Decoding the SEC’s Token Taxonomy gm Bankless Nation,

The SEC is ready to talk about more tokens that aren’t securities; it’s more cagey about the reverse. Today's Issue ⬇️ - ☀️ Need to Know: UK Crypto Donation Ban?

The UK takes aim at political donations made with crypto. - 🗣️ Analysis: Decoding the SEC’s Token Rules

How the SEC's new framework applies to your bags.

Sponsor: MegaETH — Crypto has new apps, finally.

. . . NEED TO KNOW UK Crypto Donation Ban? - 🇬🇧 United Kingdom Bans Crypto Donations to Political Parties. The island nation is also capping the donations of British citizens living abroad as part of an effort to prevent foreign financial interference.

- 🔷 Bitmine Launches Institutional ETH Staking Platform. Bitmine's MAVAN platform launches with 3.14M staked ETH, targeting institutional clients and projecting nearly $300M in annual staking rewards.

- 🟨 Binance Requests Market Maker Transparency in Updated Trading Policy. The crypto exchange wants projects to detail their market maker agreements before launching or listing tokens.

📸 Daily Market Snapshot: Stocks and crypto inched higher as Trump seemed to signal ceasefire interest even as thousands of U.S. troops neared the Strait of Hormuz. | Prices as of 5pm ET | 24hr | 7d |  | Crypto $2.43T | ↗ 1.3% | ↘ 0.7% |  | BTC $70,974 | ↗ 1.3% | ↘ 0.4% |  | ETH $2,163 | ↗ 0.9% | ↘ 1.6% |

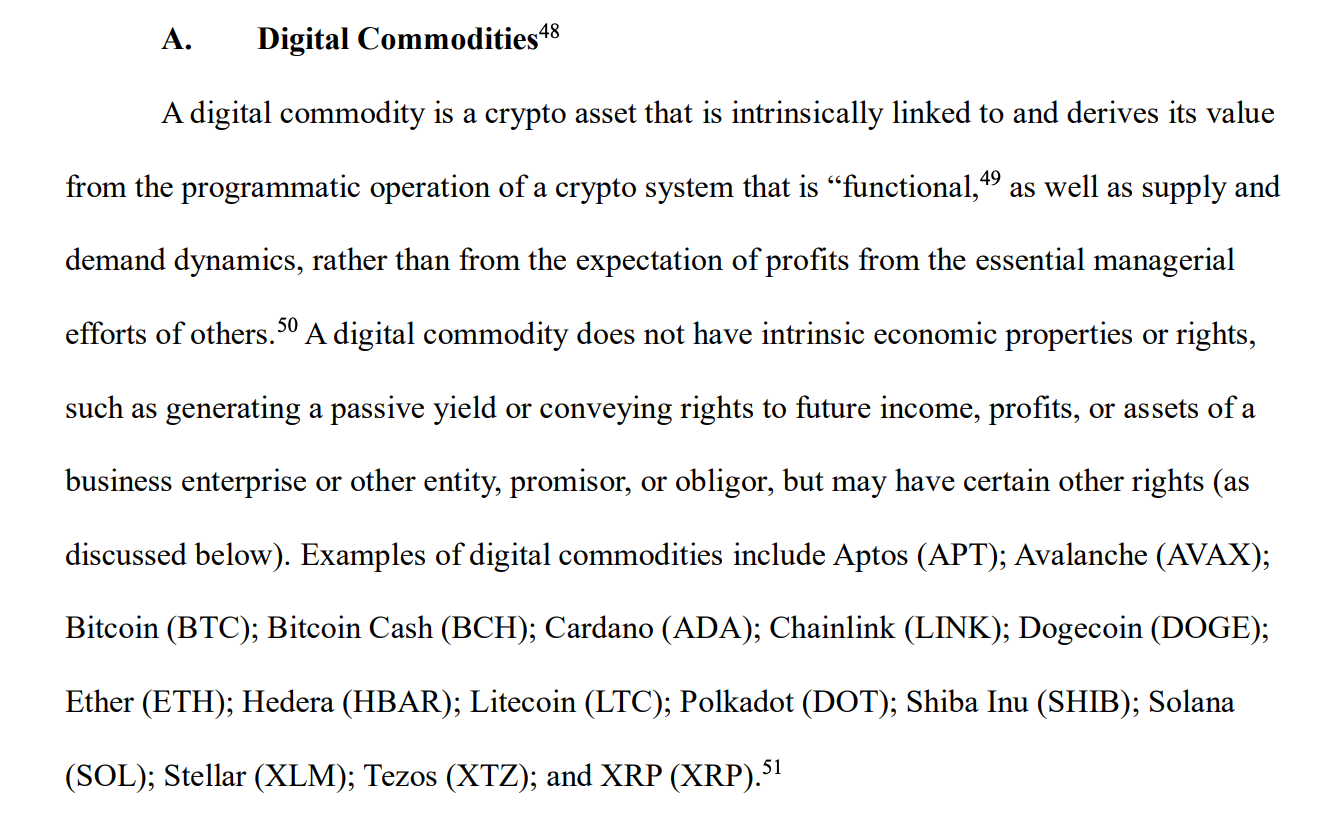

. . . ANALYSIS Decoding the SEC’s Token Taxonomy Last week, the SEC and CFTC teamed up to unveil landmark guidance, delivering a long-awaited joint interpretation detailing how and when federal securities laws apply to crypto assets. While the crypto industry has long operated in a legal gray zone, this new framework attempts to replace a portion of that uncertainty with a token taxonomy classification system, which helps distinguish how and when digital assets qualify as securities. Today, we’re unpacking this joint guidance and surmising how it may ultimately classify popular digital assets. 👇 🌾 Digital CommoditiesAccording to the SEC’s interpretative guidance, the “digital commodity” classification includes crypto assets that derive value from their “functional” role within a crypto ecosystem, as well as supply and demand dynamics. This purposefully broad definition captures the utility tokens of many established blockchain networks, with the SEC enumerating 16 distinct crypto assets that fall into this category, including: Aptos (APT); Avalanche (AVAX); Bitcoin (BTC); Bitcoin Cash (BCH); Cardano (ADA); Chainlink (LINK); Dogecoin (DOGE); Ether (ETH); Hedera (HBAR); Litecoin (LTC); Polkadot (DOT); Shiba Inu (SHIB); Solana (SOL); Stellar (XLM); Tezos (XTZ); and XRP (XRP). Although the SEC’s guidance lacks individual justifications for why these specific cryptocurrencies are classified as nonsecurity digital commodities, it emphasizes that each is not automatically considered a security, as none meet the legal definition of a “security.” The SEC claims it applied the term “digital commodity” in a strictly economic sense to describe typical asset characteristics of one category of nonsecurity digital asset. Still, the guidance asserts that any crypto asset (besides GENIUS Act-compliant stablecoins) can qualify as a true "commodity” under the Commodity Exchange Act, a designation that would trigger separate CFTC oversight and regulation. Other popular crypto tokens that went unmentioned by the SEC, but that also might qualify as “digital commodities” include: - BONK: a memecoin on the Solana network that has evolved various token governance and utility integrations since its inception

- CC: the native utility token of the Canton blockchain, used to trade, settle transactions, synchronize data, and transfer assets

- EIGEN: a restaking-based utility token within the EigenLayer ecosystem, used to provide economic security guarantees

- ETC: the proof-of-work version of Ethereum, an already SEC-designated nonsecurity digital commodity

- HYPE: the native gas and staking token of the Hyperliquid network, used to pay transaction fees and secure network operations

- STX: the native gas and staking reward token of the Stacks Bitcoin L2, used to pay transaction fees and secure network operations

- SUI: the native gas and staking token of the Sui network, used to pay transaction fees and secure network operations

- TAO: the native token of the Bittensor network, used to incentivize and reward machine learning contributions within a decentralized AI marketplace

- TRX: the native gas and staking token of the Tron network, used to pay transaction fees and secure network operations

- XMR: the native token of the privacy-focused Monero network, used to pay transaction fees and secure network operations

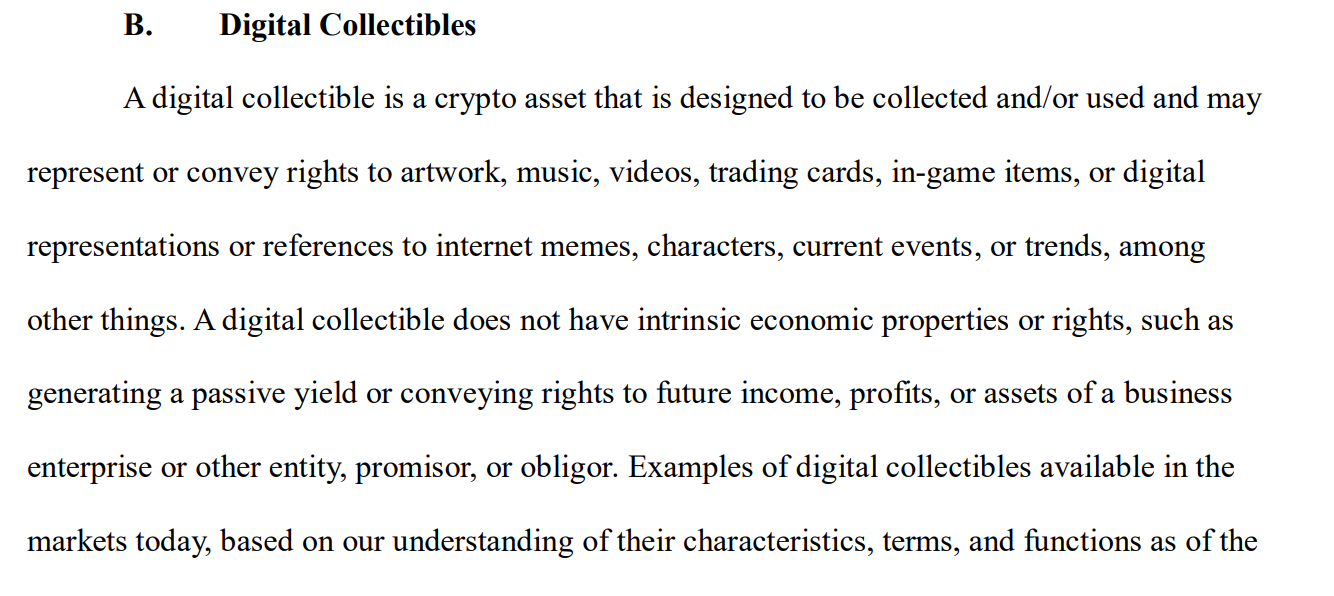

🎨 Digital CollectiblesFormer SEC Chair Gary Gensler famously failed to clarify before Congress whether a tokenized Pokémon card would be considered a security under federal law, suggesting that a definitive answer would require additional information. The crypto industry now seems closer to receiving its long-awaited answer. Newly proposed SEC guidelines suggest that a tokenized Pokémon card could be categorized as a "digital collectible,” however, additional information is still needed before certifying its nonsecurity status. This classification category applies to crypto assets intended for collection, encompassing those that "represent or convey rights” to artwork, music, videos, trading cards, in-game items, and previously defined memecoin. Similar to physical collectibles, digital collectibles do not provide holders with any ownership in business-like enterprises, even if holders own rights to commercialize the underlying intellectual property. As such, they are naturally considered nonsecurities. The SEC asserts that CryptoPunks, Chromie Squiggles, Fan Tokens, WIF, and VCOIN can be classified as digital collectibles. While the SEC categorizes memecoins as digital collectibles, the agency disclaims that these types of tokens can later transition into digital commodities once “functional" within an associated crypto ecosystem. Furthermore, the SEC explicitly notes that (as is the case with physical collectibles) that most fractionalized collectibles likely constitute securities, as purchasers depend on the managerial efforts of another party. Perhaps the need to physically custody a Pokémon card backing a tokenized version constitutes managerial efforts, triggering registration requirements under federal securities law? Popular crypto projects that went unmentioned by the SEC, but that also might currently qualify as “digital collectibles” include: - Beeple’s The First 5000 Days: the most expensive NFT ever sold, deriving value from its cultural significance, artist reputation, and historical importance in the NFT market

- PEPE: a meme coin inspired by internet culture, which derives value from its social sentiment and virality

- Pudgy Penguins and PENGU: a community-centric NFT and token brand focused around penguin-themed IP, with value driven by cultural relevance

- Quantum Cats: a Bitcoin Ordinals collection of on-chain digital artifacts, valued for their scarcity and status within the Bitcoin ecosystem

- Saga Monkes: a limited NFT collection tied to the Solana Saga phone launch, valued as a digital collectible due to exclusivity, early adopter status, and ecosystem affiliation

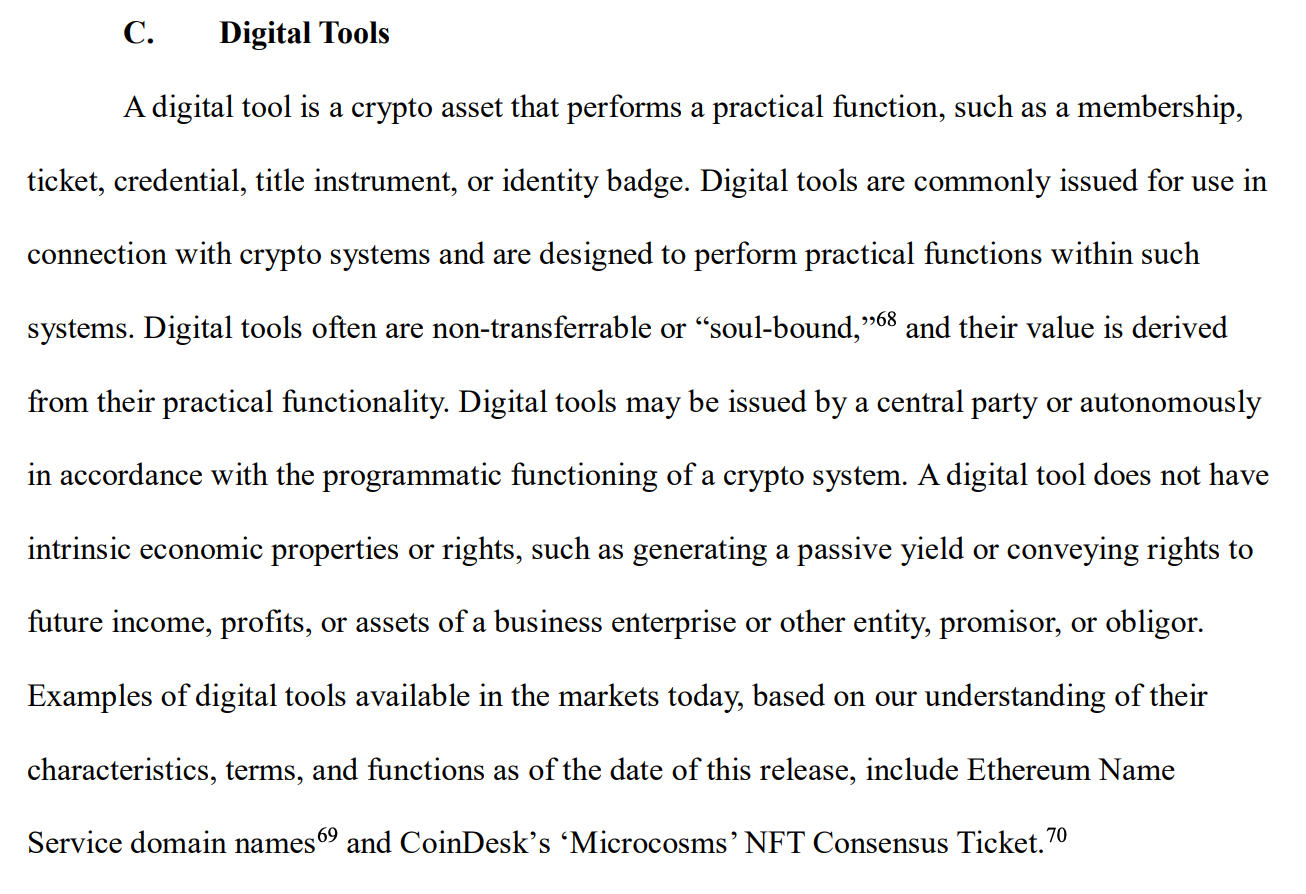

Digital tools are crypto assets designed to do something. While digital tools can hold inherent functional value, many also exist in “soulbound” formats, meaning they cannot be sold and remain permanently tied to a single user. Importantly, the SEC disclaims that digital tools cannot have, “intrinsic economic properties or rights, such as generating a passive yield or conveying rights to future income, profits, or assets of a business enterprise or other entity, promisor, or obligor.” The SEC identifies a range of digital tool use cases, including memberships, tickets, credentials, title instruments, and identity badges, and its guidance classifies Ethereum Name Service domain names and CoinDesk’s “Microcosms” NFT Consensus Ticket as digital tools. Additional digital assets that might satisfy the criteria of “digital tools” include: - FanDome NFTs: a collection of comic book-inspired NFTs distributed for free to attendees of DC Comics' FanDome virtual conference in 2021

- POAPS: digital badge generated in NFT form, minted on the blockchain to prove attendance at real-world or virtual events

- Propy NFTs: a digital representation of legal ownership in a physical property, stored on the blockchain

- VeeFriends: a collection of NFTs created by Gary Vaynerchuk, which offer access to exclusive events, including the VCON conference

- World ID: a soulbound “proof of personhood” credential issued by Sam Altman’s World

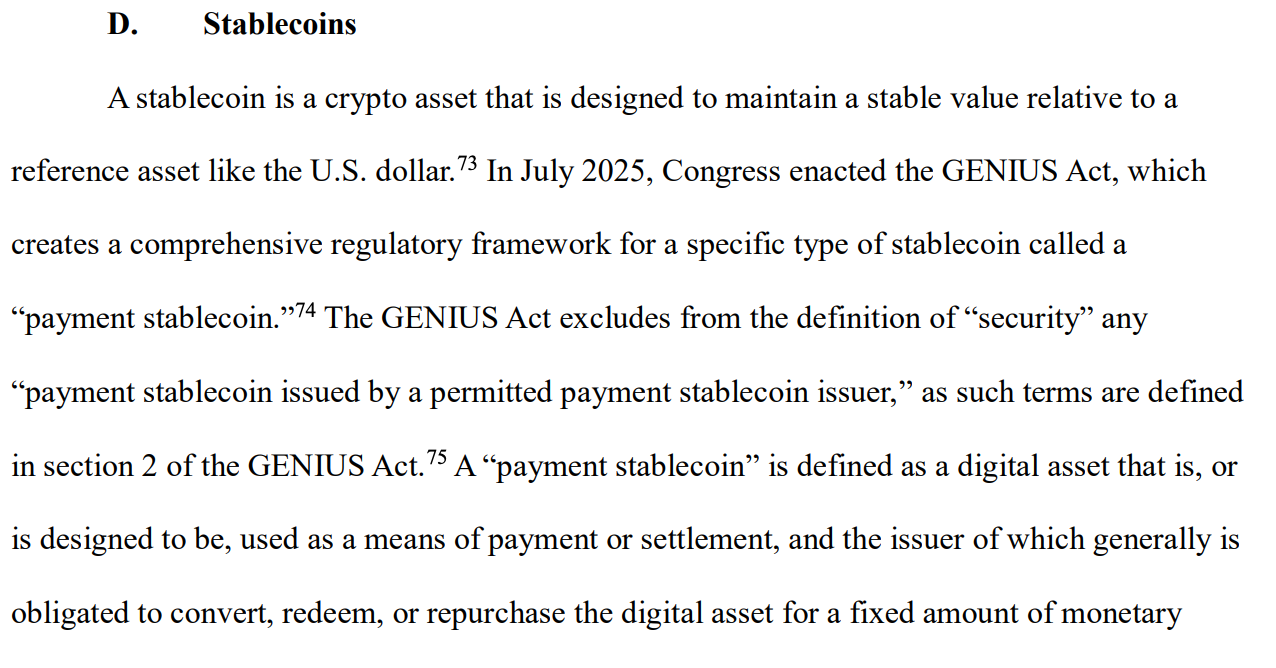

🪙 StablecoinsThe SEC’s interpretative guidance on nonsecurity stablecoins is purposefully concise, bluntly outlining how it will consider payment stablecoins as described by the GENIUS Act as nonsecurities, once it comes into effect this coming January. As such, the SEC itself will not impose registration requirements on GENIUS Act-compliant payment stablecoins for the issuance and redemption process (though the stablecoins themselves will be subject to extensive oversight from other agencies within the U.S. regulatory apparatus). Until the GENIUS Act comes into effect, however, the guidance clarifies that previously defined “Covered Stablecoins” remain considered nonsecurities outside the agency’s purview. For a stablecoin to meet this definition, its holder cannot be entitled to “receive any interest, profit, or other returns,” and its reserves must be entirely composed of “USD and/or other assets that are considered low-risk and readily liquid.” Although the SEC does not define which stablecoins it considers non-securities, dollar-pegged instruments that appear to meet the SEC’s definition of “Covered Stablecoin” include: - PYUSD: a stablecoin issued for PayPal by Paxos Trust Company, a federally registered national trust bank

- USAT: Tether’s latest dollar-pegged stablecoin, specifically designed to comply with the GENIUS Act

- USDC: a stablecoin issued by Circle, overcollateralized 1:1 by dollars and risk-free dollar investments

- KlarnaUSD: a stablecoin sponsored by buy-now-pay-later behemoth Klarna and issued by Stripe’s Bridge

🏦 Digital SecuritiesIt’s fair to say the SEC’s most consequential guidance is its most ambiguous. The regulator remains adamant that any digital assets which fail the Howey test are considered securities, a determination that has historically involved an arduous legal contest. The SEC also considers wrapped versions of instruments that already have clarity as securities under federal law – such as tokenized money market funds, stocks, and other types of structured investments – as digital securities. However, that is not to say that all “wrapped” tokens are securities. The SEC’s guidance explains that protocol mining, protocol staking, and the “wrapping” of a nonsecurity crypto asset does not involve the offer and sale of a security. It further clarifies that "certain" airdrops do not involve an “investment of money” under the Howey test. But still, it remains impossible for the agency to provide a straightforward answer for when digital assets become digital securities. In every instance, the unique fact and circumstances regarding how an issuer marketed and promoted their assets matter in determining whether an investment contract (security) was offered or sold. Non-security crypto assets become securities if offered via an investment contract that satisfies the conditions of Howey. Additionally, just because a non-security crypto asset was initially offered via an investment contract does not make it a security in perpetuity; crypto assets can become non-securities once an original investment contract is fulfilled or the issuer fails to fulfill the efforts they promised to undertake. While the SEC declines to provide examples of assets it considers securities, its guidance notably classifies XRP as a nonsecurity “digital commodity,” despite a final court determination that certain sales of the token were made as investment contracts in violation of federal securities law. Though a step toward regulatory clarity, this aspect of the SEC’s guidance ultimately reinforces rather than resolves ambiguity, merely extending existing federal securities law to digital assets while simultaneously raising renewed concerns for any projects making promises regarding unfinished work or future utility. Digital commodities, digital collectibles, digital tools, and stablecoins may be nonsecurities by nature, yet, they can still be offered or sold through an investment contract, which would subject issuers to federal securities law. FRIEND & SPONSOR: MEGAETH We're past "in it for the tech" or "in it for the money." MegaETH is bringing you products worth using, powered by USDM. |

No comments:

Post a Comment