What TBL Liquidity and On-Chain Metrics Are Saying with CheckonchainOur third collaboration with the Checkonchain team, which includes a live Q&A tomorrow!Dear Readers,

We’re happy to, once again, share the stage with our favorite bitcoin on-chain analysts, Checkonchain. Before we get into today’s article, we wanted to quickly remind you that, to celebrate our third month writing together, we will be hosting a live YouTube Q&A tomorrow at 5:30 PM EST (2:30 PM PST):

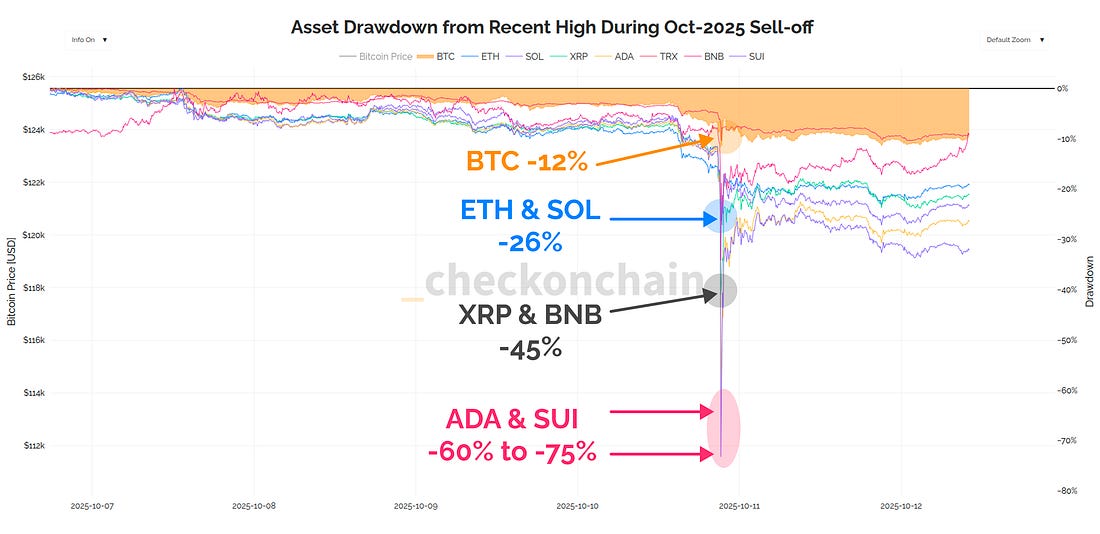

Looking forward to seeing you all there! Let’s get to the article now. As per usual, we will let the Checkonchain team open up with their analysis, and we will close it off with ours: G’day Folks, Is everyone having fun with their Bitcoins? I think it is safe to assume, a lot of us were glued to the Bitcoin price chart over the weekend, watching how the market responded after the largest deleveraging and liquidation event in Bitcoin/crypto history. Whilst Bitcoin sold off -12%, many altcoins got massacred, with ETH and SOL trading down -26%, XPR and BNB cut in half, and SUI and ADA trading down -65% to -75%… and the price of some long tail assets literally went to zero! This event was a real wake-up call for many crypto investors, showing that when volatility picks up and market makers back off, the bid for many of these tokens is simply non-existent.

I’m also very confident that we weren’t the only ones watching the corn price this weekend. Every trader and investor with a Bloomberg terminal was watching it as well to get a read on what their equity portfolio was likely to do Monday morning. Bitcoin is one of the most sensitive assets to liquidity conditions, and even though this sell-off was arguably triggered by a Trump tweet about 100% tariffs with China, the impacts of such a thing would be felt market-wide. In today’s post, we return with our monthly collaboration with team at The Bitcoin Layer, where we will be covering:

It feels to me like markets are very ready to start trending once again, and today’s post is all about recalibrating our expectations, so none of us are surprised by whichever way it breaks. Lastly, as part of our collaboration campaign, we will be extending a 7-Day Free Trial for new subs:

Disclaimer: This article is general in nature, and is for informational, and entertainment purposes only, and it shall not be relied upon for any investment or financial decisions. TL;DR

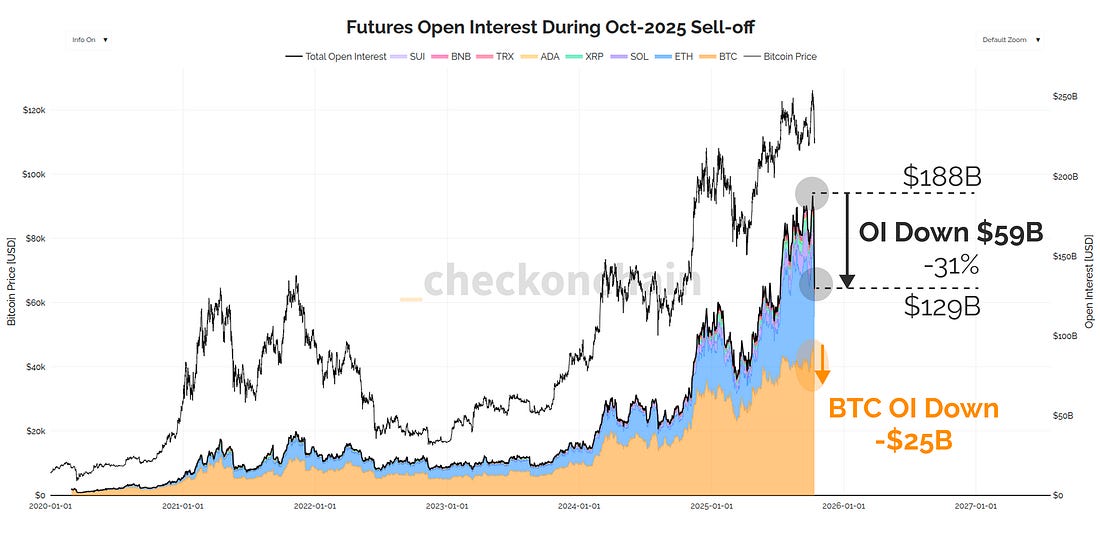

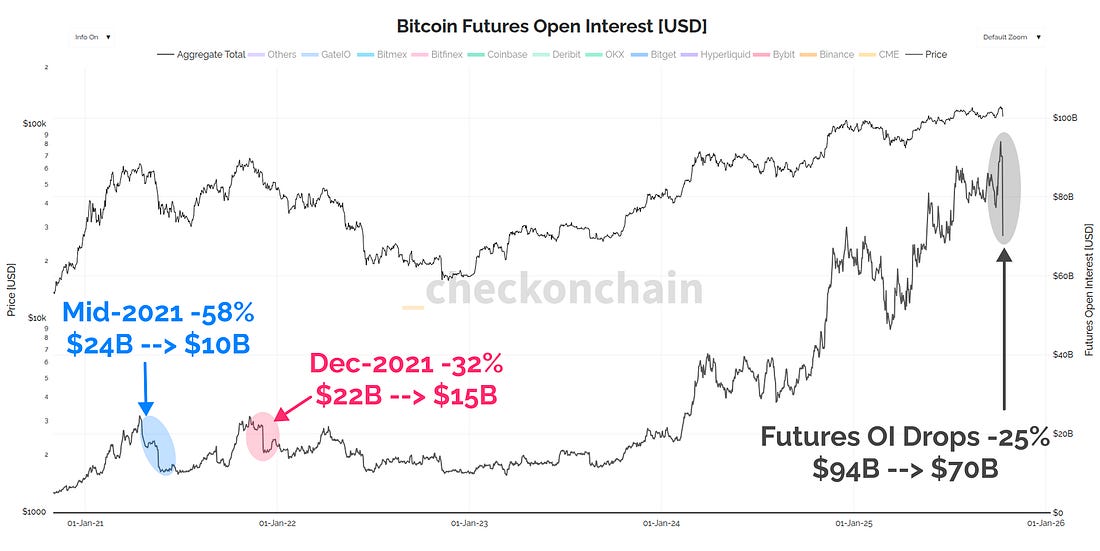

Full Premium Video Futures Forest FireAt the start of October, I published The Bulls Are In Control, which highlighted that the break back above $118k likely signalled we were due a run back to all-time-highs. What I also flagged, is that futures open interest was hitting fresh ATHs, and the odds were increasingly high that we would see a lot more volatility as a result. Whilst there was no way to predict Mr President tweeting about 100% tariffs on an illiquid Friday afternoon, it was likely we’d see a wash-out of futures leverage at some point in time. What is crazy about this particular deleveraging event, is how massive it was in absolute terms. Across the largest crypto-assets, we saw over $59B in open interest flushed out, with $25B (42% of total) coming from Bitcoin markets. The drop in open interest was precipitous, and the majority of the flush out occurred in less than an hour of trading.

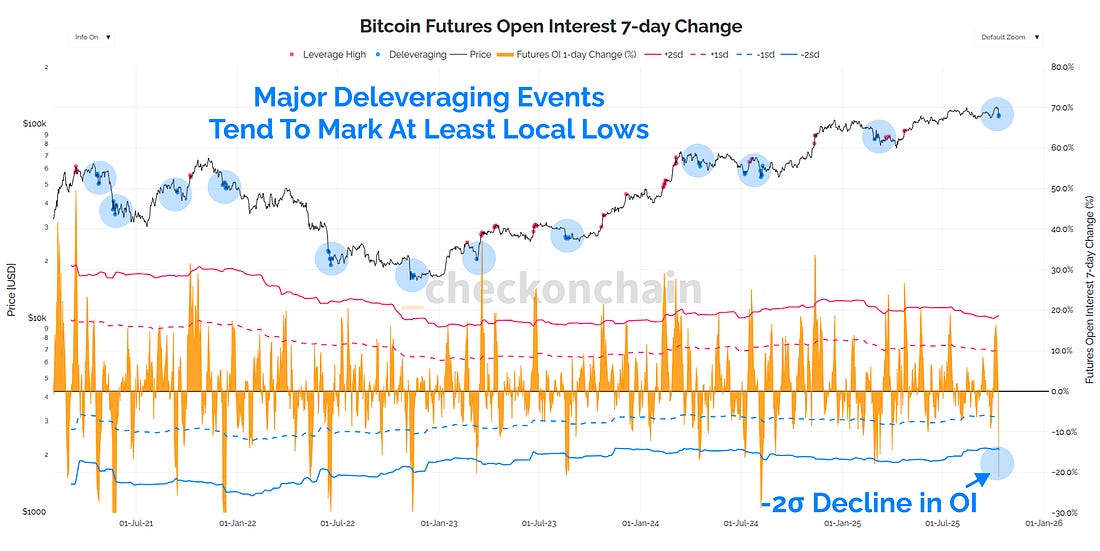

When we look at the open interest decline for Bitcoin specifically, this was a -2σ standard deviation decline, and the largest since the Yen-carry-trade unwind in August 2024. Massive deleveraging events like this are very important to take seriously, because they have several knock on impacts:

I also want to highlight how remarkable it is that Bitcoin could see -$25B in futures open interest flushed out in an hour, and the price only declined 12% from the ATH. The ability for Bitcoin markets to absorb such huge volumes of capital in distress is an incredible signal in itself. I do want to highlight the May and Dec 2021 deleveraging events as a reference point, because if this was to turn out to be the straw that broke the bulls back, these are the right reference points.

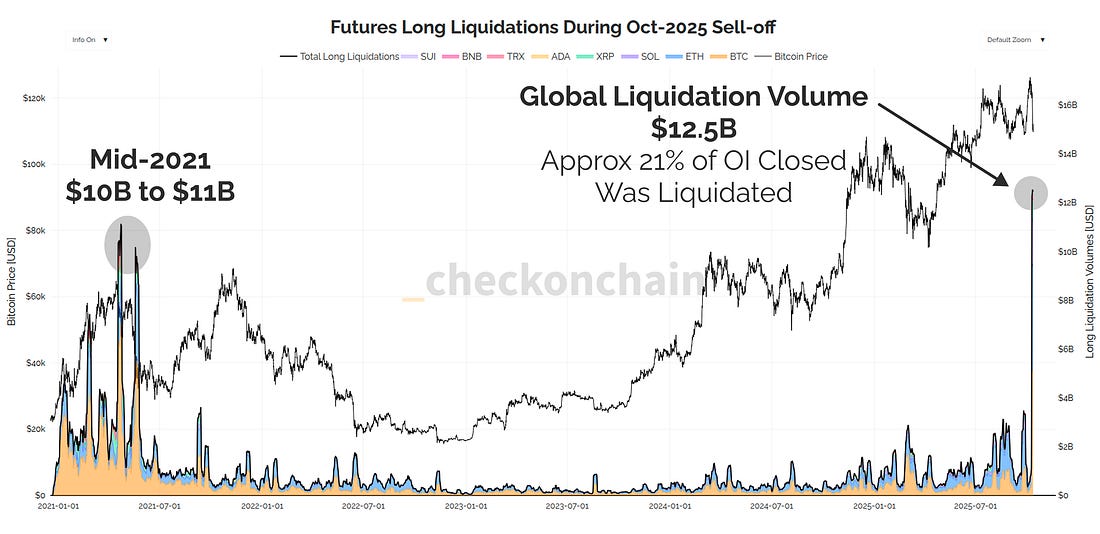

Truth be told, it remains to be seen whether these two events are appropriate comparison points, but we should all keep them in our back pockets as a potential outcome. Later in this piece, we will draw price lines in the sand for where this result may become increasingly likely. Returning to our current deleveraging event, the proportion of open interest decline associated with direct liquidations (meaning the trader’s entire account was wiped-out), was massive. Over $12.5B in liquidation volume occurred across the largest crypto-assets, representing around 21% of the total OI decline (the rest was from stop-losses and traders manually closing out their position, which didn’t zero their entire account). This exceeds the previous ATH liquidation volumes of $10B to $11B set in April and May 2021 as the bull market came off its first cycle high. Any way we want to slice it, the futures forest fire that has swept through was historic in size, and has no doubt cleared out a lot of the speculative excess.

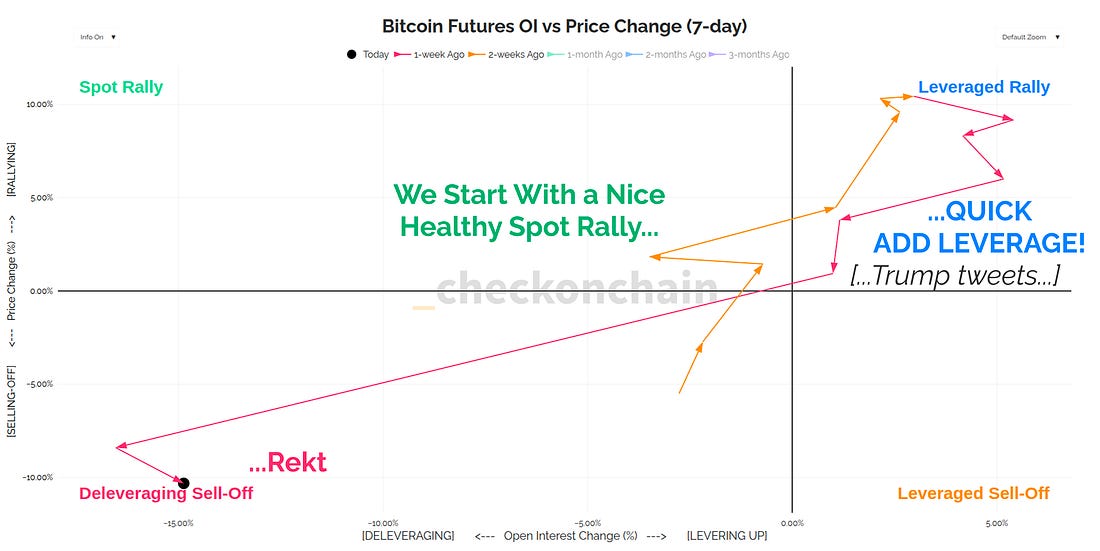

The chart below is a strange one, but I think it helps us visualise the investor behaviour that I would characterise as ‘speculative excess’.

The short summary is, as the price rallied two weeks ago, the market added more and more leverage, expecting us to fly to $1M… …Instead, we sold off -12%, and open interest declined by such a massive amount, I had to adjust the default view of this chart to fit it in. Moving forwards, a healthy market structure will see trading more in the top left quadrant, and less on the right-hand side. Lines In The SandSo, in the aftermath of a pretty significant event, how does this affect the setup for Bitcoin moving forward? Readers will know that we have retained a core bullish stance; however, with key lines in the sand for where things are likely to deteriorate. The framework by which we think about the rolling over of a bull into a bear is as follows:

With that as context, we can start by mapping out the key levels where we expect Bitcoin investor sentiment to experience marked shifts. Remember, these are not price predictions, but instead price levels where investors have historically changed their behaviour patterns in response to their portfolio performance.

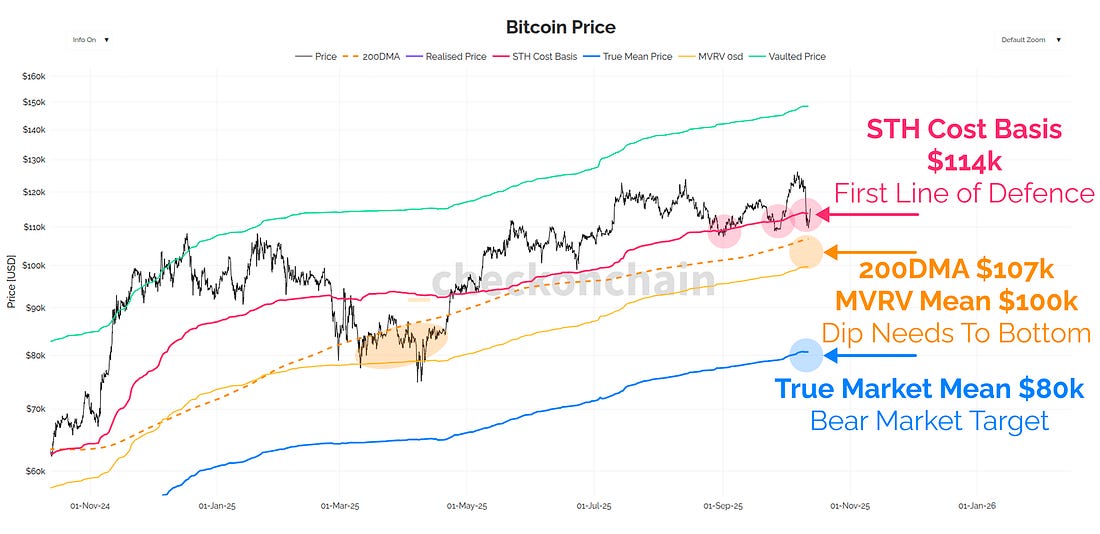

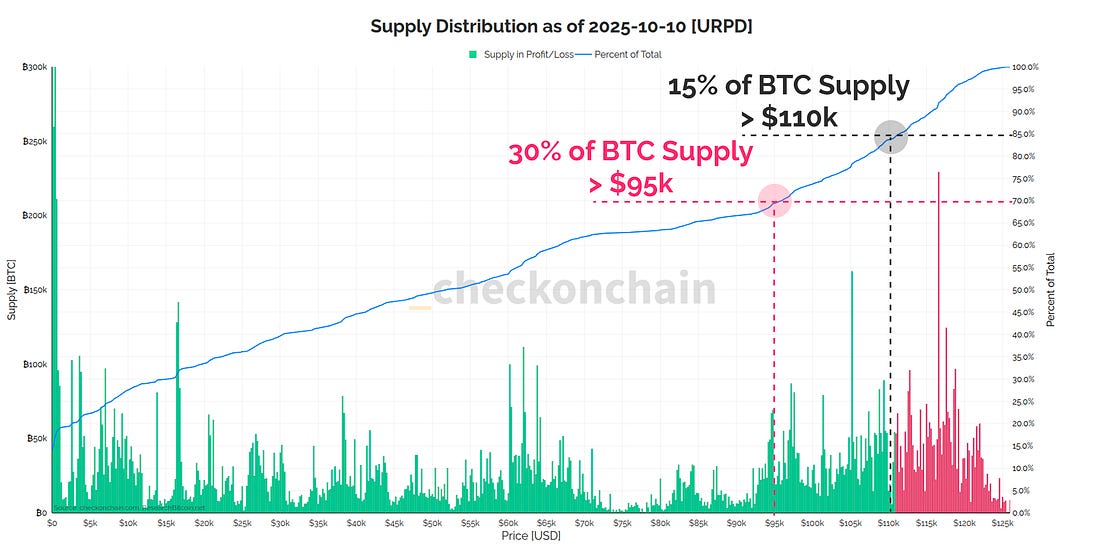

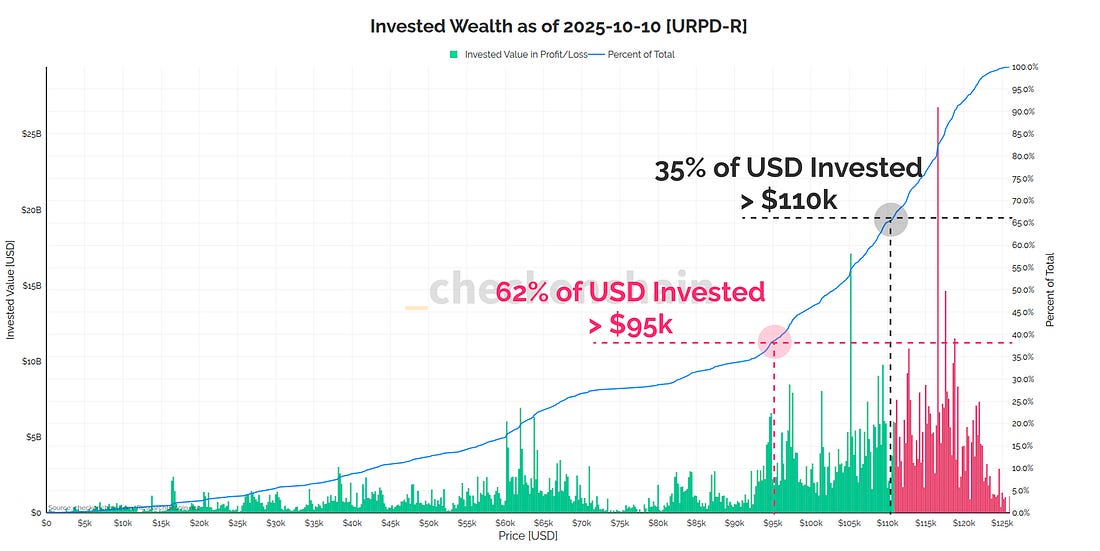

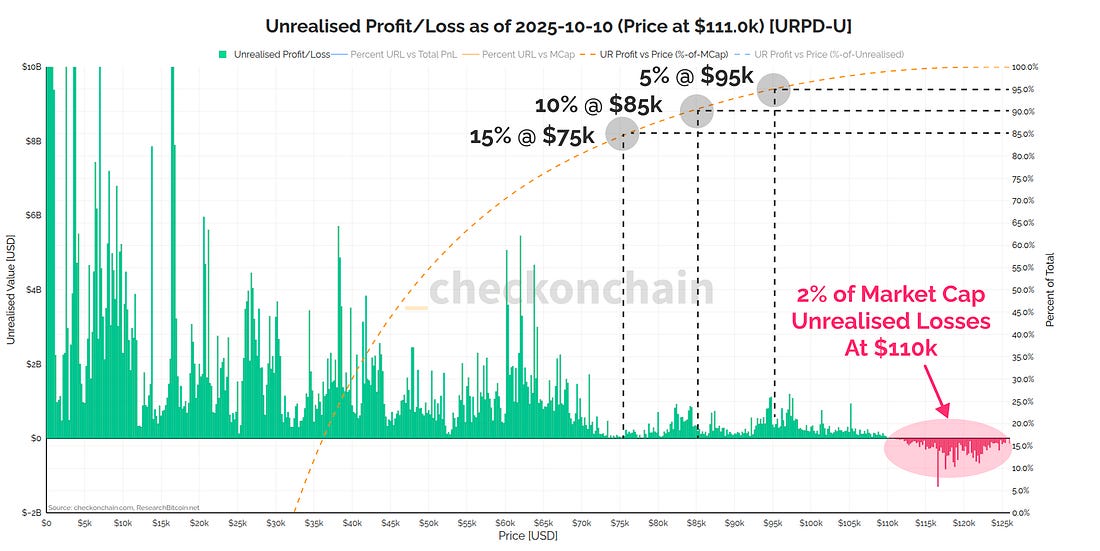

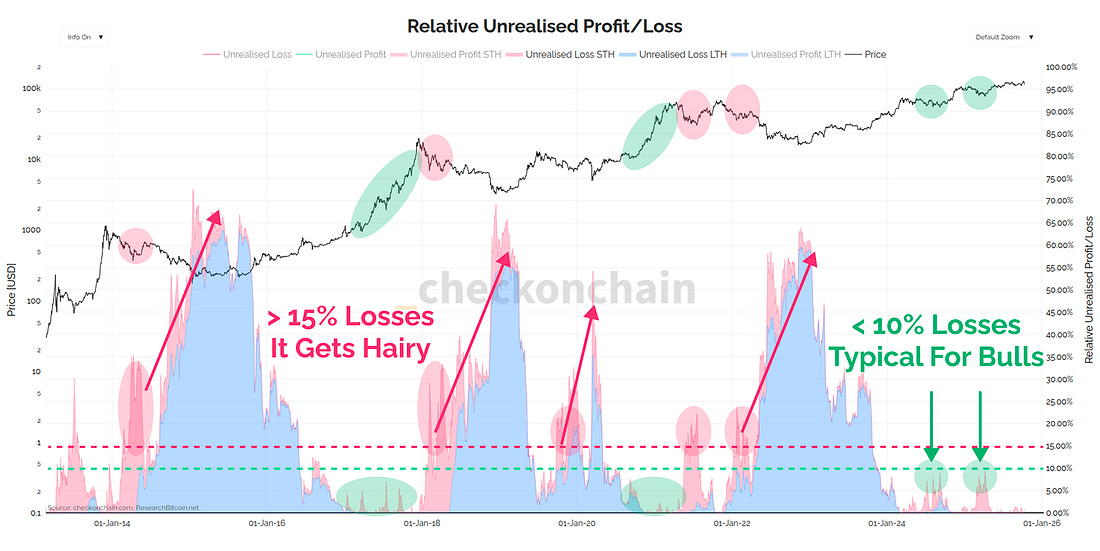

Whilst I’d rather we were higher, the fact of the matter is, the bears still have not taken us below the bulls first line of defence (the STH cost basis) on a serious closing basis. We had a forest fire…but our cabin in the woods still stands. If we look at the distribution of the entire BTC supply vs price, we can start to see why these price levels are quite important. Over 30% of the Bitcoin supply has an on-chain cost basis higher than $95k, and 15% of it was acquired above $110k. This is by far the largest zone of supply cluster that is relevant to us, because the next largest one is all the way back in the 2024 chopsolidation range, between $55k and $75k. I’m sure most of us would rather not see Bitcoin trading back down at those levels. Now, whilst the chart above is in BTC terms, most people still think about their portfolio value in terms of fiat currency (rightly or wrongly). As a result, people will naturally anchor to how much they invested, and less so to the number of coins held. The chart below shows each coin in the supply, except that we have weighted them by the price when they were acquired (think the USD value invested). From this vantage point, it becomes very clear why $95k is the most important price level to hold, because over 62% of the dollars ever invested in Bitcoin are above that price level. This is Bitcoin’s new home, and if you can imagine how nasty sentiment would get if all of those coins fell underwater…it would likely get pretty rough. Below $95k, Check the Analyst would struggle to classify the market as anything other than Top Heavy, and it is my view that this would start to heavily resemble the May and Dec 2021 crash events. Since the price is currently trading at $115k at the time of writing, we still have a buffer zone between here and $95k (although it is only $20k, and a -18% move below us). This is where those other price levels of $105k and $100k come into play, as they act as the ‘midpoint’ of the current supply distribution, and assuming we can hold above those levels, bull market sentiment should remain largely intact. However, if we were to break down to $105k…and then $100k…suddenly $95k isn’t that far away, and more and more people will start seeing a growing red number in their portfolio. If we did reach $95k, the total volume of unrealised losses held across the market would equal 5% of the Bitcoin market cap, compared to the 2% we are at today. Bull markets of the past have tended to meet their end whenever unrealised losses spike above 10% of the market cap, and we touched that upper bound in both 2024 and 2025. If you can recall, those events also had people calling for the end of the cycle, and the start of a bear market. Whilst they were ultimately proven wrong about that, it does go to show how ‘in the gutter’ sentiment can be at an unrealised loss level of 10%. The risk is, should the price fall below $95k, losses accelerate quickly, and since we don’t have a huge amount of historical support until $75k…well…you can probably see where I am going with this. I expect sentiment to get increasingly nasty below $95k, and as a result, I would really rather the bulls step in before that, so I don’t have to put this thesis to the test. So that brings us to the final chart, where we can summarise my current thinking about the key lines in the sand. These levels align both from an on-chain perspective, but also from a technical analysis perspective using the volume profile:

However…it’s not all bad news. These levels obviously map out a bear case scenario, and we must be very conscious that this is only one potential outcome. By the same note, a break above $118k would put us above the top-most volume point of control, and if cleared, would be the second time we have survived a failed ATH break below it. If we break above $118k, I believe we’re off to the races, and I stand by my previous post, noting that we have earned a serious shot at $150k. What I will leave you with is one final idea. I don’t think we chop sideways in the weeks and months ahead. I think the market is primed and ready to trend in a big way. If we go lower, I think we go a lot lower. If, on the other hand, we go higher…I think we go a lot higher. It’s time to rock and roll, and the next set of these major price levels we bust through, I believe defines the next major trend. I’m impressed we only traded down -12% on this move, but the time is certainly now for the bulls to step in. Seatbelts on.

Concluding Thoughts from CheckonchainIt is always a pleasure to collaborate with The Bitcoin Layer team, and they always bring a unique perspective to the macro and liquidity landscape that we really need as Bitcoiners. Bitcoin is a macro asset, and every man and his dog has been watching the price chart like a hawk over the weekend to see what might come next for their portfolio. Bitcoin is increasingly linked to the wider markets, and signs of weakness in equities would no doubt ripple into Bitcoin markets as well. I already think gold has shown us where this road leads (much higher). But I am conscious that further weakness in Bitcoin may be telling us the road to get there could be a bumpy one. We have a positive liquidity tailwind, and the bears haven’t proven their case just yet. Strap in. Thanks for reading, James

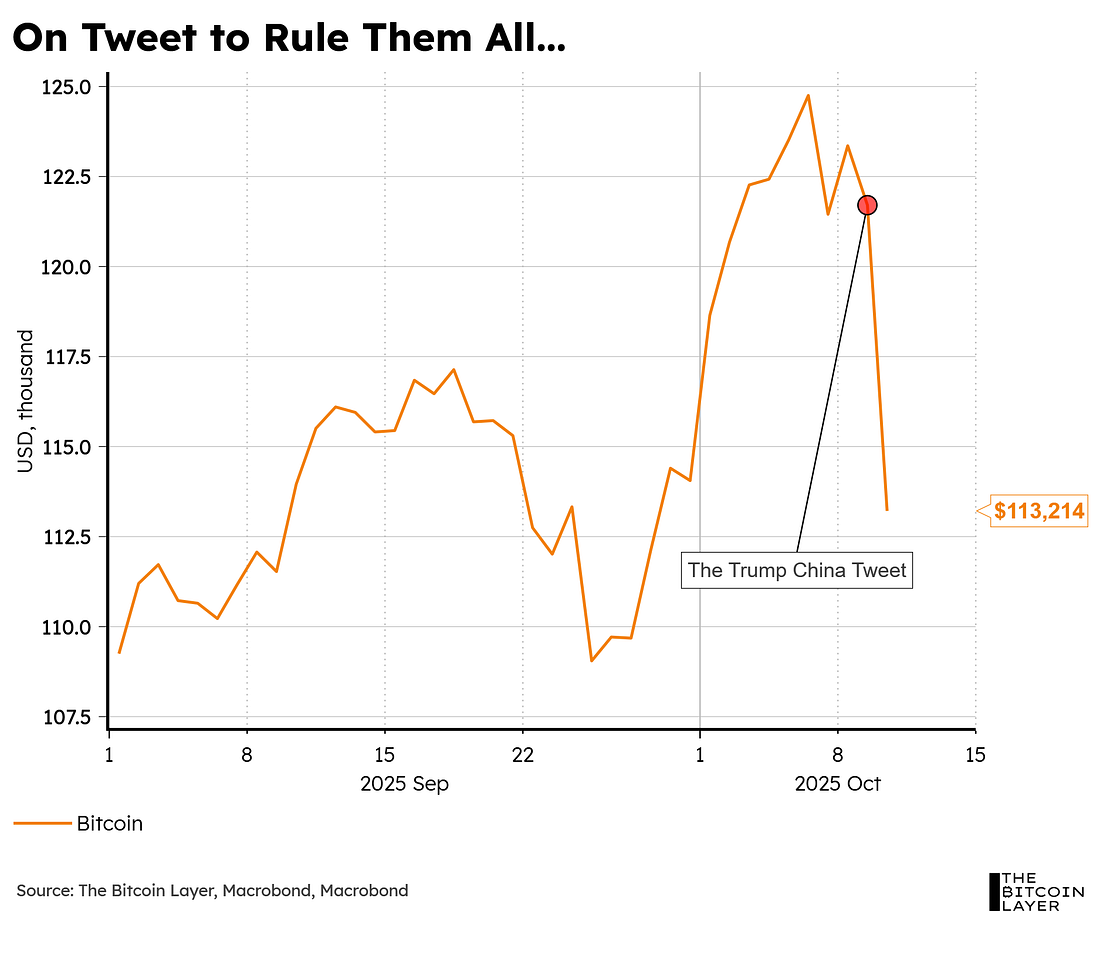

Once again, thanks to the Checkonchain team for the in-depth on-chain analysis. We will also be extending a 7-Day Free Trial (available for 48 hours) as our way to commemorate this collaboration: Onto our analysis: We are finally right in the middle of the long-awaited Uptober, and although bitcoin started the month on an extremely high note, President Trump had different plans (as the Checkonchain team highlighted in their analysis above):

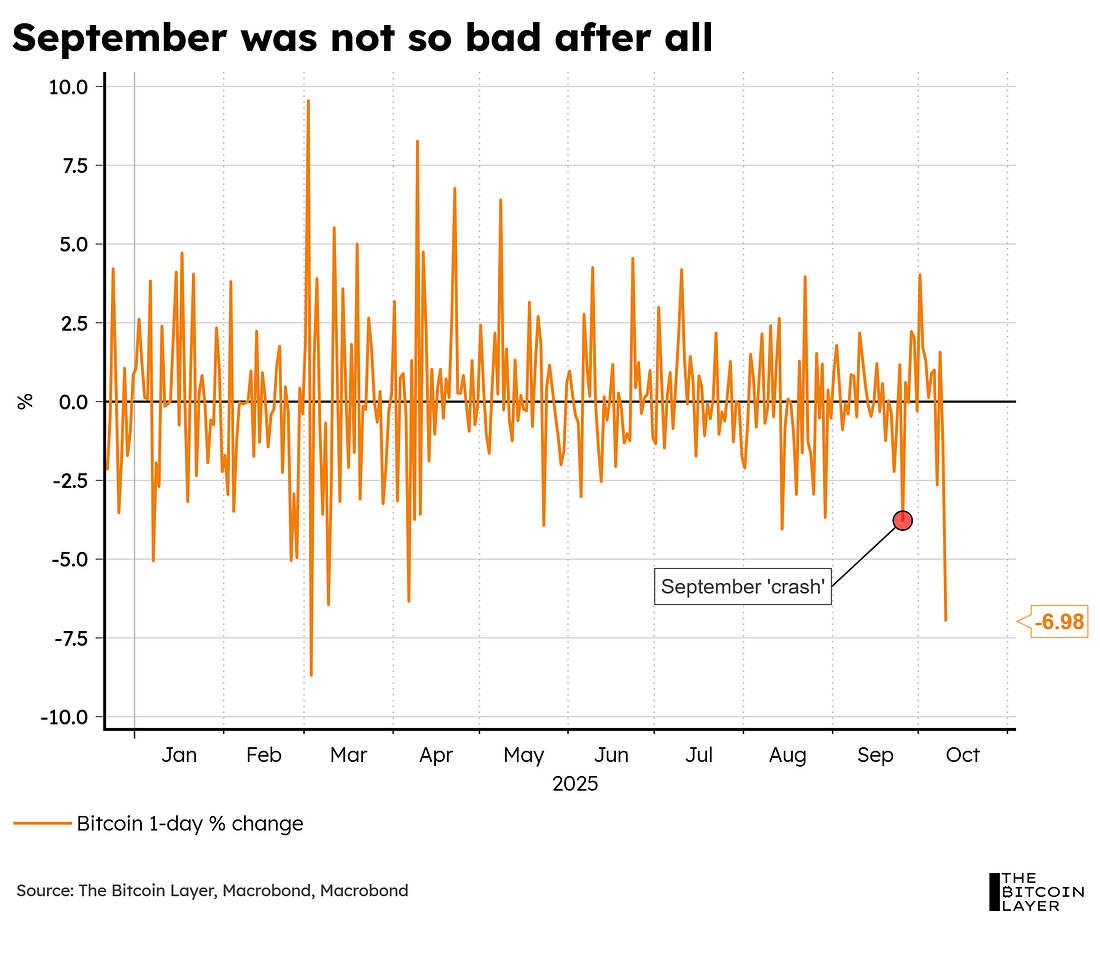

We are starting to seriously consider creating a Trump indicator alongside all of our TBL Liquidity metrics, but that’s a topic for another day. For now, suffice it to say that the roaring start to the month of October has been set back by, as Joe Consorti puts it, one of the largest nominal flash crashes in the orange coin’s history, with $278B wiped out in less time than it takes to watch an episode of your favorite Netflix drama. Just a few weeks ago, we were all talking about a 4% crash, which is looking puny right about now:

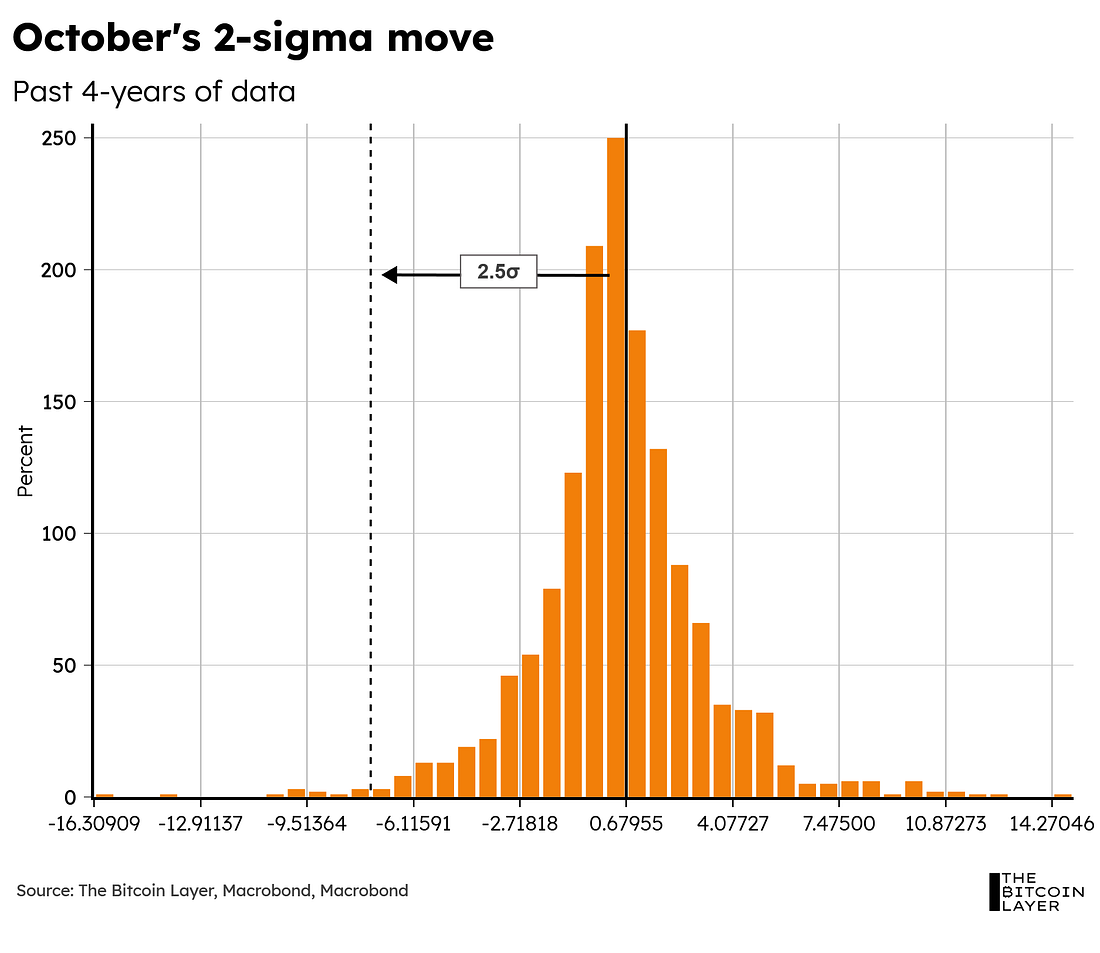

Looking back at the last 4 years’ worth of daily observations, Trump’s tweet ended up being a 2.5-sigma move for bitcoin:

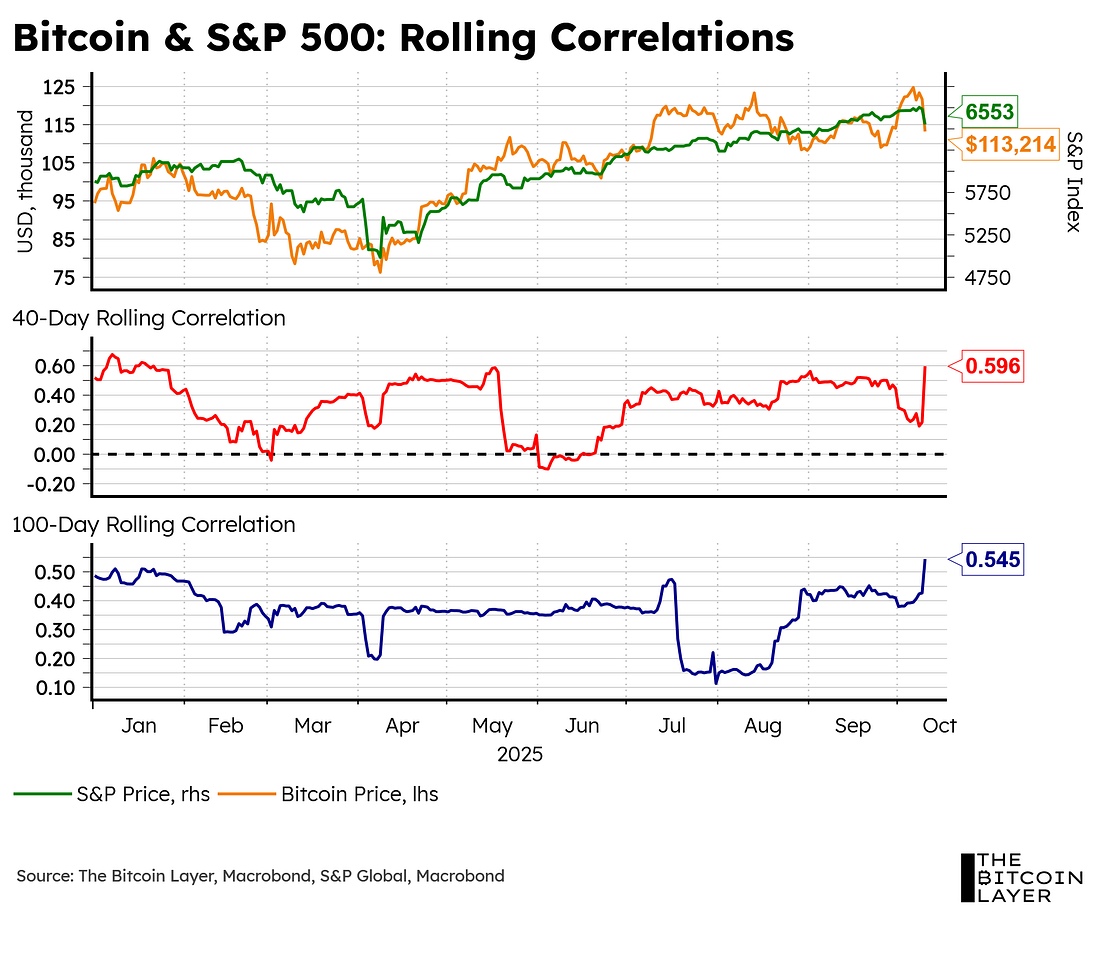

Perhaps this flash crash is a perfect example of just how exposed bitcoin is to more widespread market risks. That is, when correlations with the stock market are high (which they have been on a historical account)…

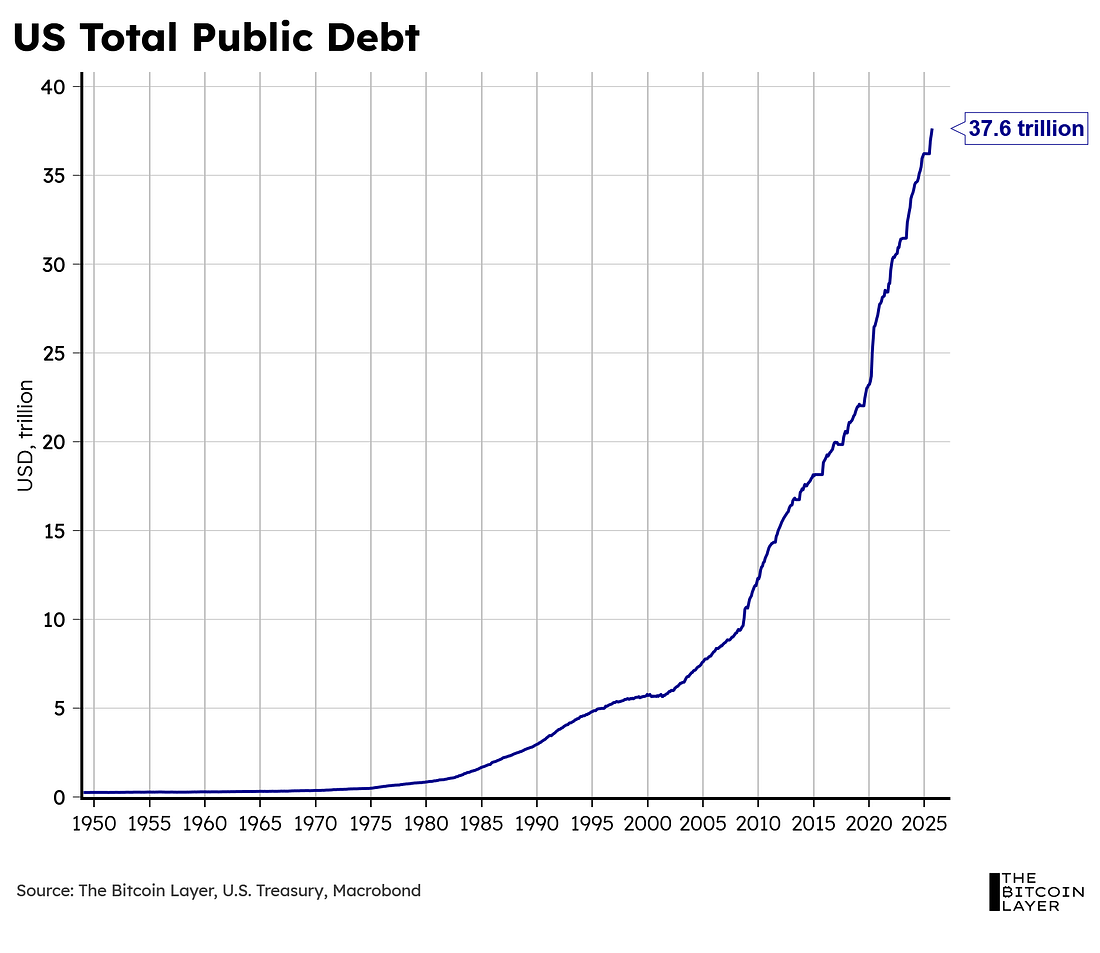

…that means more exposure to knee-jerk market reactions, such as those we’ve seen this year following Trump’s tweets. But enough of the doom and gloom. Let’s step away from daily moves and look now at the bigger macro picture. TBL LiquidityAs you’re all aware, US Treasuries play an essential role in today’s financialized economy, and whether we like it or not, they are scarce assets (...yes, we are aware of this chart):

Why are they scarce? Despite an insurmountable level of debt, U.S. Treasuries are still considered by many to be the risk-free asset of the world. Furthermore, each Treasury is its own individual asset with a unique CUSIP and characteristics. Unlike the fungibility of Apple stock—whereby exchanging one Apple stock with another leads to holding the same asset—exchanging one Treasury for another doesn’t exactly work like that. If the US Government issues a 10-year note, while at the same time, there is an old 30-year bond that was issued 20 years ago and therefore has 10 years left to mature, these two Treasuries may match in maturity, but that doesn’t make them fungible. Over 70% of the trading volume in the US Treasury market takes place in on-the-run securities, which are the most recently auctioned Treasuries (source). And while the story of how that came to be is beyond the scope of this article, the key takeaway here is that, in a self-fulfilling manner, financial infrastructure and liquidity have concentrated around newly issued Treasuries—put simply, everyone wants the new ones because there’s just a lot more infrastructure, and therefore, more you can do with them. On-the-runs are also easier to post as collateral in repo transactions, even though technically all Treasuries are supposed to warrant the same haircut as each other—bilateral repo participants don’t always agree with the idea that a deep off-the-run Treasury equals an on-the-run one. Ergo, US Treasury Buybacks. Given the high spreads and illiquidity behind old Treasuries, older issues add frictions to the market (clogging balance sheets and, therefore, liquidity), so removing these older issues from the market leads to reduced frictions and fewer hiccups overall. Anyway, where were we? Oh, that’s right! The scarcity of US Treasuries—specifically, on-the-run Treasuries. The reason we mention that is because of something known as the circulation of collateral. As a result of the aforementioned scarcity, as well as high demand, US Treasuries are prime collateral, leading a single US Treasury security to circulate around multiple balance sheets. The Fed puts it best:

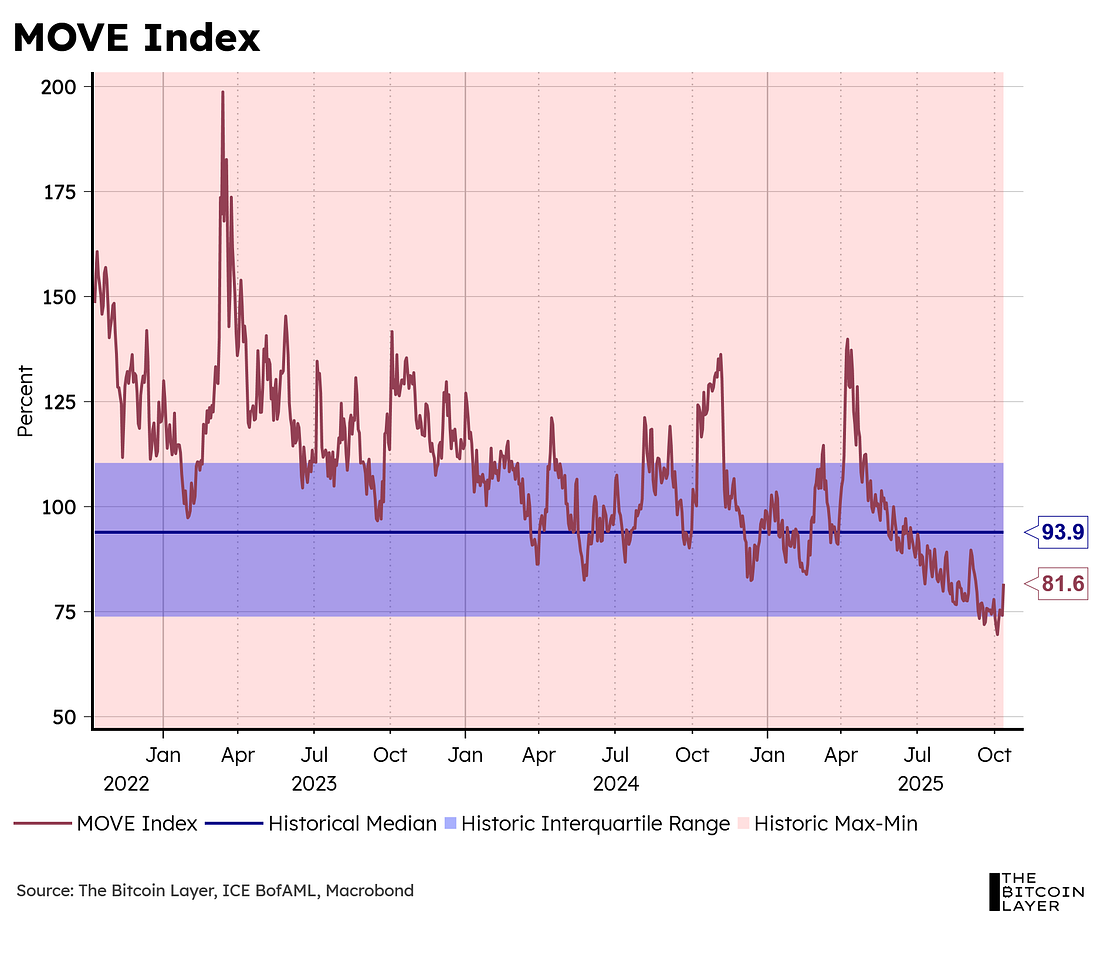

In a recent piece, we explained what the collateral multiplier is in more detail, but to keep things simple and in line with this section of the article (in case you forgot, we’re talking about TBL Liquidity), when a single Treasury is rehypothecated multiple times in funding transactions (repo markets), that is an indication that US Treasuries are extremely prime collateral, which is why a greater number of funding transactions are taking place on a fixed number of Treasuries (i.e., a high collateral multiplier). The only reason participants would be willing to borrow against borrowed collateral (rehypothecation) is that the collateral is extremely stable. In comes the MOVE Index. Bond market volatility affects the collateral multiplier directly, and therefore risk assets like bitcoin, because when it rises (MOVE Index up), you get two things:

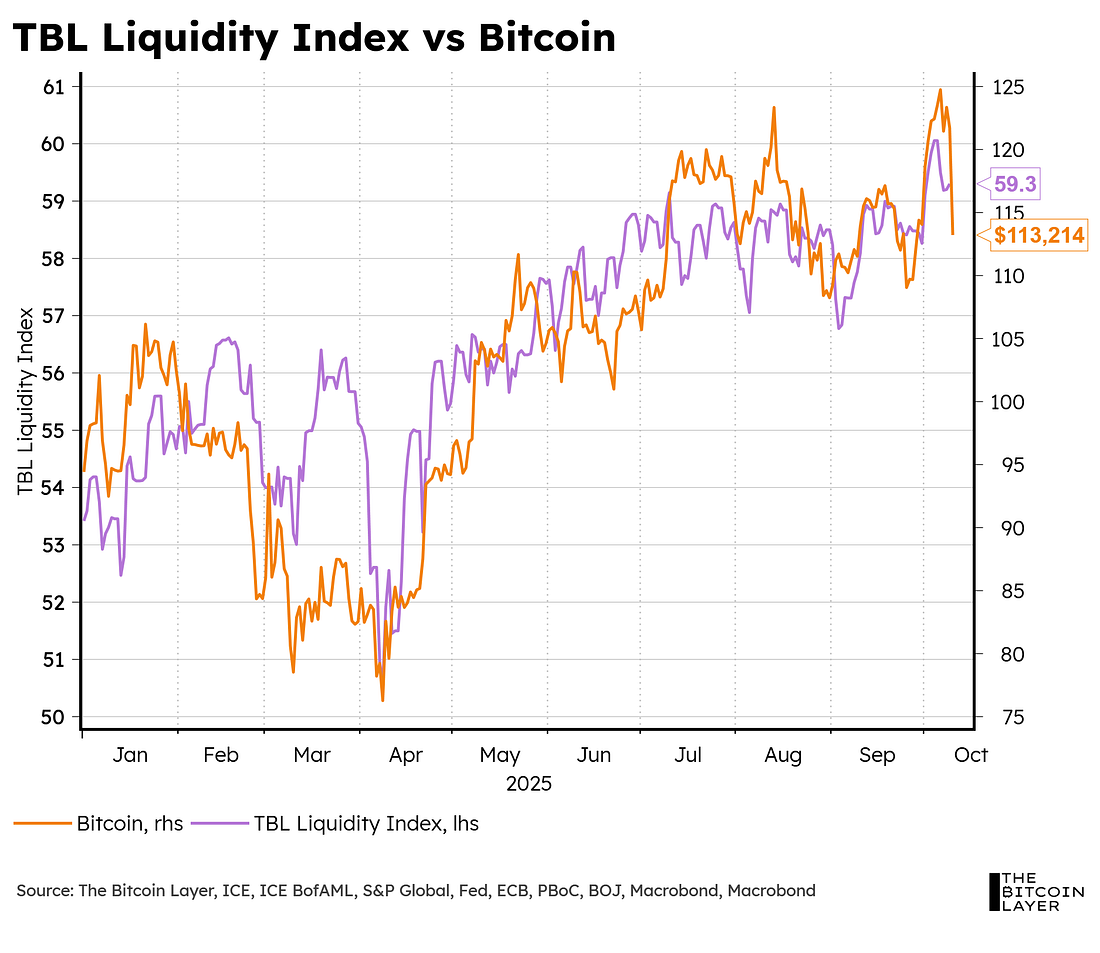

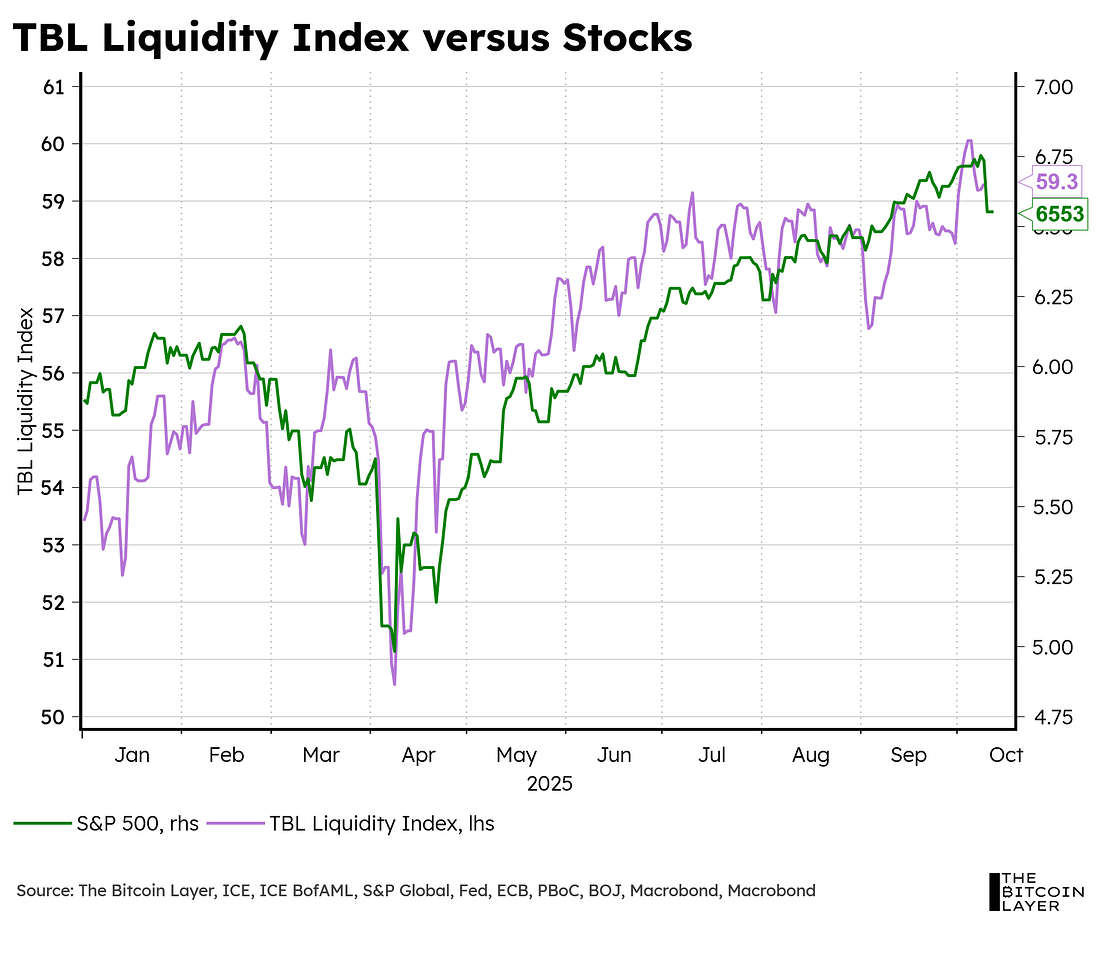

The net effect is that risk asset positions financed via repo (with Treasuries as collateral) fade, and risk plummets. Herein lies the importance of bond volatility to our TBL Liquidity Index—specifically, its opposing effects on our index. Just look at TBL Liquidity next to both bitcoin and the S&P 500 over the past year as bond volatility has decreased (which, in our framework, is positive for liquidity):

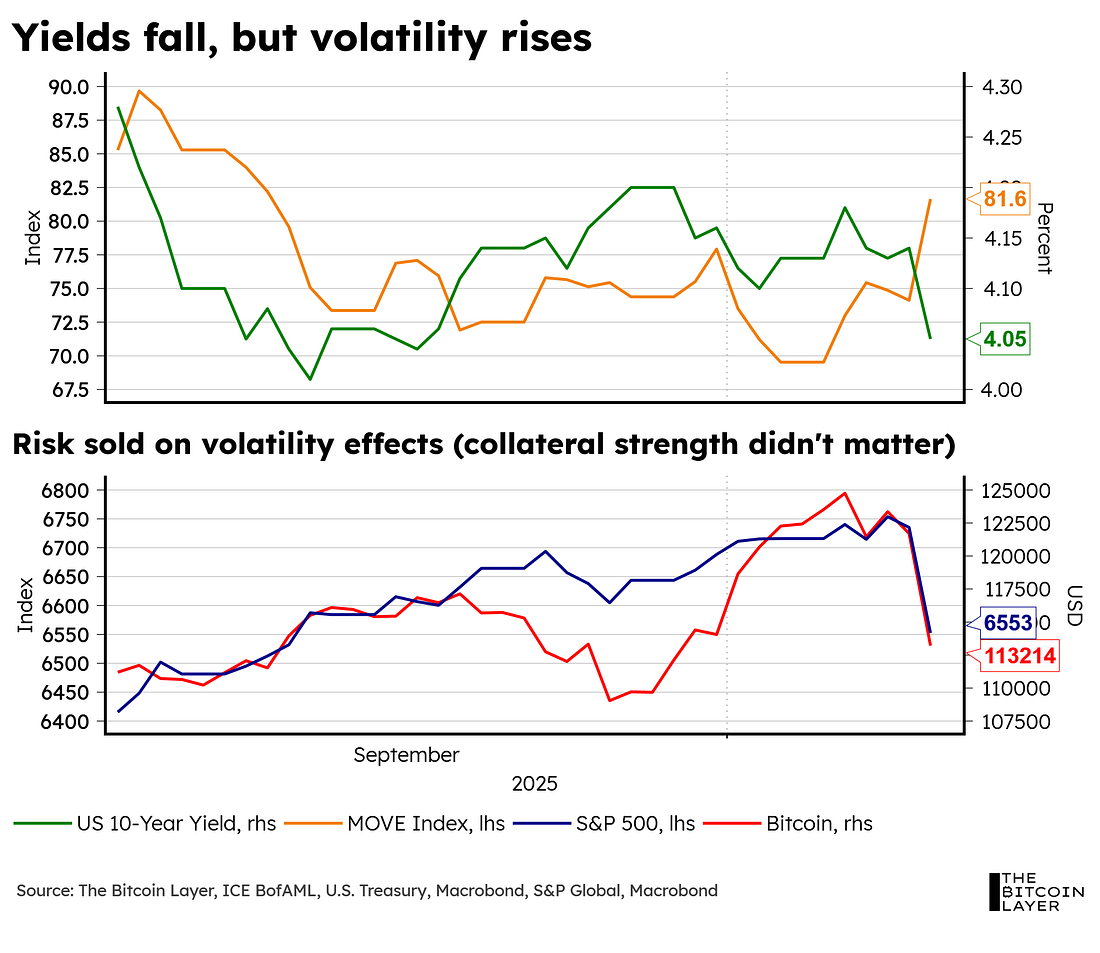

Now, one thing that’s important to note here is that volatility is what matters in these financing transactions. In other words, if the collateral increases in value (Treasuries rise in price—yields fall), but does so in a violent way, a lender in repo markets will still demand a higher haircut. These are short-term loans with terms set ex ante, so if a lender doesn’t know where the Treasury will be tomorrow, that uncertainty affects the loan terms more than whether the collateral’s value ultimately rises or falls. This is why volatility measures like the MOVE index are more relevant for understanding repo market conditions (and liquidity) than the direction of Treasury price movements. A prime example of this hierarchy of importance took place yesterday: despite the underlying collateral becoming more valuable (yields down), bond volatility rose, which negatively affected the collateral multiplier, which hurt liquidity, and risk sold (chart below):

Outlook for UptoberThat said, our outlook for October is still bullish. Zooming out, we have 4 things going our way: First, volatility remains at historically low levels, which is what has been leading our overall bullish liquidity narrative in the first place:

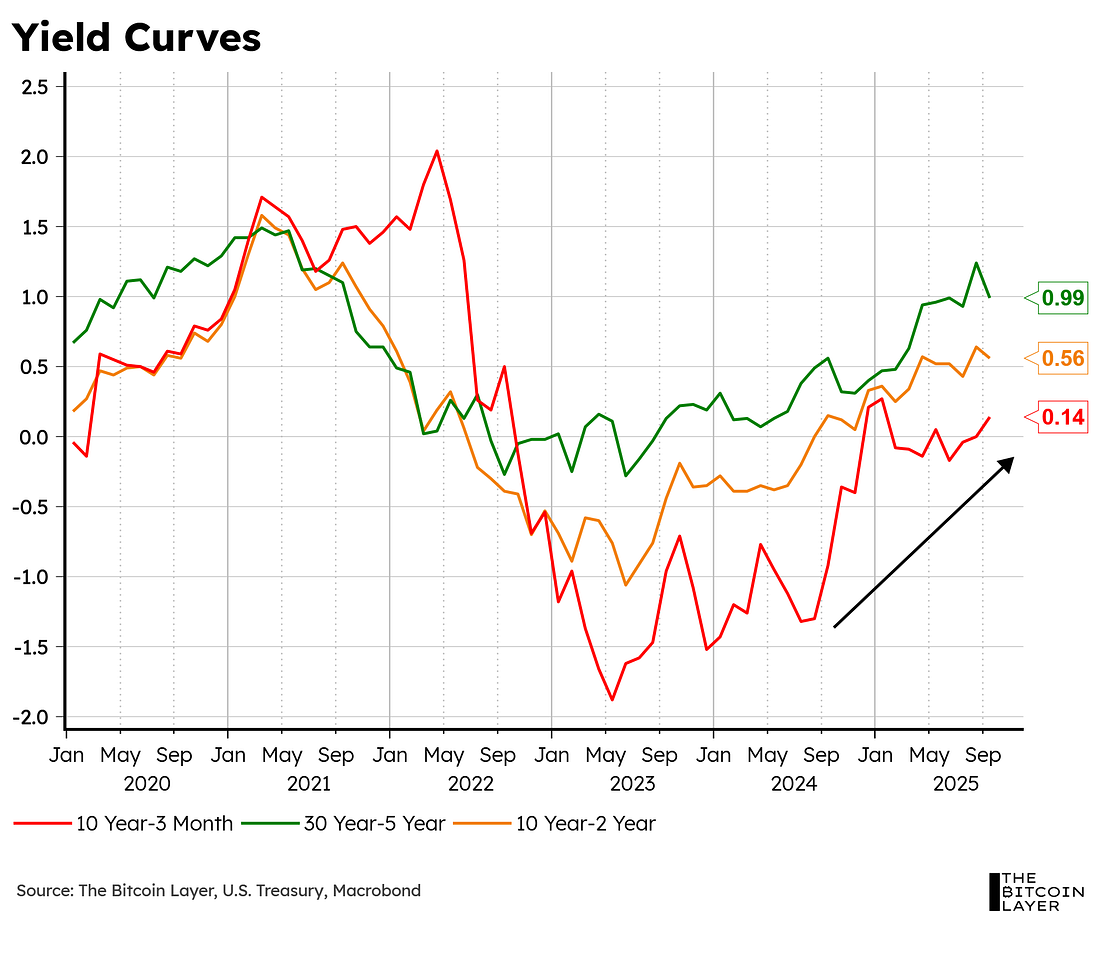

Second, as the current administration fixes its mind’s eye on what people care about the most (inflation), low rates may continue to be the target of some more Trump-Tweet scrutiny, with a special focus on the back-end of the curve due to mortgage rates. This creates US Treasury tailwinds, which, over time, bleed into the system in the form of lower haircut benchmarks (positive for liquidity). Third, steeper curves may lead to better numbers in banks’ earnings reports over the next few weeks, which may help a V-shape recovery in the overall market:

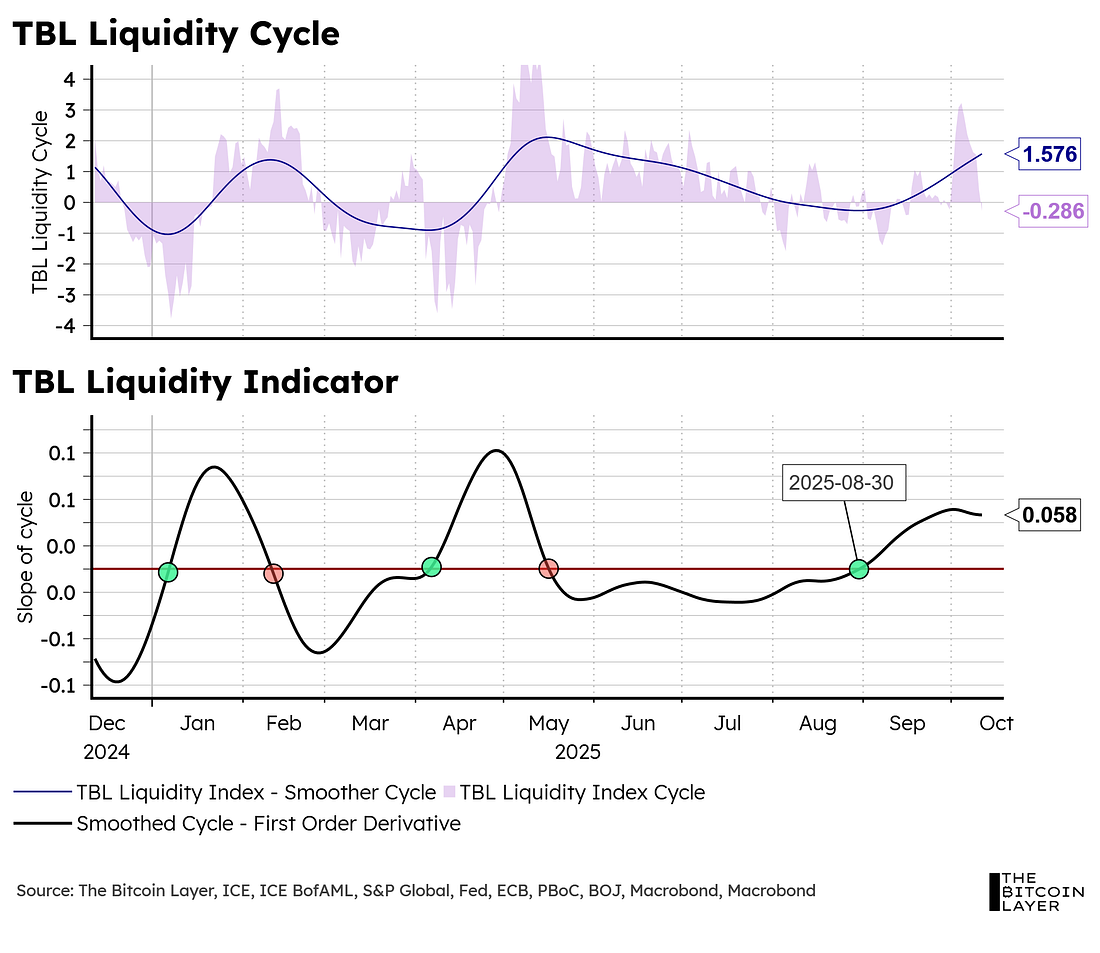

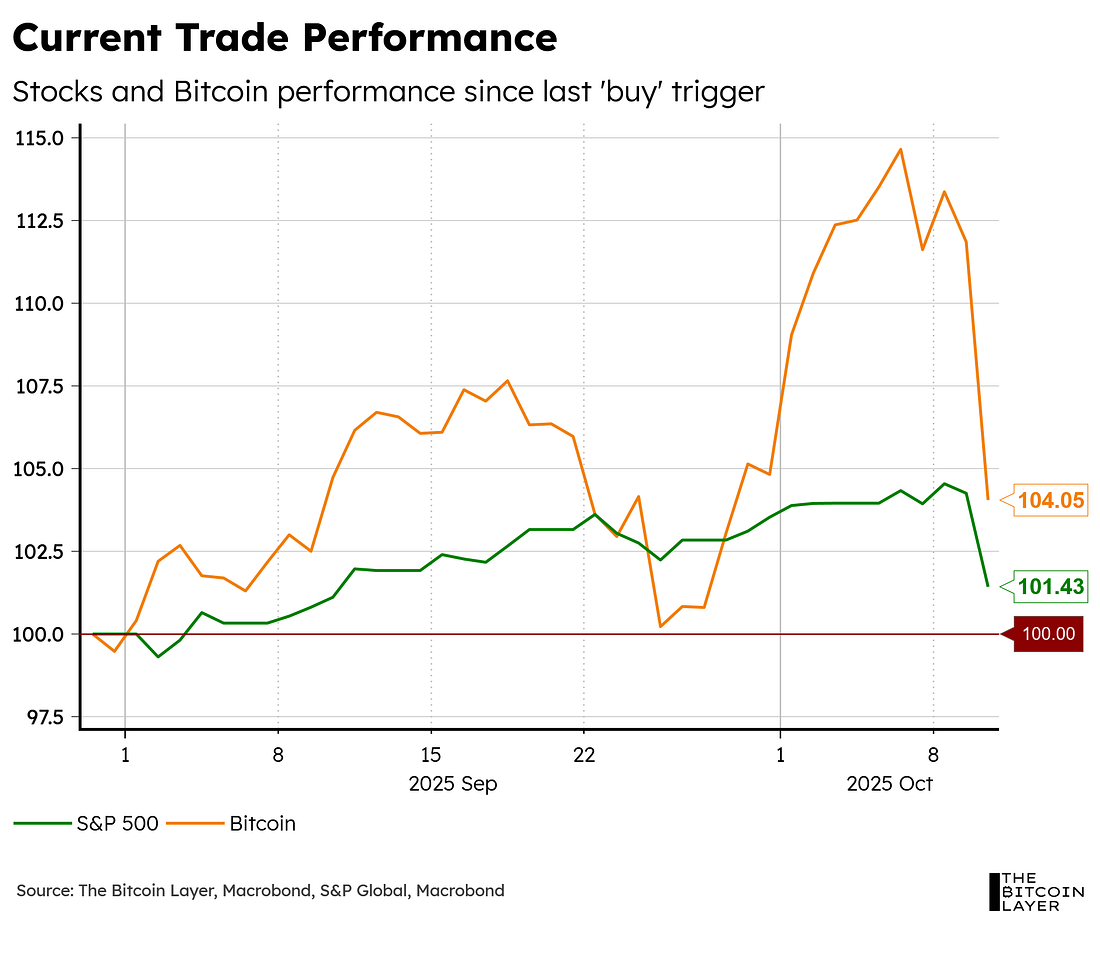

This, as seen from the correlation chart above, could bleed into a V-shape for bitcoin as well. Lastly, despite the government shutdown, the market remains fairly certain on 2 cuts this year, which again provides tailwinds in the overall market for risk. We continue to rely on our proprietary TBL Liquidity Indicator for our buy-and-sell signals, whose latest buy signal remains green in both stocks (+1.43%) and bitcoin (+4%):

Overall, our narrative for October remains bullish—only if Trump has mercy with his tweets. This Article Was Brought To You By:

The End of Fiat Retirement: Navigating Economic Uncertainty with a Bitcoin Retirement Plan Is the fiat retirement system sinking? With markets uncertain, layoffs on the rise, and monetary policy shifting, it might be time to rethink how you protect your long-term savings. On October 28 at 12 PM CT, Mark Moss and Unchained’s Jeff Vandrew will cover:

Learn how bitcoin can protect your purchasing power, strengthen your retirement plan, and offer a level of sovereignty no other retirement asset can. Tuesday, Oct 28 at 12:00 PM CT — online, free to attend.

We are also happy to announce our newest sponsor this month: Arch Lending! At TBL, we help you decode Bitcoin’s macro trends and give clear market signals—holding Bitcoin is just the beginning. Arch lets you borrow against your Bitcoin—unlock cash without selling:

Stay long, stay liquid. Use code “Nik” for 0.5% off interest rate for 2 years.

Blockstream Jade Plus is the easiest, most secure way to protect your Bitcoin—perfect for beginners and pros alike. With a sleek design, simple setup, and step-by-step instructions, you’ll be securing your Bitcoin in minutes. Seamlessly pair with the Blockstream app on mobile or desktop for smooth onboarding. As your stack grows, Jade Plus grows with you—unlock features like the air-gapped JadeLink Storage Device or QR Mode for cable-free transactions using the built-in camera. Want more security? Jade Plus supports multisig wallets with apps like Blockstream, Electrum, Sparrow, and Specter. Protect your Bitcoin, sleep better, stack harder. Use code: TBL for 10% off. Looking for an Onchain Data API?Checkonchain friend The Bitcoin Researcher has just rolled out a new API for Bitcoin onchain data which has just about every metric you’d want. I’ve had a few folks reach out looking for API access, and I highly recommend checking this service out if you’re interested in playing with the underlying data feeds.

Thanks for reading The Bitcoin Layer — for access to all content, upgrade to paid!

|

Monday, October 13, 2025

What TBL Liquidity and On-Chain Metrics Are Saying with Checkonchain

Subscribe to:

Post Comments (Atom)

Popular Posts

-

Watch now (42 mins) | Discussing the strength latest risk asset rally | Michael Howell live Q&A next week ͏ ͏ ͏ ͏ ...

-

Citizen Brief: gm, it's been a brutal 2025 for crypto's top tokens, but not everything is looking red on the 90-day charts...

-

With 95% of supply already mined, Bitcoin’s price is now driven more by global liquidity and institutional flows than halving cycles. ...

-

Figuring out bitcoin’s next move and TBL Pulse Webinar coming up ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ...

-

Wednesday, May 6th at 2:00 PM EST. Free to attend. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ...

No comments:

Post a Comment