury money printing and the monetization of T-bills by banks. In another follow up episode to the recent series on Michael Howell's liquidity framework, we walk through examples of how the Treasury creates money when it borrows and spend, and compare that to the primary dealer financing of Treasuries via repo investments from money market funds (MMFs). Check out—MONEY PRINTING 101: Banks Print Money To FUND The Deficit  WednesdayIn this episode, Joe walks through an action-packed day in macro. The CPI print for last month came in cooler than analyst estimates, led by the shelter component which saw its first monthly decline in 3 years. Following the cool CPI data, rate expectations fell and risk assets popped, but Powell was quick to temper dovish hopes with his press conference in the afternoon. Though the Fed is content with the path of inflation, it is not satisfied with the level still being well above its 2% target. It remains flexible, with its eye on developments in the labor market, into the end of the year. Joe wraps by talking about how asset prices will behave heading into the end of the year. Check out—Macro Update: CPI Cools, Shelter Inflation Tanks & Fed DELAYS Cuts  ThursdayGreetings from Alaska! On the flight up from Los Angeles, I cracked open the 1986 book recommended to me by our liquidity mentor Michael Howell—Interest Rates, the Markets, and the New Financial World by Howell’s own mentor Henry Kaufman. Kaufman worked in banking, then for the Fed, then became partner at the investment bank Salomon Brothers. While essentially finished with my research for book 2 (aiming for a Fall 2024 release), I was hesitant to start another book that might influence my book writing, but in the end I couldn’t help it. Readers know that I’m in the process of deconstructing Howell’s liquidity model for our own and your benefit, so I figured a book by his mentor should be good enough. I’ll leave you with this thought before we cover yesterday’s inflation report and Fed decision, only to revisit it before we conclude today’s letter. It felt surreally important given the recent wave of excitement surrounding replacing the current administration with a more bitcoin-friendly one:

Check out—Powell pumps stocks and admits government lies about jobs data

FridayIn this episode, Joe sits down with Drew Armstrong, president and chairman of Cathedra Bitcoin, a publicly traded bitcoin miner on the Canadian Stock Exchange. Drew takes Joe through a mining masterclass. They discuss how mining public companies raise money, how the landscape is evolving, hashprice, hash rate migrating from the US, how miners are consolidating, and how L2s, Runes, and other things demanding bitcoin blockspace accelerate the development of scaling solutions so that bitcoin fulfills its chief function: better money. Check out—Bitcoin Mining MASTERCLASS: Miner Revenue, Economics, & Integrating AI with Drew Armstrong  Our videos are on major podcast platforms—take us with you on the go! Keep up with The Bitcoin Layer by following our social media! That’s all for our markets recap—have a great weekend, everyone!

River is our Bitcoin exchange of choice. Securely buy Bitcoin with zero fees on recurring orders, have peace of mind thanks to their 1:1 full reserve multisig cold storage custody, and withdraw at any time. Need help? They have US-based phone support for all clients. Now introducing River Link 🔗allowing you to send Bitcoin over a text message that can be claimed to any wallet. Give a gift, pay a friend for dinner, or orange pill your friends, completely hassle-free. Use River.com/TBL to get up to $100 when you sign up and buy Bitcoin. Thanks for reading The Bitcoin Layer — for access to all content, upgrade to paid!

|

Saturday, June 15, 2024

Bull Market Raging, EU Sovereign Debt Worries, Consumer Confidence Plummets: TBL Weekly #98

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment