The Labor Market Is "Hot" & Rate Cut Bets Are Falling...Huh?: TBL Weekly #97Don't worry, there's a reason for it.Welcome to TBL Weekly #97—the free weekly newsletter that keeps you in the know across bitcoin, rates, risk, and macro. Grab a coffee, and let’s dive in.

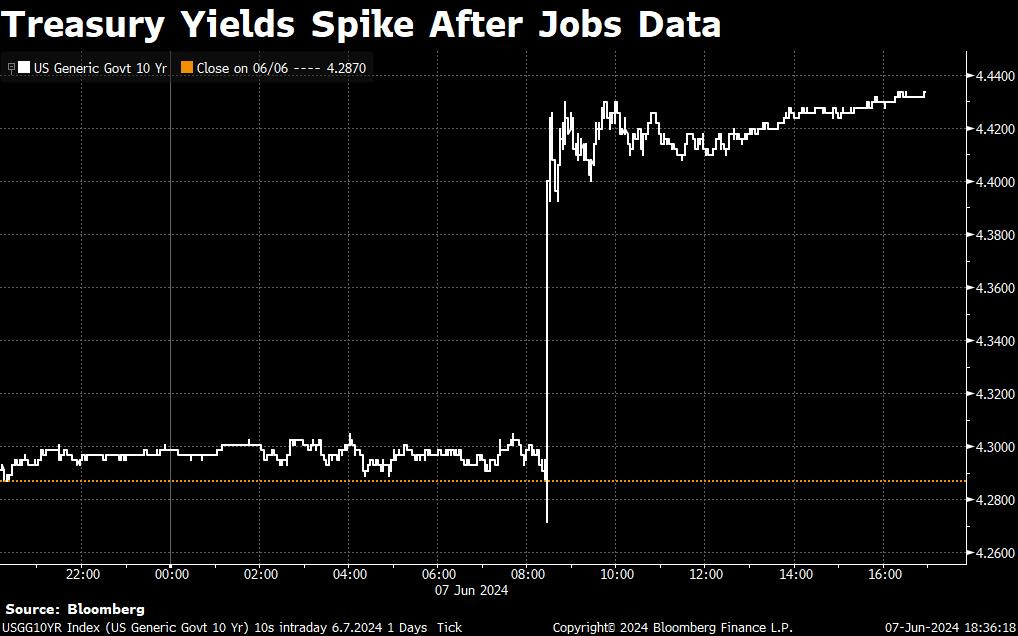

River is our Bitcoin exchange of choice. Securely buy Bitcoin with zero fees on recurring orders, have peace of mind thanks to their 1:1 full reserve multisig cold storage custody, and withdraw at any time. Need help? They have US-based phone support for all clients. Now introducing River Link 🔗allowing you to send Bitcoin over a text message that can be claimed to any wallet. Give a gift, pay a friend for dinner, or orange pill your friends, completely hassle-free. Use River.com/TBL to get up to $100 when you sign up and buy Bitcoin. Good morning TBL Readers, happy Saturday ☕ We had quite the mix of economic data this week. At the front of the week, we had disappointing ISM manufacturing and services data that signaled prices cooling and employment finally taking a nosedive, and JOLTS data that showed job openings massively disappointing by almost half a million fewer positions than the month prior. Then the establishment data released on Friday morning told a completely different story for the labor market, one where payrolls massively beat to the upside by almost 100,000 positions to 272,000 new payrolls added last month, and average hourly earnings rose 4.1%. What on earth is going on here? Well, at the very least, the establishment survey and the household survey have never been more disparate. The jobs report has gotten increasingly ridiculous as the years have gone by, and the massive detachment of the establishment data from what people are actually reporting in their own work-life has really never been this different. Deceptive headlines are what matter, and we’ve seen just how prominent a fixture they have become in the U.S. government’s framing of the economy. You can always revise the prior release down after the fact once the headlines about economic might have been printed. One tweet summed up the state of establishment data perfectly: Yields popped off of the back of the +272k payrolls data, and it was an astonishingly big move. The market is clearly throwing a lot of weight behind the establishment survey over the household survey, which we’ll get to in just a moment. Growth and inflation expectations which were choppy/trending down all week gave up half of their gains on the week with just one data release. As we’ve been saying, the Fed’s focus is firmly on the labor market rather than CPI:

A 20-basis-point downward move in 10s was reversed to a 6-bps decline on the week after the NFP pop. Look at how huge the move all across the curve was, with the very front-end flat on the week as expectations are for an on-hold Fed in the face of mixed labor market data:

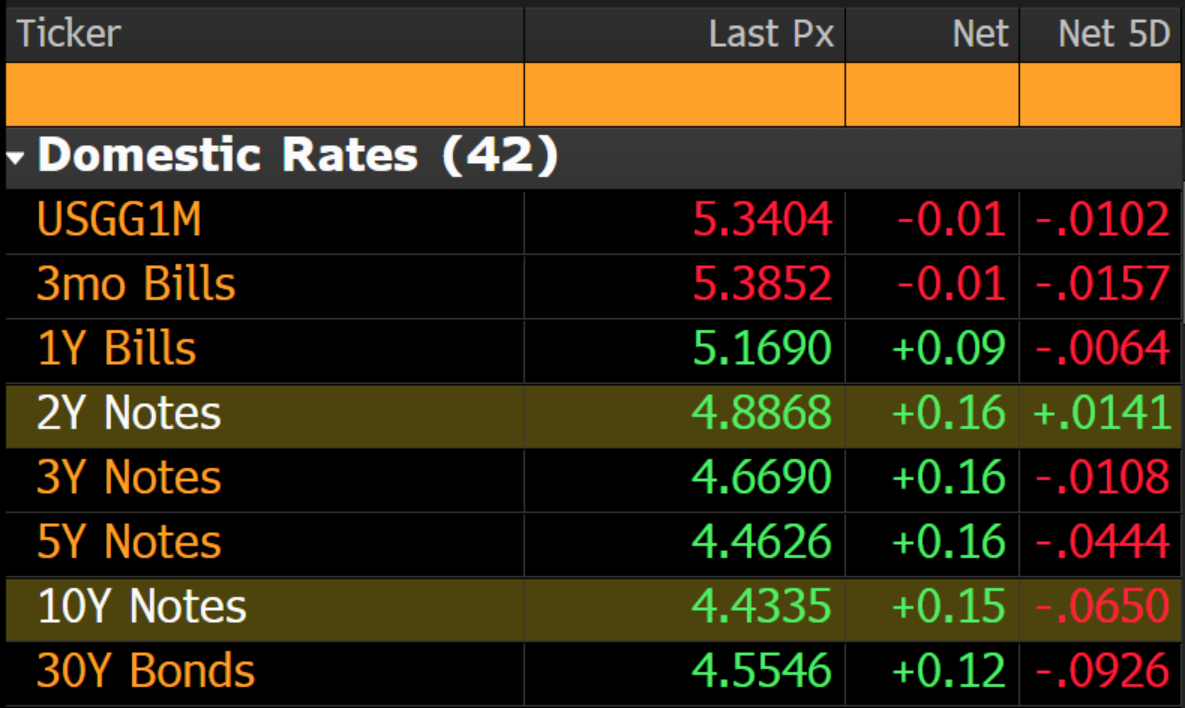

Look at the move in 2s. Just two days ago we were highlighting how the Fed, following Europe and Canada, would be one of the next in line for the G7 nations to begin maintenance rate cuts given the global trend of weakening growth and activity in the labor market. Expectations for cut #1 were moved from December to September, and then right back to December, all in one fell swoop. Sensitivity to only a handful of prints is now very high. This market moves on a dime:

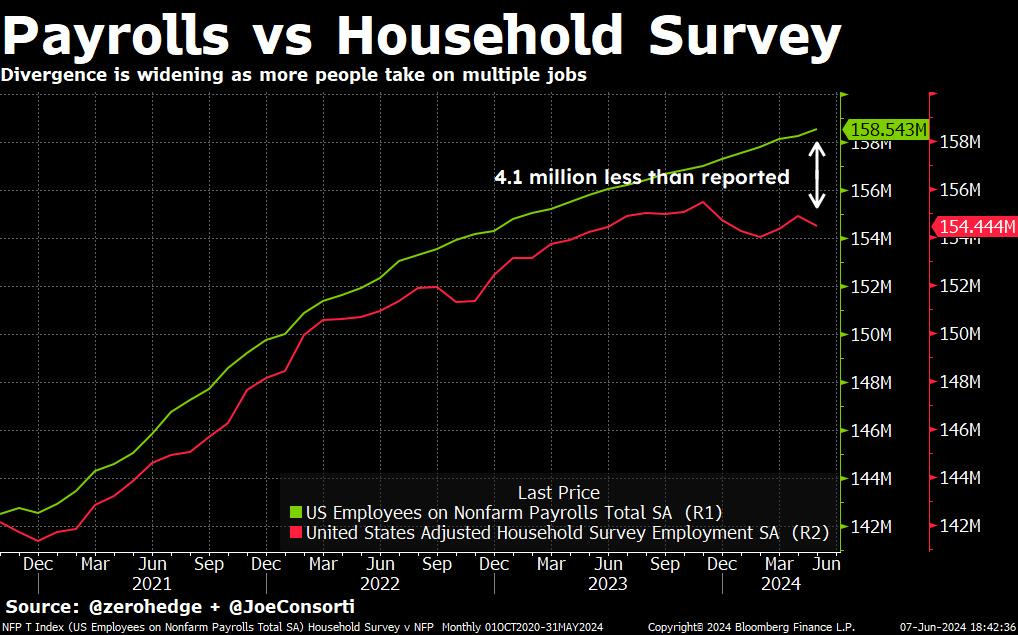

The establishment payrolls data is in green and the household survey is in red. Note the divergence between the two. Actual jobs as surveyed by households, who are the ones actually working said jobs, are at 154.4 million, compared to the establishment’s 158.54 million number. The household survey was down 408k this month. Not a single headline. That is a divergence of 4.1 million fewer jobs actually being worked than what is reported by the BLS, the widest gap it has ever been:

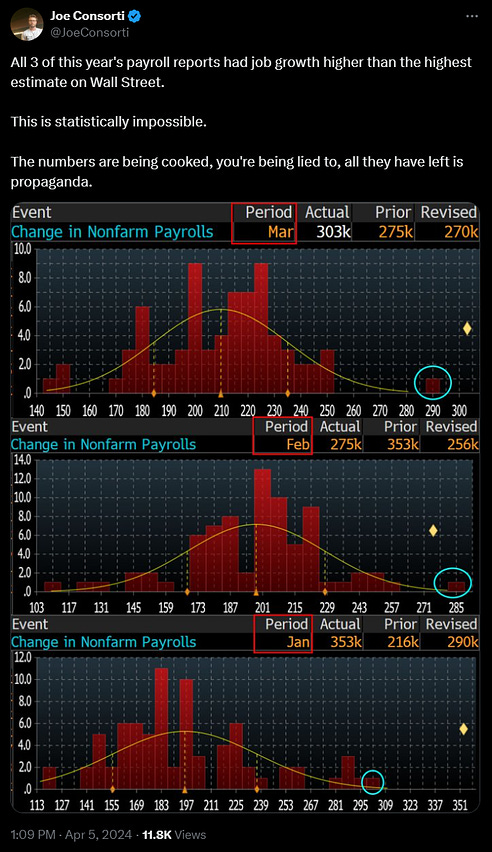

Despite payrolls as measured by the establishment data was an absolute blowout, the unemployment rate rose from 3.9% to 4% over the same period. The unemployment rate is based on the Household Survey, which measures the labor force status of individuals. In contrast, the nonfarm payroll figures come from the Establishment Survey, which counts jobs from employers' payrolls. These two surveys can sometimes show different trends. You can see it in the divergence. Though the market lends more weight to NFP, since it is what the Fed uses to inform its monetary policy decisions, the unemployment rate is derived from the household survey, where people are reporting stagnating or fewer jobs. The revisions for the NFP data were once again comically large. Remember the strategy: overestimate to a laughable degree for good headlines about a ‘red hot labor market that continues to beat analysts estimates’ and adjust to the real number one month later. Here’s what we got for revisions this time around:

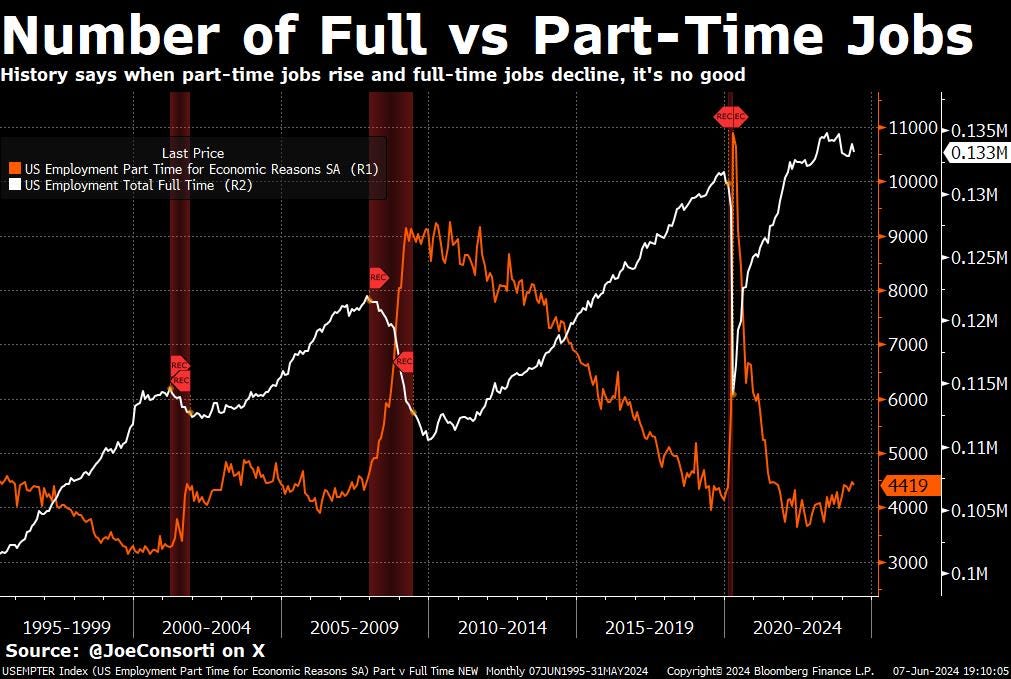

Like I tweeted two months ago, beating even the highest analyst estimate this often and this consistently is statistically impossible. The numbers are cooked for the sake of headlines, don’t be fooled. That’s not to say the labor market is on its deathbed, it isn’t. Simply that they’ve cushioned the blow of fear by overestimating at every turn, and it is increasingly blowing up in their faces as Americans grow embittered with an establishment that they know is lying to them yet does it anyway: Full-time jobs are topping out and heading down while part-time jobs are rising.

History tells us this signals a forthcoming recession. Look at 2000, 2008, and 2019 when the white line began inflecting down and the orange line began inflecting up; recession was declared (after the fact) soon after this event occurred. As far as timing goes? That's anyone's guess. This cycle has been defined by the word ‘elongated’, and that would be my best estimate of when we may see a recession as defined by two consecutive quarters of negative GDP growth, despite this indicator flashing red:

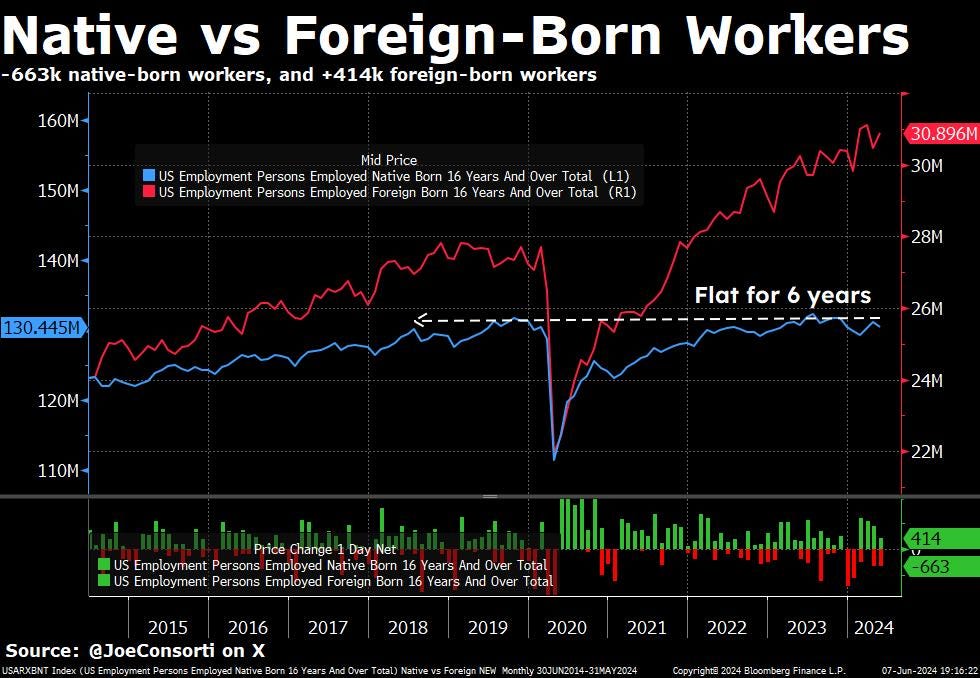

The awful trend continues. In May, 414k foreign-born workers gained a job while 663k native-born workers lost a job. There have been zero net new jobs for native-born workers since July 2018, six years ago. TBL is not a political outlet, we are however pointing out how this has disinflationary pressure on wages and prices. As the employment component in prints like ISM Manufacturing inflects upward while Prices Paid in the same survey inflect downward, this is a factor behind why:

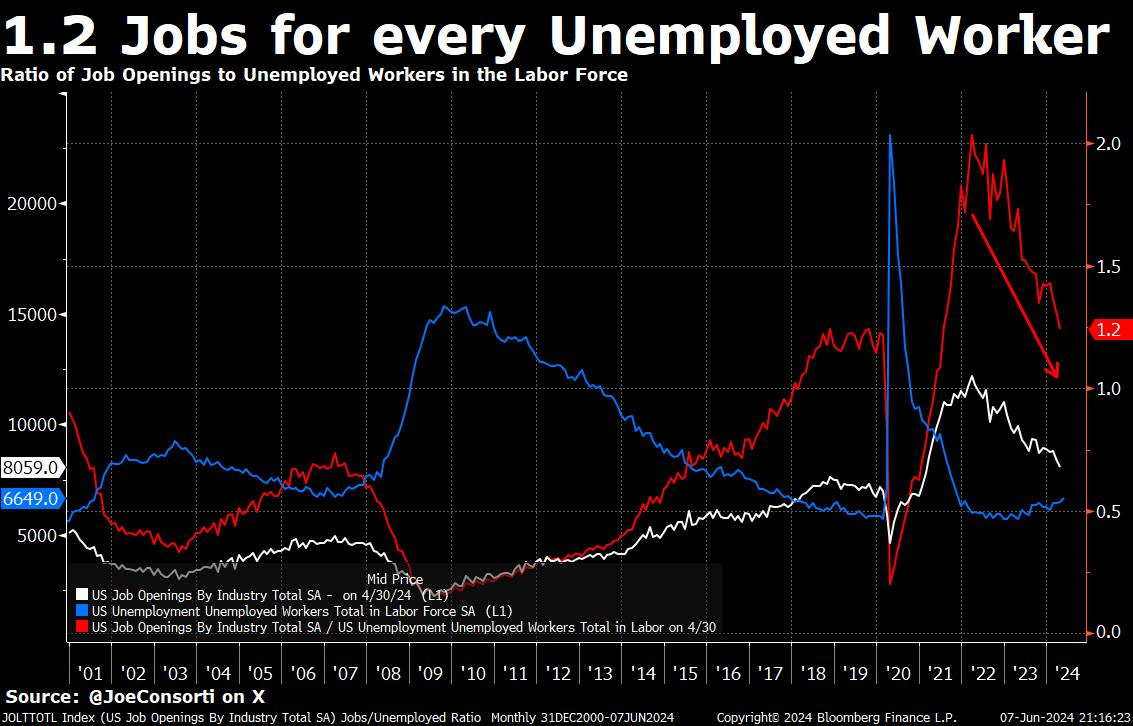

The cooling is also visible in the amount of jobs that are open for every worker who doesn’t have one. From a high of 2 jobs for every unemployed worked in 2022, a very loose labor market frothing over with opportunity, we are now back down to 1.2 jobs per every unemployed worker, close to the pre-COVID level. There is still ample opportunity out there for workers, but the gap between labor demand and labor supply is narrowing. When this flips below 1.0, we’ll have already entered recession:

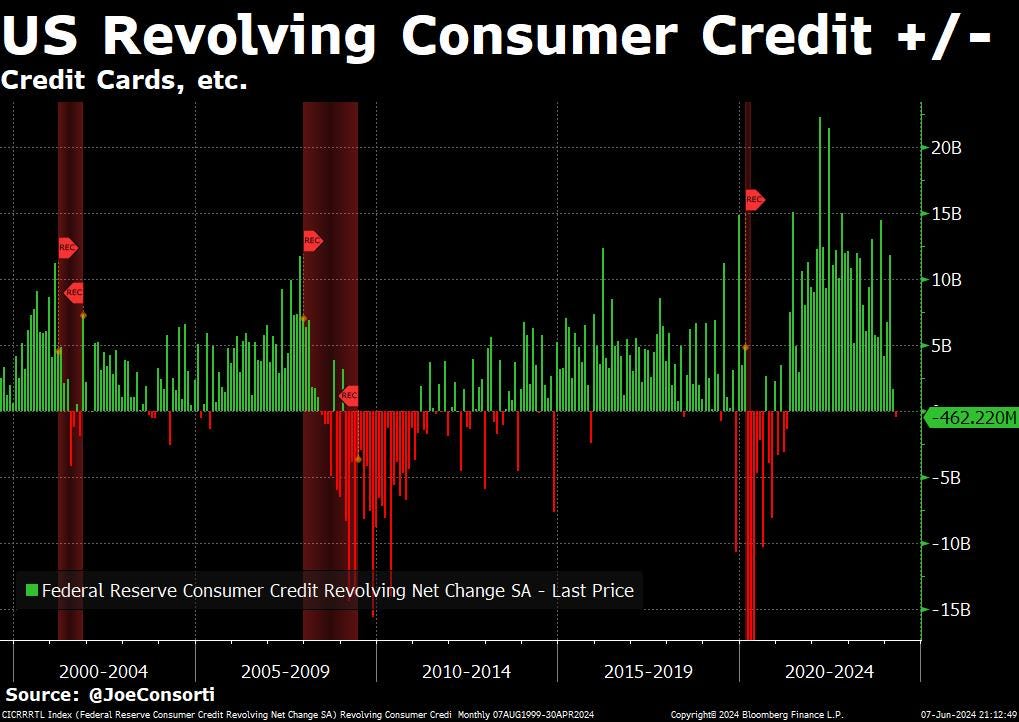

In case you want more on the messy and cooling labor market picture, Nik made a great video on Friday for you to check out now if you haven’t. Consumption continues cooling, too. Revolving consumer credit, largely credit card debt, missed at $6.2 billion in April versus $10 billion expected. March was massively revised lower from $6.3 billion to -$1.1 billion (naturally). Credit card balances shrank on an annual basis for the first time in 3 years, down $462 million in April from the year prior, or 0.4%. As we’ve seen in depleted cash savings, people turned to credit cards. Now that delinquencies are on the rise and teaser rates aren’t being handed out like free samples anymore, credit card balances are falling:

Here’s a more detailed view of daily spending per household, so you can see where people are cutting back. Look at the far-left column. Every single category of credit card spending declined from June 2023 to June 2024 except for General Merchandise, Online Retail, and Transit. The heaviest hit areas are the most discretionary areas, with Entertainment down 14% YoY, Furniture down 13.8%, and Home Improvement down 11.5%. Cutting back on what you don’t need prices cutting back on life’s necessities, and when we reach that point, we’re past the point of no return: Next Week with NikOn Wednesday, the market will receive a wealth of information that should be enough to dictate the path of front-end interest rates heading into the election. After a hot wage print yesterday, bond traders sold long positions built earlier in the week and rejected the important 4.25% area on 10s. Rocketing higher after wage data fits in with the narrative that the economy is nowhere near the slowdown needed to warrant rate cuts. That is why these cuts keep getting pushed back—traders are preparing for a recession or labor market disaster that wants to happen but statistically hasn’t materialized enough. CPI and the FOMC’s dots should give the market lots of information, but we still can’t call September away from the 50/50 chance at which it currently stands. The reason is that so much data will arrive in July and August that might make the Fed feel more comfortable to cut. What we can’t assume, however, is that the Fed will avoid action due to election timing. If the labor market starts to turn for the worse and inflation stays close to 3%, the Fed could get away with some policy rate reduction, even if it comes days before people line up to vote. As of now, we simply do not see the data that would mandate a cut. And for that reason, Wednesday’s should bring much of the same: Powell acknowledging rates have peaked for the cycle, but flat-out refusing to consider another rate hike. Maybe he saw some of the on-the-ground data from the Texas residential real estate market, or maybe he saw Joe’s charts on the heavily manipulated labor statistics. Either way, we truly believe that Powell is cautious on the economy just as we are, hence why he won’t allow for more rate hike discussions. He wants bond traders to be ready for cuts, even if he has to say “not yet” at each of the next few press conferences. We’ll also see lots of Treasury supply hit the market which will give us another opportunity to reflect on the inverted curve and just how much supply would be required to actually resteepen it. Lastly, next week brings a settlement day for Treasuries (QT) and some calendar considerations around a corporate tax deadline—this brings the potential for money market disruption as money floods into the TGA (and out of reserves, and out of money market funds which fund dealer Treasury positions). Count on us to be your repo watchers.

If you’re enjoying today’s analysis, consider supporting us by becoming a paid subscriber. As a paid subscriber, you get full access to all research as it drops. TBL Pro Subscribers: LIVE Zoom Q&A InviteIt’s time to take this research community to the next level: live Q&A sessions with you, Nik, and Joe. Subscribers already receiving our full slate of research need to do nothing other than sign up using the link below. For an extremely accessible price (about 12% of an online subscription to Wall Street Journal + Bloomberg), TBL Pro members receive exclusive research and chart packs, can personally request explainer videos and research letters, and can now participate in monthly, unedited conversations with the TBL researchers. Only TBL Pro members will have access to the Q&A recordings after the conclusion. Accordingly, we invite all of you to join the TBL community for our first live Q&A session!

You’ll find the registration to the Zoom Q&A in the post below, only available to paid subscribers (TBL Pro Members). Once you have registered, you will receive an email with the direct link to the meeting, which you can then use to join the session on June 20th, 2024. Here are some quick links to all the TBL content you may have missed this week: MondayIn this episode, Nik delivers an economic and markets update to start the trading month of June. With a weak ISM manufacturing release on Monday morning, Treasury yields and the dollar declined, the latter breaking an important trendline. Nik discusses a record in SOFR daily usage, a terrible day in crude oil prices, and looks at Redfin housing data to identify some trouble in inventories. Check out—Markets Update: BAD DATA To Kick-Off June  TuesdayBitcoin has gone through a 3-month consolidation phase in a tight range between the high $50k and low $70k range, and it finally looks primed to break out. Pending further macro data that shows a cooling off in the economy, bitcoin in and of itself looks primed to explode if this is the beginning of the bull market, which is still our belief here at TBL. Today we make the case:

Check out—Bitcoin is raring to breakout

Want to watch it in video form? Joe has you covered:  WednesdayIn this episode, Nik breaks down a Wall Street Journal opinion piece about the Fed's balance sheet. While explaining Fed policy rates, the repo market, and why wholesale repo funding is the most important component of financial plumbing, Nik describes how the Fed could use the timing of Fedwire payments as an indication of reserve scarcity. This an a very educational episode for those interested in Fed policy mechanics and monetary plumbing. Check out—Stanford Professor: Fed Is Scared Of REPO CRISIS ThursdayCanada cut rates yesterday. Europe cut rates this morning. A reader sent me a message yesterday telling me my prediction about Canada came true, but I gently reminded him that I didn’t necessarily predict it—I’m a money markets watcher. It’s my job to tell you when rate cuts and/or hikes will happen a few weeks before they occur, but I also try to get a sense with three to six months lead time. That’s why the prediction of Fed cuts by June was not necessarily wrong… just early. The move lower in global yields this week has been somewhat shocking. I am certainly surprised by its strength. It has also meant a brilliant setup for risk assets; any move lower in yields is accompanied by intensely attractive liquidity conditions for bitcoin. We have been bullish for some months and describing the current chop as simply a mid-bull consolidation. To be frank, we are ready for that consolidation to end. Eyes on $80k. Check out—Rates quick pivot, glorious bitcoin setup

FridayCheck out—TBL Thinks: Multifamily Goes Bust, Chip War Wages On It’s Thinking time. This week we cover apartment building developers’ despair amidst a financing crunch, and the latest in the global chip war. TBL Thinks is our way to summarize the most important paywalled, longer reads relevant to global macroeconomics, helping you cut through the noise. With that in mind, please enjoy.

In this episode, Nik recaps an eventful week in economic releases and bitcoin price movement. He explains the latest developments in the labor market, analyzes bitcoin fundamentals and price behavior, considers the election's impact on Treasuries, and concludes with an opinion on the state of the Fed's ample reserves framework. His ultimate conclusion is that the Fed will be forced to expand its balance sheet. Check out—Global Macro Update: Fed Will Print, Bitcoin STUCK At $70,000, Rate Cuts  Our videos are on major podcast platforms—take us with you on the go! Keep up with The Bitcoin Layer by following our social media! That’s all for our markets recap—have a great weekend, everyone!

River is our Bitcoin exchange of choice. Securely buy Bitcoin with zero fees on recurring orders, have peace of mind thanks to their 1:1 full reserve multisig cold storage custody, and withdraw at any time. Need help? They have US-based phone support for all clients. Now introducing River Link 🔗allowing you to send Bitcoin over a text message that can be claimed to any wallet. Give a gift, pay a friend for dinner, or orange pill your friends, completely hassle-free. Use River.com/TBL to get up to $100 when you sign up and buy Bitcoin. Thanks for reading The Bitcoin Layer — for access to all content, upgrade to paid!

|

Saturday, June 8, 2024

The Labor Market Is "Hot" & Rate Cut Bets Are Falling...Huh?: TBL Weekly #97

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment