Inflation Won't Come Down And The Fed Is Pissed: TBL Weekly #85You feel it in your wallet, and now the Fed is feeling it from news outlets and vocal critics.Welcome to TBL Weekly #85—the free weekly newsletter that keeps you in the know across bitcoin, rates, risk, and macro. Grab a coffee, and let’s dive in.

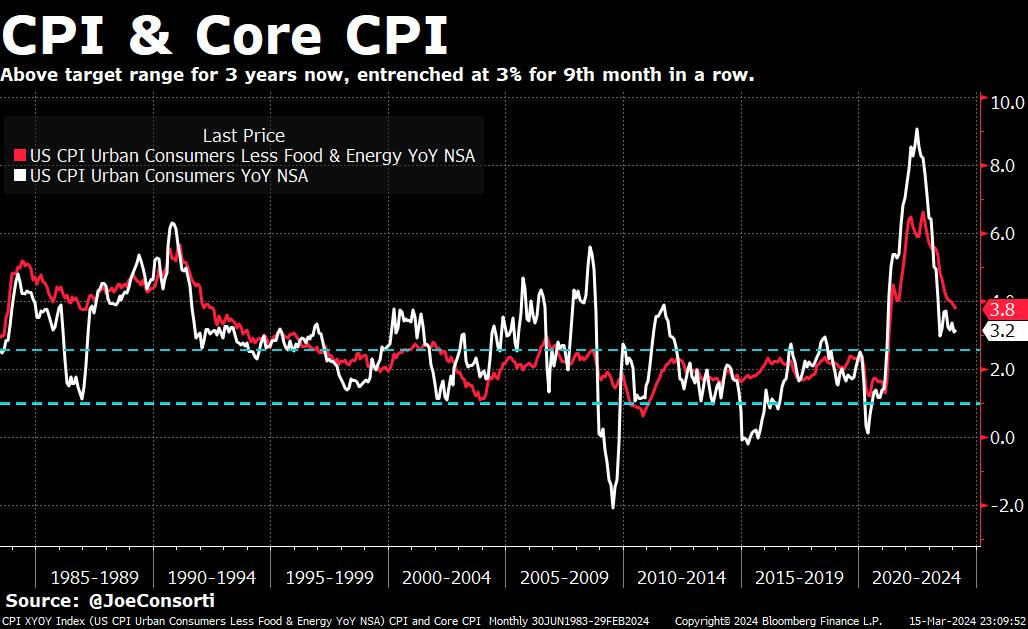

River is our Bitcoin exchange of choice. Securely buy Bitcoin with zero fees on recurring orders, have peace of mind thanks to their 1:1 multisig cold storage custody, and withdraw at any time. Need help? They have US-based phone support for all clients. Now introducing River Link 🔗allowing you to send Bitcoin over a text message that can be claimed to any wallet. Give a gift, pay a friend for dinner, or orange pill your friends, completely hassle-free. Use River.com/TBL to get up to $100 when you sign up and buy Bitcoin. The week got off to a rough start with CPI coming in above the expectation of 3.1% annually at a still-hot 3.2%. Core inflation also came in hotter than anticipated, decelerating to 3.8% instead of the expected 3.7%. This marks the 9th month in a row where price inflation has been higher than the Fed’s target of 2%, which has been loosely held over the past several decades between 1% and 2.5% with transient periods above and below. I’ve denoted this range in the blue dashed bars in the chart below, with headline CPI in white and core CPI in red—note the volatility of headline due to food and energy prices compared to core which has removed them. We’ve been in the longest elevated inflationary regime since the early ‘90s:

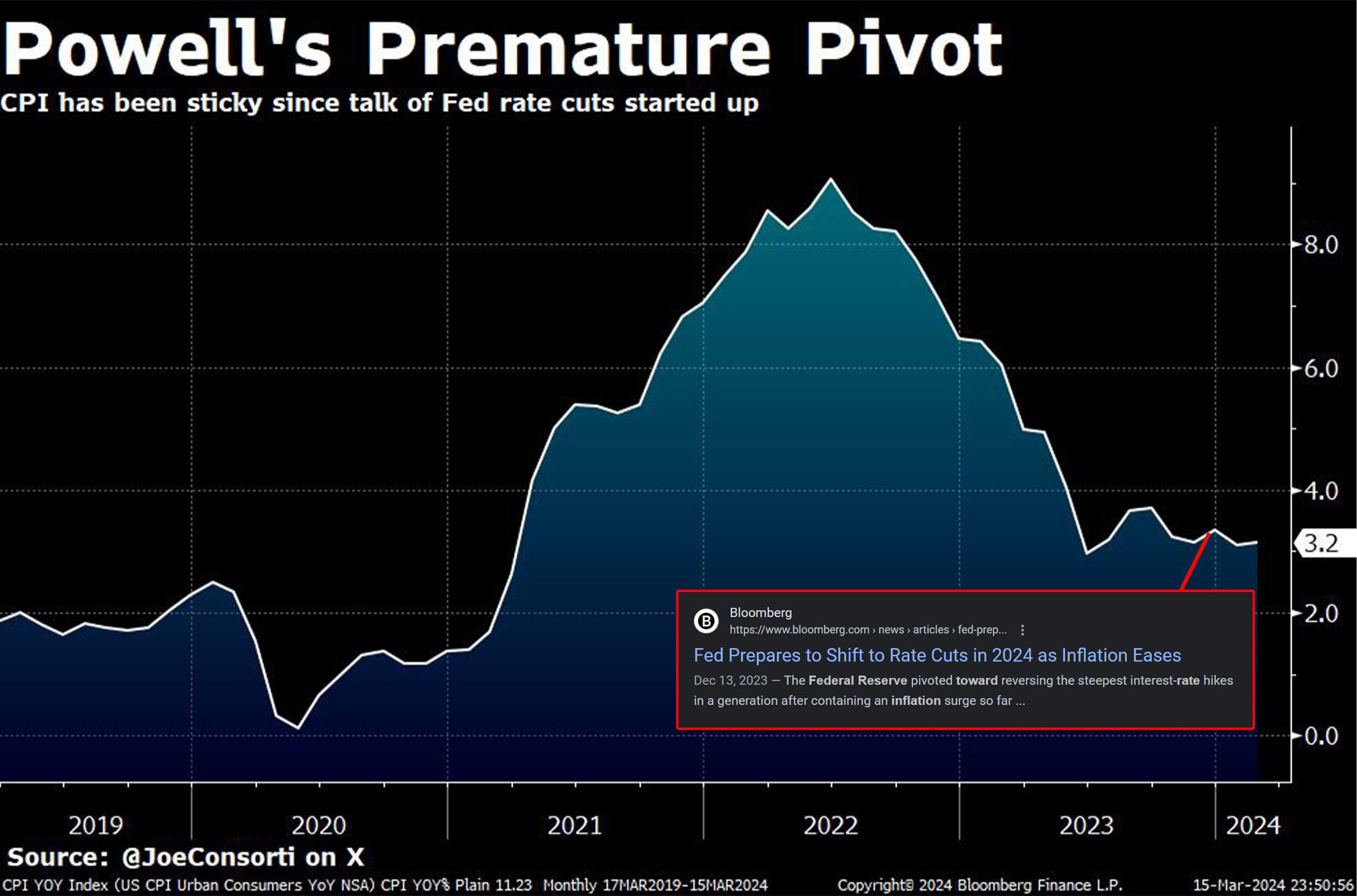

Following the dismal CPI print, Treasury Secretary Janet Yellen finally relented on Wednesday that the Fed and Treasury regret saying inflation was transitory: The reason for such a colossal blunder on inflation? One has not been provided. We’d wager it is a combination of being too late to hike initially, paired with prematurely forecasting rate cuts on the horizon before CPI reached 2%. The latter measure was done in an effort to not risk deflation and allow price inflation to descend gracefully onto the 2% runway instead of crashing below it, but the Fed clearly missed the mark on timing, instead landing on the 3% runway and being unable to shake it. With Powell so close to reframing his legacy as Volcker’s heir apparent in his unabashed hawkishness, he quickly reverted to his inner squeamish and dovish Arthur Burns tendencies. Sad!

Biden humorously remarked later on Wednesday that “we have the lowest inflation rates of any country in America.” While the rest of the world is likely what he meant and not Canada, Mexico and Honduras, that’s not true either. Japan, Germany, France, the UK, and many other Western and developed countries have lower annual price inflation rates as of March 2024 than the United States. Worse yet, consumers don’t think inflation is going to come down, which throws a wrench into the Fed’s inflation progress, as inflation expectations drive spending habits and therefore impact price inflation quite a lot. One-year ahead consumer inflation expectations have risen to 3.04%—not too far off from where we are today. If you’re up for election less than 8 months from now and the main issue for voters is inflation, this is not the kind of data that inspires confidence, this is the kind of data that inspires phone calls to the Federal Reserve for them to do something about it:

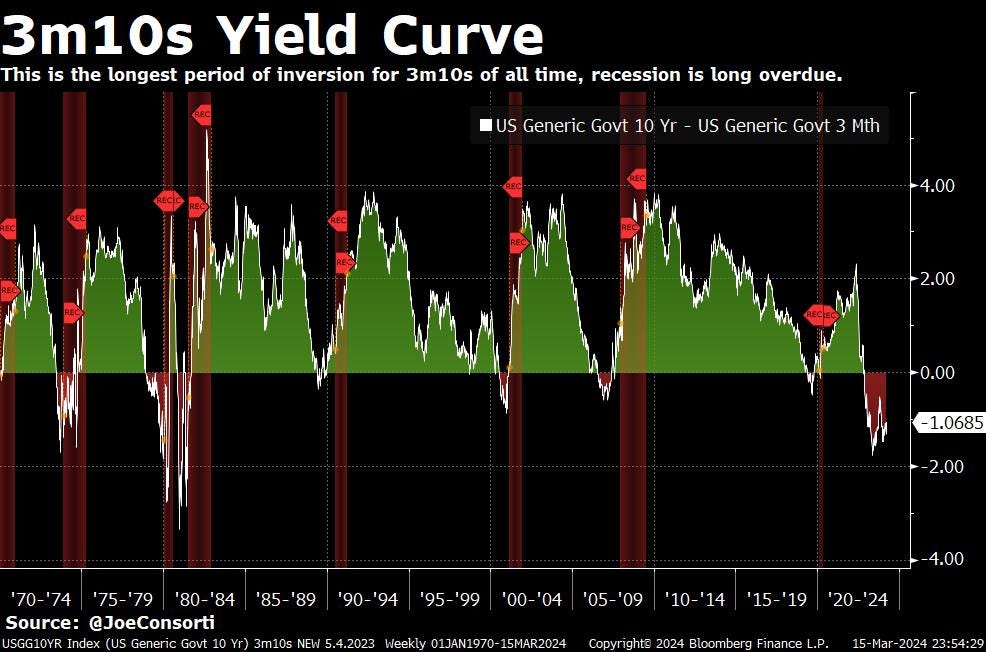

Asset prices are also raging, with the S&P 500 almost 5200 and bitcoin cresting $72,000 per coin (don’t miss our updated $300,000 price target analysis from Thursday). With assets soaring into the stratosphere, financial conditions are clearly not as tight as Powell would like them to be, and increased spending as a result of heightened asset prices (wealth effect) is yet another tailwind too. The market clearly has not taken the Fed’s talk of holding rates high and tight very seriously, opting to pay much more attention to the Fed’s seemingly premature talk of cuts. With the FOMC meeting arriving next week, Powell has the stage to reign in inflation expectations by talking down a hot stock market and seriously hunkering down on keeping rates where they are until the inflation battle is won. If he really wants to get serious, he could take cuts off the table entirely. He will not do this. Why? He is not cutting to ease deflation (which we don’t have yet), he is cutting to save the banks. With the Fed’s sweetheart bailout BTFP facility ending this week, banks need all the support they can get. The Fed’s mandate that trumps all others is financial stability, and whether or not it says this explicitly, it is what the Fed prioritizes when push comes to shove. Also, the yield curve has been inverted for its longest period ever. Banks borrowing short and lending long doesn’t exactly work when front-end rates are 100 bps higher than long-end rates for years on end. With profitability in the toilet and emergency facilities increasingly restricted and scrutinized, the Fed’s projected cuts this year won’t be to ease a broken economy as much as they’ll be to support our financial plumbing:

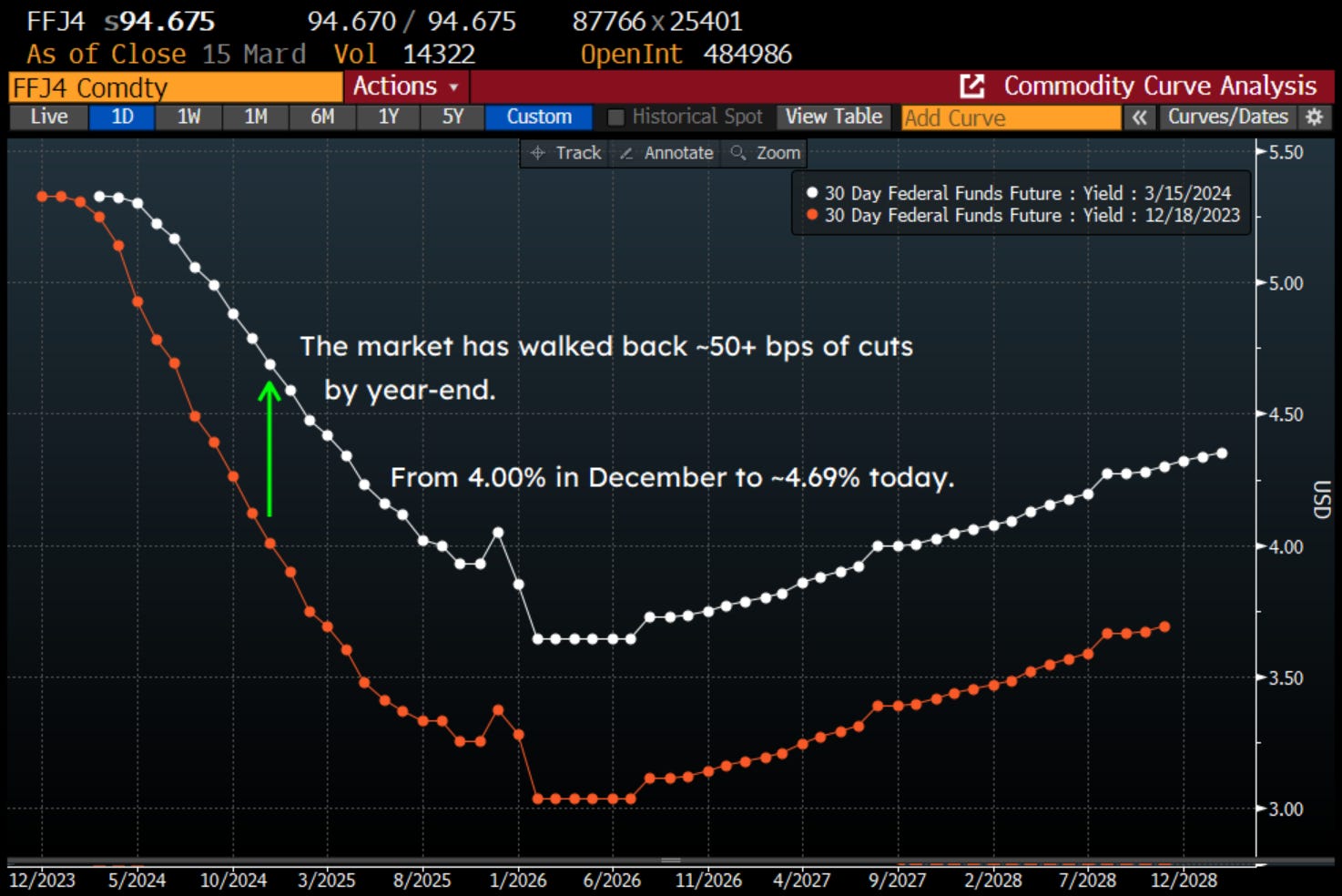

Here are the curves for Fed Funds projections from December (orange) and today (white). Fifty bps of cuts are priced in by the end of the year. The market has walked back ~50 bps of expected cuts by year-end thanks to persistent inflation and a rip-roaring economy and asset markets, rising from 4% in December to 4.69% today:

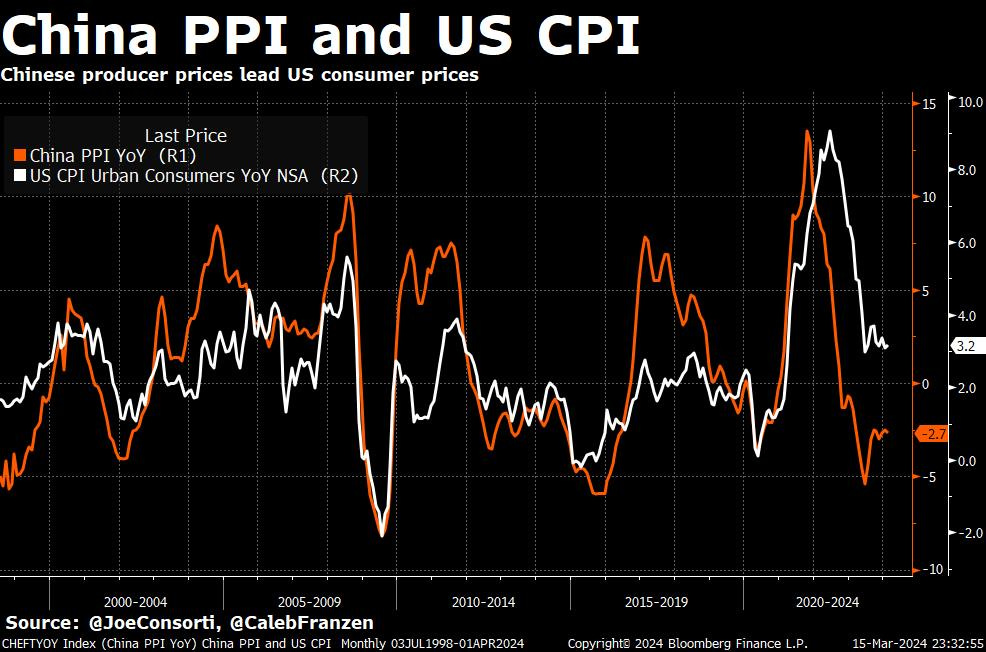

Regardless of what the Fed’s decision is come Wednesday, the inflation fight is more out of their hands than ever before. For one, with the federal deficit wider than ever relative to GDP and the President’s announced $7.3 trillion budget for the next fiscal year, we’ve never been spending more for fewer units of economic output. This much fiscal spending into the economy asserts dominance over the Fed’s tools of policy rates and its balance sheet, lessening the impact of, and even outright negating the Fed’s tightening efforts, as we discussed in last Monday’s post. Additionally, the global inflationary impulse has always played a substantial role in what happens domestically. The recent reacceleration in Chinese producer prices due to economic stimulus has once again driven US CPI higher along with it. As long as China’s economy is dragging its heels and the government pumps it full of stimulus to get it going again, a tailwind propping US CPI off of its 2% target will persist:

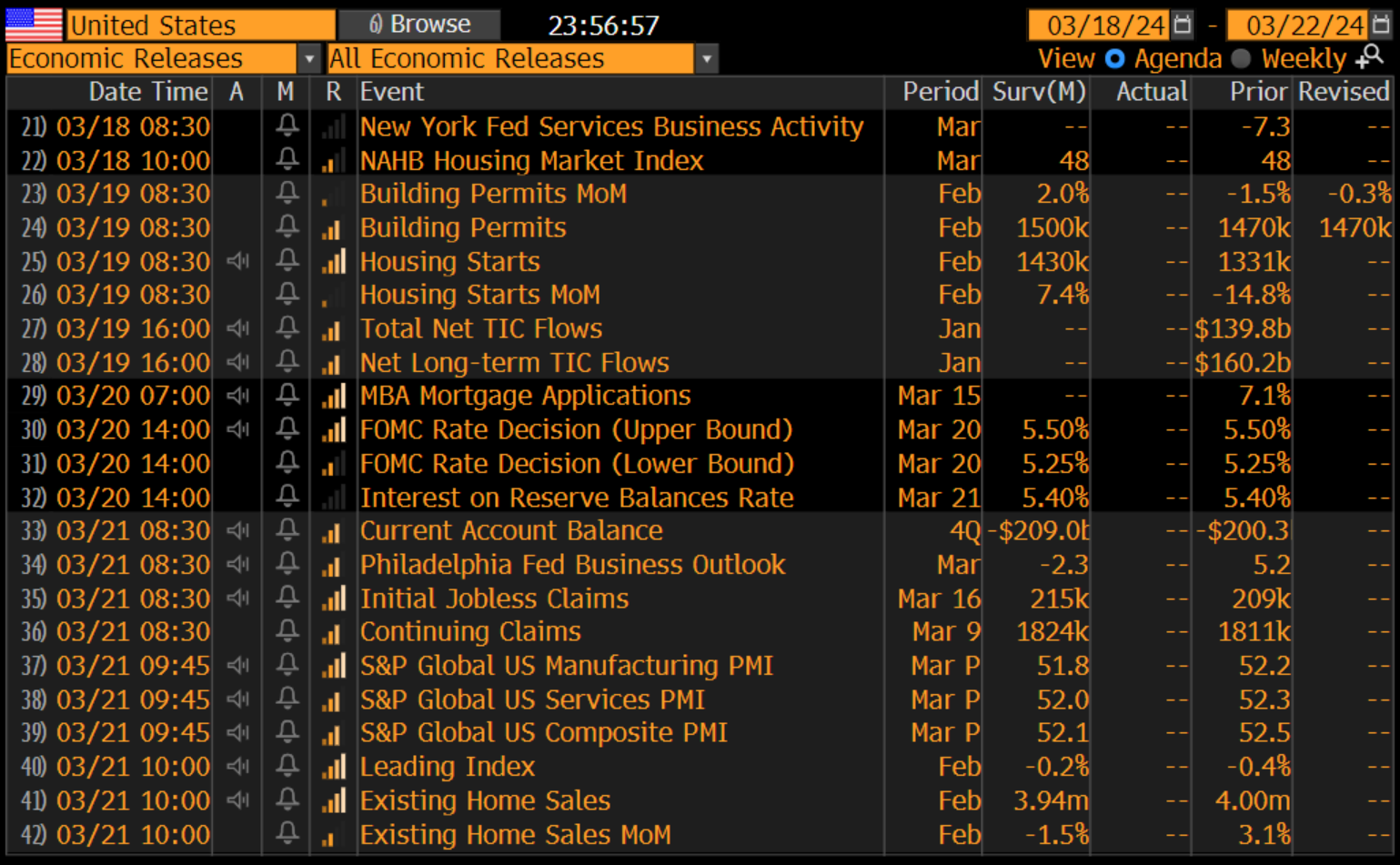

Next WeekIn the week ahead, our focus will of course be on Wednesday’s FOMC decision. Specifically, we will gauge Powell on the aforementioned Volcker/Burns meter, look to the voters’ projections for the policy rate in the quarterly SEP, and search for any clues about the path of reserves and RRP. On the dot plot (SEP, or the Fed’s economic and policy rate projections), expectations from voters are for three cuts this year, but with the recent inflation numbers, some are expecting this could potentially be reduced to two. Whether two or three, we still believe the reason for cuts is financial stability and not inflation. On reserves and RRP and the Fed’s QT schedule, we are extremely curious as to the details we’ll receive. The reason for our curiosity stems from a focus on financial plumbing, ample reserves, and repo funding, combined with a genuine doubt that the Fed understands just how fragile the repo market could get if QT continues on its current path. If the Fed gives us any relevant information on QT changes, our analysis will shortly follow. We do have a suspicion, however, that details will be somewhere between thin and nonexistent—smaller banks will not be happy without an end in sight to reserve drain. On the economic front, we have almost nothing to truly anticipate except for Thursday claims and existing home sales:

Twenty-year Treasuries will be auctioned next week, but without signature tenors and a large net settlement, all focus will be on Powell’s presser. Notice how last week’s large 10- and 30-year auctions and the net settlement on Friday resulted in much higher yields on the week, even though the 30-year auction was beyond stellar. Don’t pay too much attention to the auction stats themselves but rather the price action surrounding the event. Higher long-term yields are a danger and appear to be the path of least resistance. If you’re enjoying today’s analysis, consider supporting us by becoming a paid subscriber. As a paid subscriber, you get full access to all research as it drops. Here are some quick links to all the TBL content you may have missed this week: MondayIn this episode, Nik presents an explainer on Bitcoin's realized price. In an effort to simplify the understanding of on-chain metrics, Nik gives us basic definitions of nodes, UTXOs (unspent transaction outputs), realized capitalization, and realized price. We look at the formula for realized price, and give several illustrations of the differences between market price and realized price. Check out—What Is Bitcoin Realized Price?  TuesdayThe movement of bitcoin on its blockchain clues us into investor behavior, from which we can determine where we are in the cycle relative to historical norms. Bitcoin has a relatively short history, but today we will rely on that history for guidance and conclude with four charts to speculate on this cycle’s peak. Check out—Long-Term Holders Say BTC Is Nowhere Near The Top: On-Chain Update

In this episode, Nik is joined by Caitlin Long, founder and CEO of Custodia Bank to discuss the current bitcoin bull market. Caitlin shares her thoughts on the enormous demand for bitcoin ETFs since approval, explains why Wall Street will never control bitcoin, and discusses her bank's regulatory fight against the US government. Check out—Wall Street Will NEVER Control Bitcoin  WednesdayIn this episode, Nik is joined by Galaxy head of research, Alex Thorn. Alex gives his take on bitcoin ETF inflows now topping $1 billion per day, explains the ability of shareholders to leverage holdings with prime brokers, and shares an excellent overview of how on-chain metrics are evolving. Learn why Alex believes we are still early in this current bitcoin bull market. Check out—Bitcoin ETF MANIA As Flows Top $1 BILLION PER DAY  ThursdayWhen I first understood bitcoin, I panicked. That’s because I didn’t own any. Unease originated from my mathematical understanding that if bitcoin achieves adoption as global neutral money, bitcoin would trend to about $1 million, or around $20 trillion in market cap. At the time, Treasury supply was trending toward $20 trillion, and the size of the financial system plus real estate totaled several hundred trillion dollars. Over the past few days of observing bitcoin ETF inflows and doing some more rough calculations, I now realize how easily bitcoin will approach my original estimates. Put on your prediction goggles. Check out—Bitcoin to pass MMFs

FridayIn this episode, Nik conducts price study on bitcoin to gauge whether or not the market is overheated and topping out. We begin with an analysis of bitcoin funding markets and a brief explanation of their significance, and then proceed with a look at weekly and monthly candles and bitcoin's relative strength index (RSI). Check out—Is Bitcoin's Bull Run Already Over?  Our videos are on major podcast platforms—take us with you on the go! Keep up with The Bitcoin Layer by following our social media! That’s all for our markets recap—have a great weekend, everyone!

River is our Bitcoin exchange of choice. Securely buy Bitcoin with zero fees on recurring orders, have peace of mind thanks to their 1:1 multisig cold storage custody, and withdraw at any time. Need help? They have US-based phone support for all clients. Now introducing River Link 🔗allowing you to send Bitcoin over a text message that can be claimed to any wallet. Give a gift, pay a friend for dinner, or orange pill your friends, completely hassle-free. Use River.com/TBL to get up to $100 when you sign up and buy Bitcoin. Thanks for reading The Bitcoin Layer — for access to all content, upgrade to paid!

|

Saturday, March 16, 2024

Inflation Won't Come Down And The Fed Is Pissed: TBL Weekly #85

Subscribe to:

Post Comments (Atom)

Popular Posts

-

Join DAS Asia's Most Exclusive Networking Experience ...

-

March 13, 2024 | Read Online 💥Ethereum Targets L2 Scalability As Dencun Goes Live Together with GM Defiers! Ethereum's highly-...

-

Bitcoin Correlations Report, June 2026 ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ...

-

Dear Readers, ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ...

-

Bitcoin's rise to new highs comes at a time when the Fed is not printing money (as hard-money types so fear), but unprinting it. ...

No comments:

Post a Comment