For decades, finance textbooks and MBA models all started from the same place: the U.S. 10-year Treasury yield is the risk-free rate. It is the baseline for everything, the yardstick against which corporate bonds, mortgages, dividend discount models, and venture hurdle rates are measured. In times of panic, capital flies to Treasuries. They are the safest asset in the world. Jeff Park recently argued in The Radical Portfolio Times that it’s time to stop calling it “risk-free” and start calling it what it really is: the risk-full rate. Why? Because the assumptions that once underpinned Treasuries no longer hold.

As Park puts it: “When your supposedly risk-free benchmark loses purchasing power year after year, that’s not risk-free. That’s risk materializing fully in slow motion.” If Treasuries aren’t risk-free, then the entire structure of yields and spreads has to be reconsidered. In this piece, we’ll build a framework for evaluating preferreds in the Bitcoin Age. We’ll cover the capital stack, spreads, and comparables. If the foundation has shifted, investors need new tools. Consider this letter an exploration of how these credit instruments are evolving.

This extended $75k–$110k range has caused some to wonder if the bull run is exhausted. But what if the on-chain evidence tells a totally different story? Join James Check (Checkmate of Checkonchain) and Connor Dolan for a data-driven discussion on what a maturing bitcoin market means for the road ahead. James will break down:

On-chain metrics show bitcoin has crossed the Rubicon—from a nascent store of value into a true institutional-grade asset class. This session will help you understand what that means for this bull market and beyond—and how you might position yourself appropriately. Tuesday, September 30th at 3PM CT — online, free to attend. Register now for early access to a new on-chain metrics report from Unchained and Checkonchain:

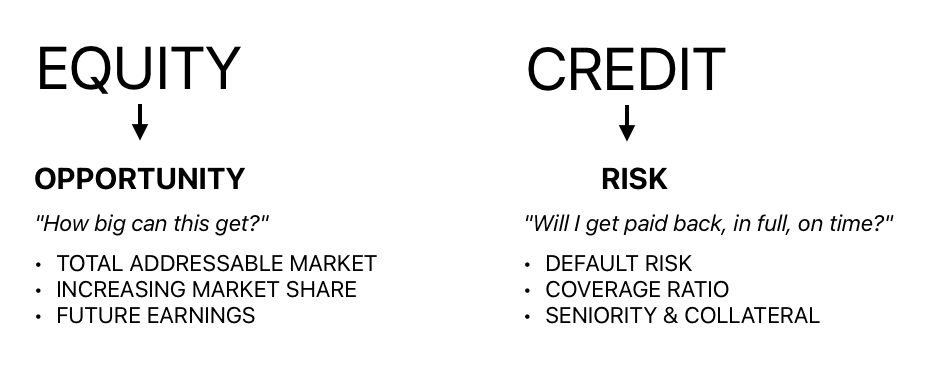

Blockstream Jade Plus is the easiest, most secure way to protect your Bitcoin—perfect for beginners and pros alike. With a sleek design, simple setup, and step-by-step instructions, you'll be securing your Bitcoin in minutes. Seamlessly pair with the Blockstream app on mobile or desktop for smooth onboarding. As your stack grows, Jade Plus grows with you—unlock features like the air-gapped JadeLink Storage Device or QR Mode for cable-free transactions using the built-in camera. Want more security? Jade Plus supports multisig wallets with apps like Blockstream, Electrum, Sparrow, and Specter. Protect your Bitcoin, sleep better, stack harder. Use code: TBL for 10% off. Risk MindsetPreferred stocks are a bit strange in that they are technically equity but practically debt. If we want to think about preferreds, we need to do it in terms of credit, not equity. When we talk about equity, we mean common stock, where a shareholder has a claim on the future earnings of the company. Equity is about growth. It’s about figuring out how the company is adding value and what it is selling. Is it a product or a service? What is the total addressable market? What are they developing? How innovative are they? How can they increase market share, or how can they expand the market itself? Equity is about growth, earnings, and opportunity. Credit is a different game. With credit, it is all about risk. What is the risk that the company defaults on its debt? How can a creditor improve their odds of getting their money back, even if the company goes bankrupt? What is the company’s ability to service its obligations? When you are thinking about preferred stock, you need to switch from a growth mindset to a risk mindset.

Strategy’s TwistPreferred stock is not a very “sexy” instrument to own. They’re rather boring, with less liquid markets than common stock, because preferreds are designed to provide a steady yearly yield instead of potential value gains like common stock. So why are the preferreds issued by Strategy relatively “hot”? They’ve managed to do large IPOs and attract more trading volume than most other preferreds. That comes down to a few unique selling points:

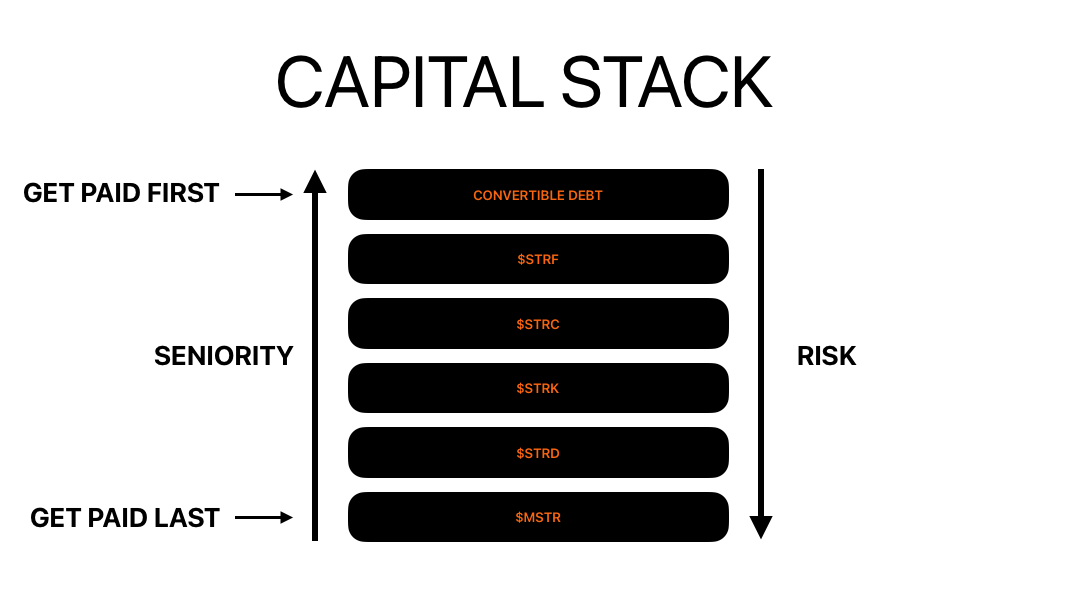

We’ll explain these USPs throughout this letter. The combination makes these preferreds very attractive—at least if you believe bitcoin is valuable and will continue to gain value. This is a key point, and it applies to Strategy’s common stock as well. In a recent letter, BTC-Backed Yield Curve, we explored what Stretch ($STRC) is and its main characteristics. That piece was more focused on what bitcoin treasury companies are and how to think about them. We recommend reading it to get a broader view of what they’re trying to accomplish. Issuing preferreds is only one “tool” Strategy has (and soon others may adopt) to raise capital in order to accumulate more bitcoin. Capital StackTo understand why preferred stock yields what it does — and why Strategy’s preferreds sit where they do — we need to revisit a basic concept in corporate finance: the capital stack. Think of a company as a pyramid of claims. At the top are the safest lenders, and at the bottom are the equity holders. In between sit various shades of debt and hybrid instruments. When things go well, everyone gets paid. When things go badly, the order of repayment is determined by seniority in the stack. Here’s the general hierarchy:

Why Seniority MattersSeniority defines risk and reward. At the top of the stack, secured lenders take little risk and earn modest yields. At the bottom, common shareholders accept volatility in exchange for potential multi-bagger returns. Preferreds sit in the middle. They carry more risk than bonds (no maturity, discretionary dividends), but less risk than common equity. One might argue against owning preferreds because they sit below debt in the hierarchy. But here is the first twist: if the company doesn’t issue traditional debt, the preferreds rise to the top of the capital stack. They get paid first. That’s why you need to analyze the full stack before making a judgment call. Currently, Strategy still has outstanding convertible debt. The goal is for preferreds—with STRF as the crown jewel—to sit at the top of the capital stack. But this is a transition that takes time. Of the $8.2 billion in convertible debt outstanding, $5 billion remains out-of-the-money, and $3.2 billion is in-the-money. In other words, the current stock price of $MSTR trades above the conversion price on some converts, which makes them in-the-money.

As you can see in the overview, the convert with the highest conversion price is the 2029 note, at $672.40. All of these converts include clauses that allow the debt to be converted before maturity. We didn’t research the exact conversion dates, but if the stock price trades above the conversion levels and those dates have been reached, Strategy could start converting this debt into equity. This would be dilutive to the common stock but would strengthen the position—and credibility—of the preferred stock. It’s a clear dichotomy of incentives, a structural tension in the capital stack. Strategy already calculates mNAV, including the assumed dilution from these converts, so future dilution is accounted for in its reporting.

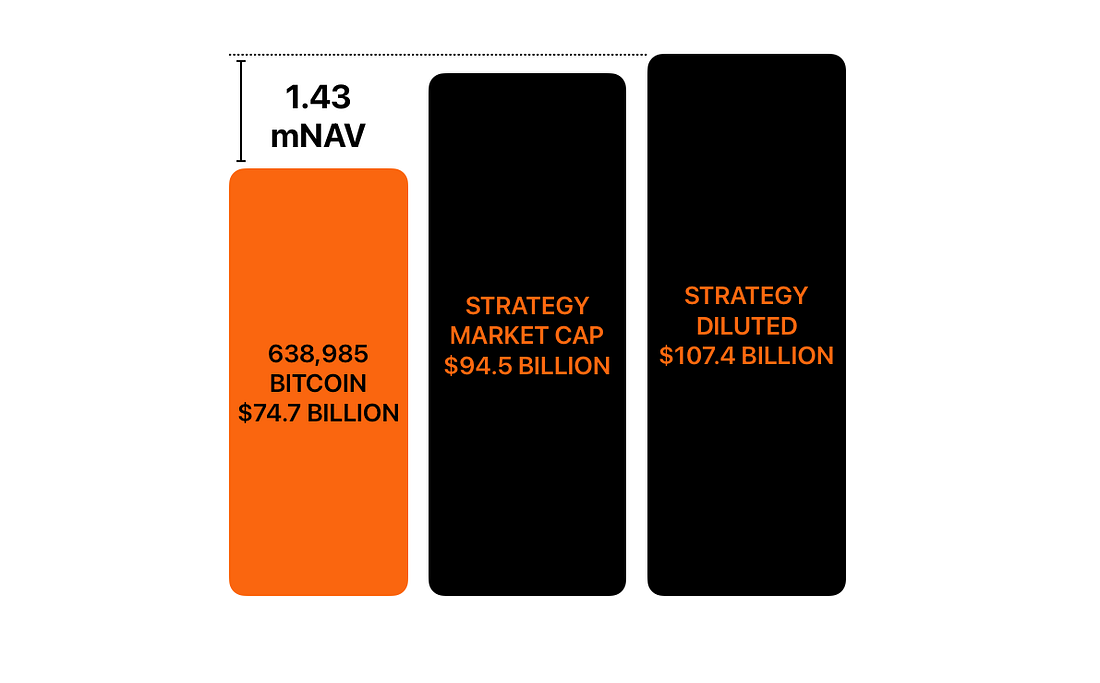

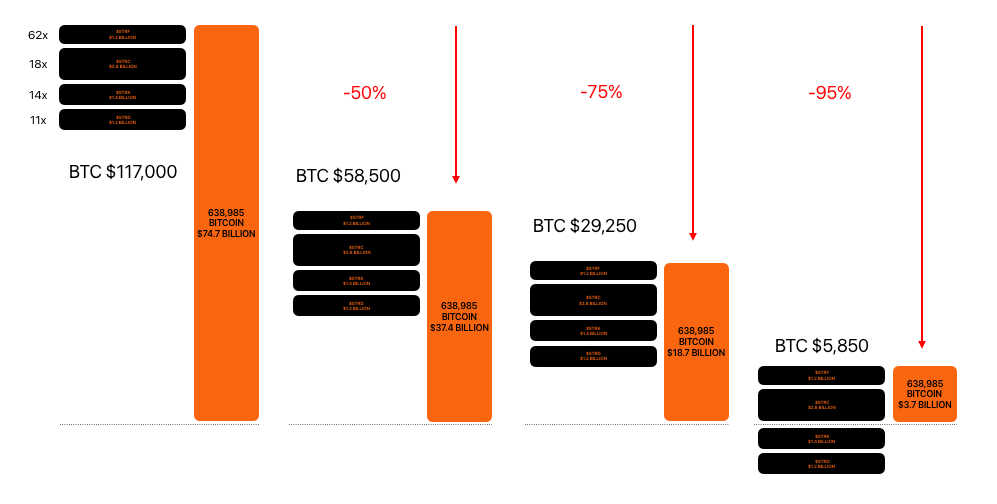

CollateralWhile unlikely in a no-debt situation, it’s important for educational purposes to note that assets on the balance sheet must be unencumbered. An unencumbered asset is owned outright by the company, free from claims, mortgages, or other legal obligations. These assets can be sold, transferred, or pledged as collateral for new loans because they are not already tied up. For preferred stock to have a solid credit rating—meaning a high probability that shareholders receive dividends and the liquidation preference in case of insolvency—the bitcoin on the balance sheet must be unencumbered. In 2022, Strategy took out a loan with Silvergate Bank, collateralized with bitcoin. That gave the bank the right to liquidate the pledged assets if Strategy failed to pay interest or if the collateral fell below the required value. That was an example of some of Strategy’s bitcoin being encumbered. At the time, they hadn’t issued preferred stock yet. If they were to raise capital now with a BTC-collateralized loan, it would undermine the credibility of their preferreds. Please note that the image below is a simplified model, not the current reality. We left out the outstanding convertible debt to show how to think about preferreds once the converts are either repaid or converted into equity. In other words, when that liability is gone. At that point, STRF would sit at the top of the capital stack. At today’s levels, the assets on the balance sheet would be worth 62 times the nominal value of the preferreds. This multiple is also known as the BTC Rating. With the converts gone, bitcoin could fall 75% to around $30,000, and there would still be enough value in the stack to cover the outstanding preferreds. Only at $6,000 bitcoin—an almost 95% drawdown—would there no longer be value to back STRD and STRK. For investors who see bitcoin as pristine collateral with long-term value, these preferreds look attractive because of the size of Strategy’s bitcoin holdings. If we return to the structural tension on the balance sheet, it becomes clear that preferred holders actually benefit when Strategy issues more common stock to buy more bitcoin. This strengthens the balance sheet without adding liabilities, increases the credibility of the preferreds, and works as a form of deleveraging.

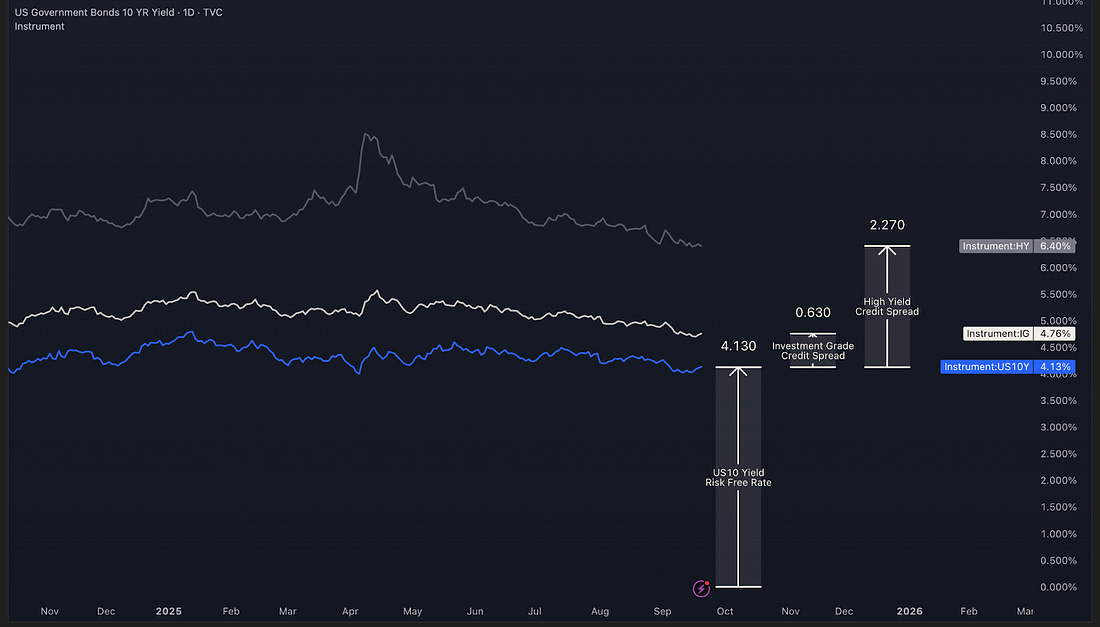

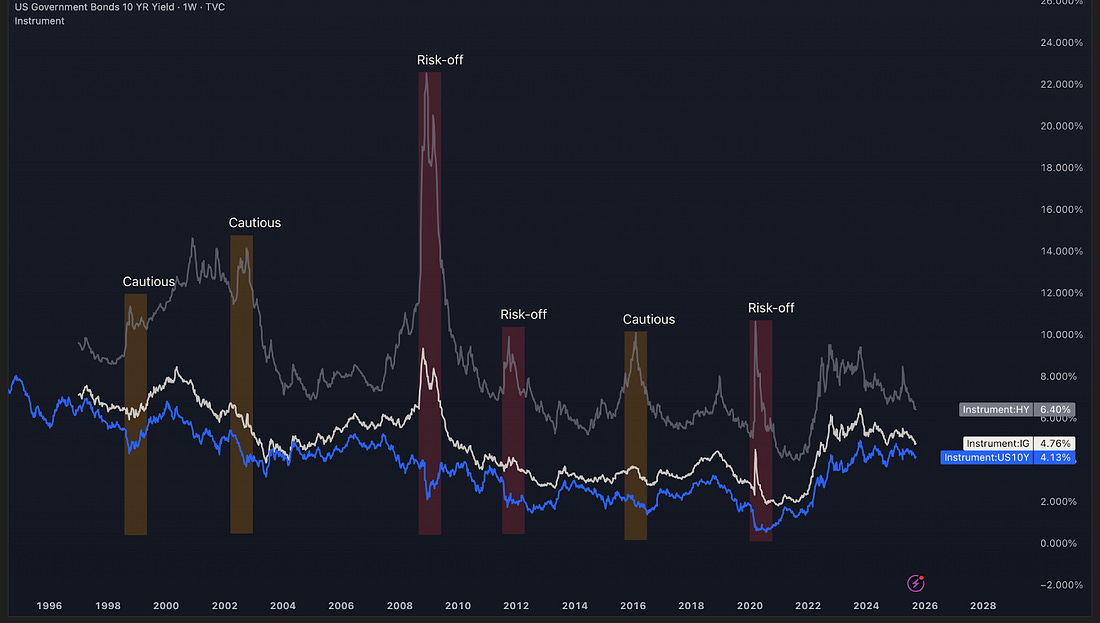

BenchmarkWhen people talk about investment grade versus high yield, they’re really describing two different neighborhoods in the credit market. Investment grade (IG) bonds are issued by companies with stronger balance sheets, steadier cash flows, and credit ratings of BBB or higher. They represent the safer end of corporate credit, and as a result, the yields are lower. In the chart below, we show the U.S. 10-year yield, which most credit spreads use as a starting point. And with IG now yielding 4.76%, that leaves a spread of just 63 basis points. High yield (HY), by contrast, is the riskier part of town: companies with more leverage, shakier earnings, or smaller, less diversified businesses. Their bonds carry ratings below BBB–, which should compensate investors for taking on more risk. HY is currently yielding 6.40%, or 227 basis points above the so-called risk-free rate. Both categories are easy to access for everyday investors through liquid ETFs: $LQD for investment grade, and $HYG or $JNK for high yield.

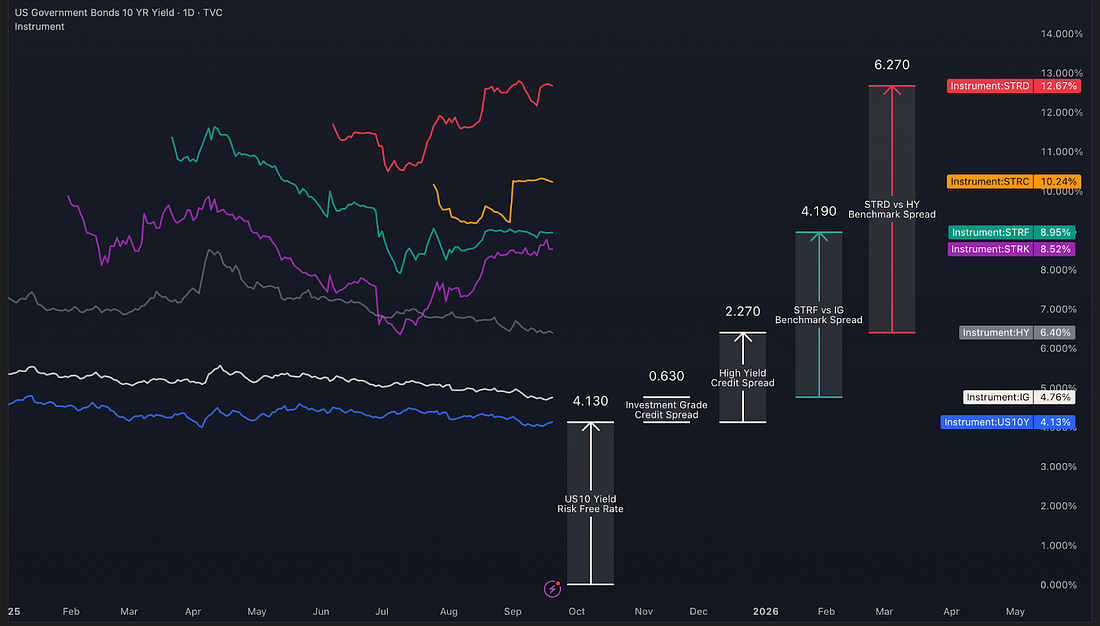

This is where Strategy’s preferreds become interesting. STRF, for example, pays a fixed $10 dividend. On paper, that works out to a spread of 400–500 basis points above IG corporates, which makes it feel more like a high-yield instrument. Some would argue it’s not a fair comparison with investment-grade bonds, since debt ranks higher in the capital stack and preferreds aren’t as safe as corporate debt. But as we explained earlier, once the convertible debt is removed from the balance sheet, it does become a fair comparison. STRF would be most senior in the stack, with cumulative dividends, a moving liquidation preference, and enhanced clauses designed to ensure shareholders get paid. At present, it has a BTC Rating of 7.7x. One could debate whether that makes it investment grade today, but this is how it has been presented to the market. STRD, another series, also offers 10%, but its position in the stack makes it closer to high-yield comparables: junior to senior debt, perpetual in structure, and with non-cumulative dividends. This is where the investor decision comes in. Would you rather own high-yield corporate bonds, dependent on future earnings of those companies for a 6.40% yield, or own STRD, which sits lowest on Strategy’s stack and yields about 12%? The market is effectively saying that STRD carries much higher risk. Otherwise, HYG holders should sell their positions and rotate into STRD. That would push HYG yields higher (as investors sell the ETF) and bring STRD yields lower (as buyers bid up the price, reducing the effective yield). As we’ve said before, we’re not here to tell you what to think, but how to think. The real question for investors is this: is STRF more risky than LQD, or is STRD more risky than HYG? And if so, what is the right spread? Currently, those spreads are 419 basis points and 627 basis points. For the enthusiasts, the chart below shows something resembling a theoretical risk curve: least risk and lowest yield on the bottom left, with each step to the right moving up the risk spectrum—and the yield curve along with it.

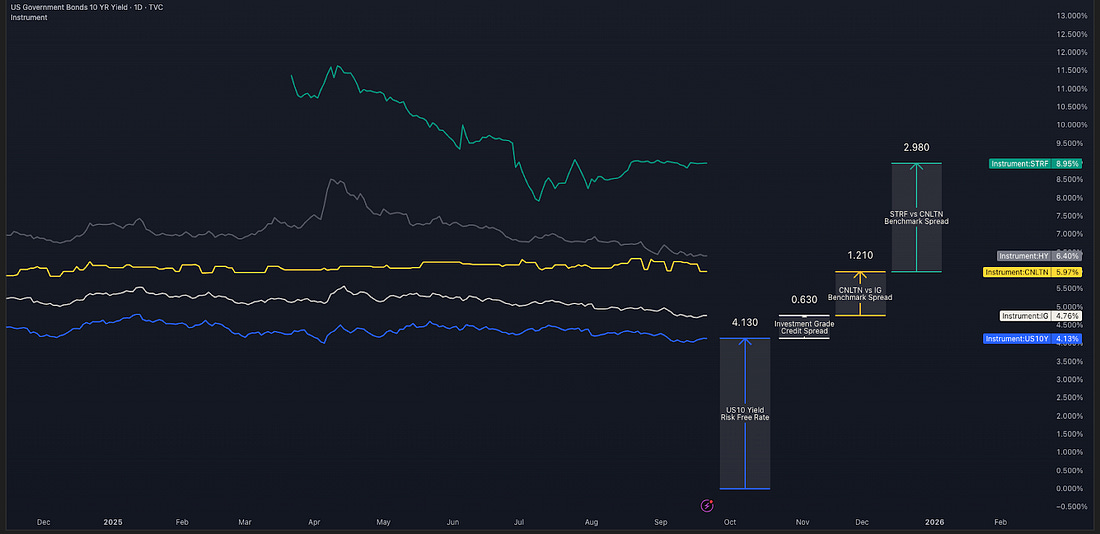

ComparisonPut STRF next to an old-school utility preferred like CNLTN, and you can feel the two worlds of “income” diverge. CNLTN is a 1947-vintage, $50 par Connecticut Light & Power issue that pays $2.00 a year (a 4% fixed coupon), cumulative and callable at $54 plus accrued dividends. It sits below a tower of senior utility debt—first the secured mortgage bonds and unsecured notes at the operating company, then holding-company paper—so its safety comes less from seniority and more from the regulated, steady cash flows of a New England wires business whose returns are set by commissions. The risks are concrete and local: ice storms, hurricanes, regulatory disallowances, and cost-recovery lag. Rarely existential, often boring, occasionally expensive. Unique Selling PointsAt the beginning of this letter, we mentioned five USPs that make Strategy’s preferreds attractive (if you value bitcoin). We covered the large bitcoin asset backing, their place in the capital stack and eventual move to seniority, and the high dividend payments. What we haven’t covered yet, but will here, are:

CallabilityCNLTN is callable once the stock trades above $54. STRF is practically non-callable. What does that mean for an investor? As you know, fixed dividend preferreds—like bonds—have yields that move inversely with price. If price goes up, the effective yield goes down. With CNLTN, it often feels like “the house always wins.” Here’s why:

STRF and STRD, by contrast, are practically not callable. They can only be called under very specific conditions, not simply because they trade above par. That gives them more potential for upside price gains, making them more attractive. The caveat is that investors should expect Strategy to keep issuing new preferreds. More supply can dampen how high valuations can run. Moving liquidation preferenceThe last USP is the moving liquidation preference. The floor is $100, but it increases if the preferred trades above par. That means if someone buys at $130, their liquidation value adjusts upward, so they don’t immediately face a $30 gap. This feature makes it easier for investors to pay above par, which supports higher trading prices. Where CNLTN’s price mostly breathes with interest rates and utility credit spreads, STRF’s risk lives in a different dimension: bitcoin volatility, access to capital markets, and management’s discipline in sizing obligations versus collateral. That’s why STRF can trade at yields that look “high-yield-ish” even though it isn’t funding a risky operating business. And why, if base rates slide, STRF’s upside isn’t automatically capped by a simple issuer call. So again, the question for investors: what do you deem riskier, CNLTN or STRF? And what should the spread be between them? If the market isn’t pricing them the way you think it should, that mispricing could present an opportunity.

RotationAfter comparing preferreds with other debt instruments and legacy preferreds, they can also be compared against each other. In the chart below, we’ve mapped different risk environments. By looking at the U.S. 10-year yield, investment grade, and high yield, you can spot periods when they all move in the same direction.

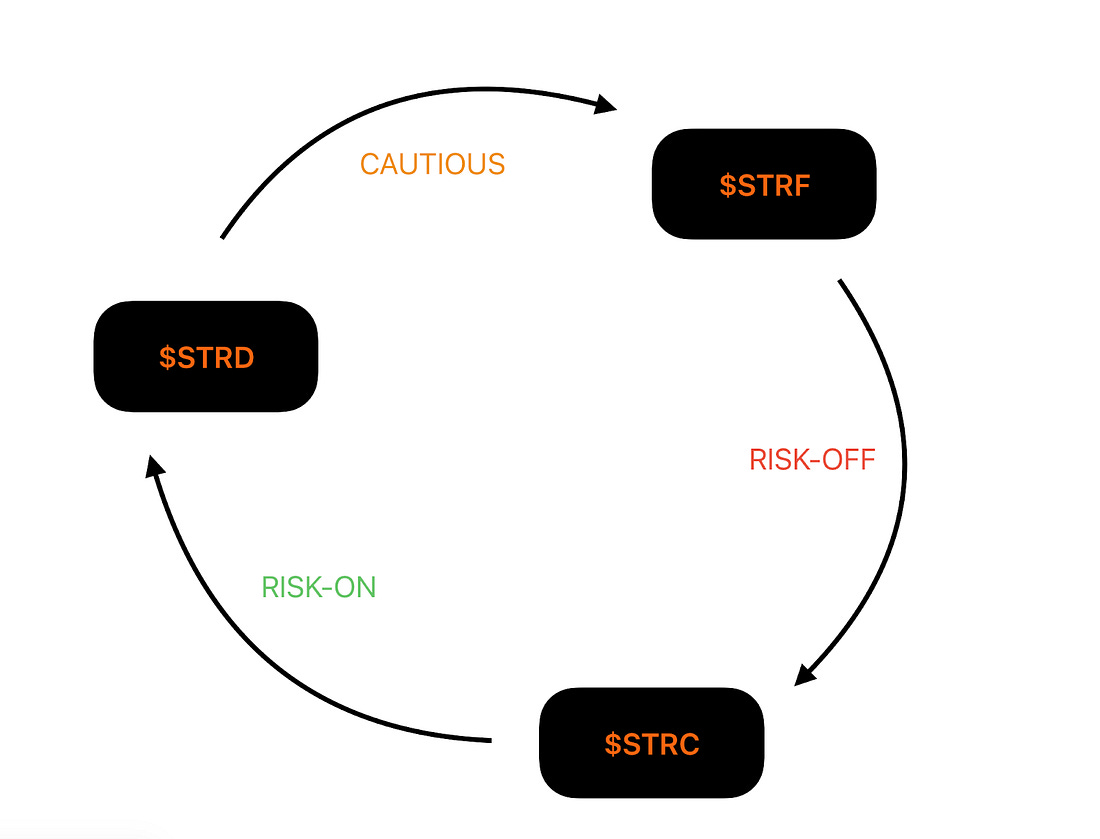

While there are many more scenarios and possibilities, we’ve highlighted these as the ones to act on in theory. But remember, we began this letter with the idea that U.S. government bonds may no longer serve as the safe haven they once were. So the question becomes: what could be the alternative safe-haven asset in times of financial distress?

Stretch could be an alternative that maintains a relatively stable price around $100 while still delivering a high yield. Because Strategy offers a variety of preferreds, an investor can stay within bitcoin-backed credit instruments yet still choose the one that fits their needs across different risk environments. In a risk-off environment, even investment-grade spreads widen, which would likely cause STRF to sell off as well. In that case, an investor might hold STRC while capital markets remain rough. When the storm passes and conditions improve, STRD could offer both high yields and potential price appreciation. In periods where there isn’t a full-blown crisis but markets are showing signs of fear, high-yield spreads might rise while investment-grade yields remain stable or even fall. In that environment, STRF could be the more compelling choice.

The New Hurdle RateThis letter is titled The New Hurdle Rate. Many have argued that bitcoin’s CAGR could—or should—be seen as the new hurdle rate. It’s the rate against which investors compare other opportunities to decide whether they are attractive. That framing makes sense for equity, as we’ve discussed. These assets carry higher volatility and revolve around the question: How big could this get? But what will the new hurdle rate be for credit instruments? The ones that focus on risk and receive compensation for taking that risk? The ones centered on the question: Will I get paid back, in full, on time? What risk are you willing to take, and what compensation do you demand in return? If dividends or interest payments are denominated in dollars—while the supply of dollars grows 7% per year—what is the minimum yield you require? Strategy introduced these preferreds with exactly these questions in mind: how can we raise capital in the Bitcoin Age? Now the market must decide how to treat them. Will they be seen as risky because the issuer holds bitcoin on its balance sheet? Or will they be seen as safe for the same reason? Will they be repriced, and if so, how far will that repricing go over time? We’ll keep asking these questions, and we’ll keep sharing our thoughts with you. Thanks for reading,

This extended $75k–$110k range has caused some to wonder if the bull run is exhausted. But what if the on-chain evidence tells a totally different story? Join James Check (Checkmate of Checkonchain) and Connor Dolan for a data-driven discussion on what a maturing bitcoin market means for the road ahead. James will break down:

On-chain metrics show bitcoin has crossed the Rubicon—from a nascent store of value into a true institutional-grade asset class. This session will help you understand what that means for this bull market and beyond—and how you might position yourself appropriately. Tuesday, September 30th at 3PM CT — online, free to attend. Register now for early access to a new on-chain metrics report from Unchained and Checkonchain: Thanks for reading The Bitcoin Layer — for access to all content, upgrade to paid!

|

Monday, September 22, 2025

The New Hurdle Rate

Subscribe to:

Post Comments (Atom)

Popular Posts

-

During a crypto cycle where few communities are feeling their best, Hyperliquid is continuing to make its fans happy with major new upgrade...

-

Citizen Brief: gm, it's been a brutal 2025 for crypto's top tokens, but not everything is looking red on the 90-day charts...

-

Good opsec can't protect you from every attack vector in crypto, but our resident DeFi explorer has some tips to help you keep your fun...

-

Also Bitcoin Is Getting Closer To Test Its Long-Term Trend & Inflation Is Rising Again ͏ ͏ ͏ ͏ ͏ ͏ ͏...

-

The best thing right now is to find protocols with great fundamentals that you can hold for 6-12 months. Since mar...

No comments:

Post a Comment