TBL Weekly #176: Interest Rates Don't Care About Oil AnymoreAnalysis on the relationship between oil and interest rates, and our latest episode on bitcoin's potential price bottom.

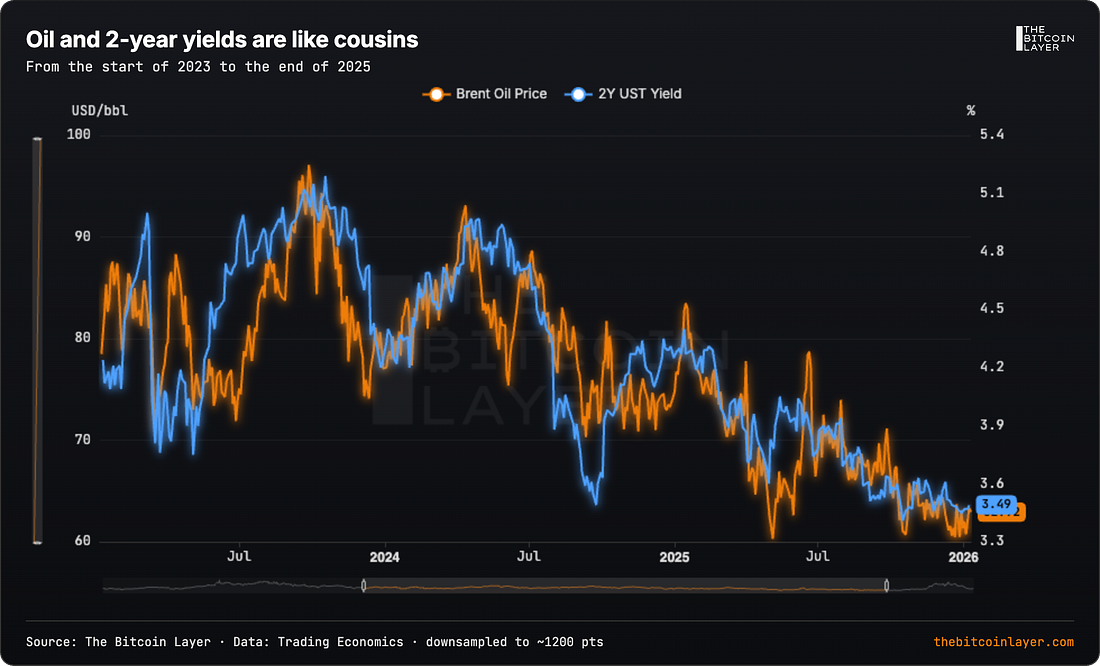

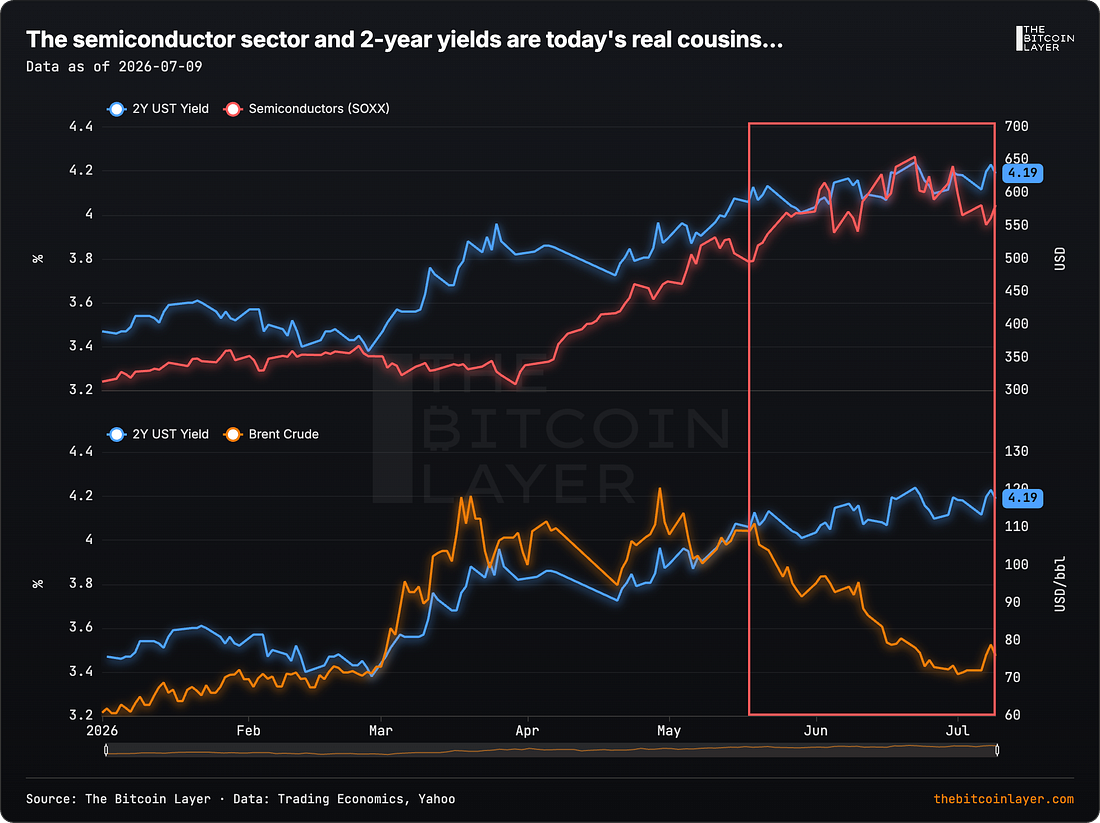

Dear Readers, Before we get started, note that all the charts within this article were created using our MCP server, which anyone can connect to. Historically, Brent crude and 2-year yields move almost in tandem; just take a look at both of these assets from 2023-2026:

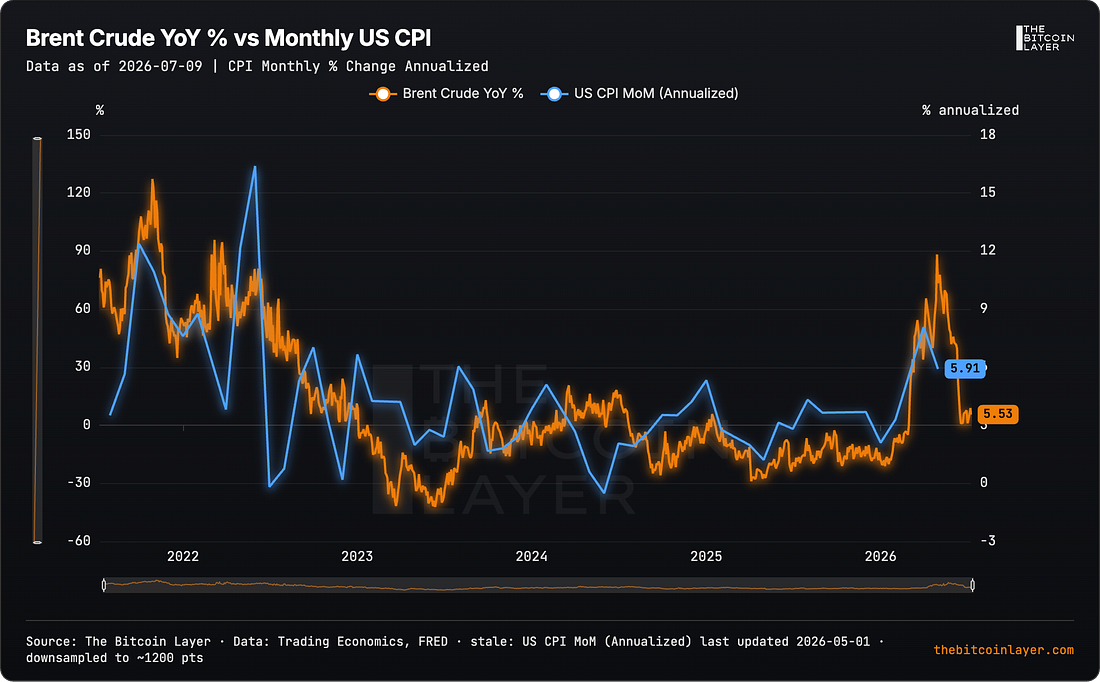

This makes sense given oil’s near one-to-one relationship with inflation:

What’s interesting to note, however, is what has taken place since mid-May:

When the Strait of Hormuz issues began back in February, the relationship continued to hold: higher oil prices —> higher 2-year yield. However, as war tensions began to ease (though they seem to be rising again now that the World Cup fever is behind most countries), so did the relationship between oil and yields. That is, oil fell, but yields held their ground. Article brought to you by:

Open a new health savings account or transfer from an existing HSA. Use code TBL to waive the $50 setup fee. Learn more at SOUNDHSA.com Article brought to you by:

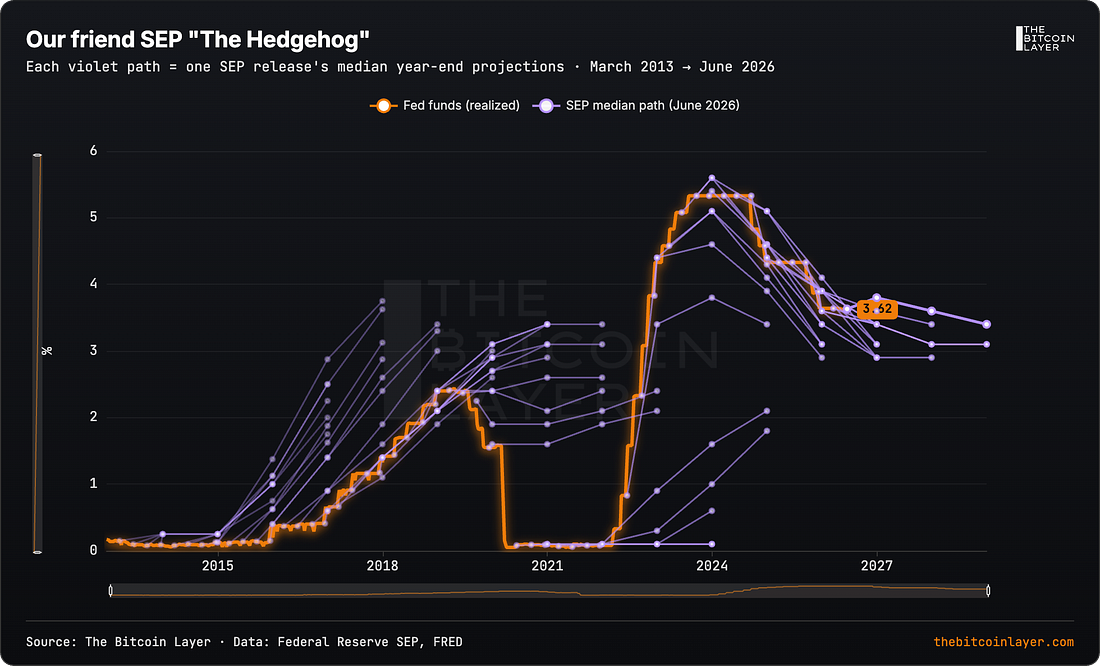

Bitcoin isn’t just an asset. It’s a community. Join 20,000+ Bitcoiners across 71 countries on Club Orange to meet local Bitcoiners, discover events, find bitcoin-friendly merchants, and grow your network. I have a strong feeling this is the market putting TBL narratives on display. With oil no longer having influence on the most Fed-sensitive coupon, something bigger is clearly at play, and the latest FOMC minutes provide some guidance. Before we go into Fed expectations, however, I would like to note an important caveat, which my friend, SEP The Hedgehog, will help me demonstrate (if you didn’t get it, SEP is short for the Fed’s Summary of Economic Projections):

As you can see from our hedgehog, the Fed isn’t very good at projecting its own future policy rates (i.e., they drive using the rearview mirror), which adds credence to Warsh’s questioning of why we have a dotplot at all. The Fed constantly overshoots and undershoots on its own policy expectations. That’s the caveat. No matter what the Fed tells you, forward guidance should never be held as gospel. Caveat aside, the latest FOMC minutes are less about us trying to gauge where the Fed will set interest rates going forward (which the hedgehog shows would be a futile effort), and more about whether our larger narratives are seeping into markets (which they are); thereby explaining why yields are not coming down with a weakening Brent. To keep it nice and short, here’s a great summary of AI’s part in the latest FOMC minutes from Ed Yardeni’s latest piece:

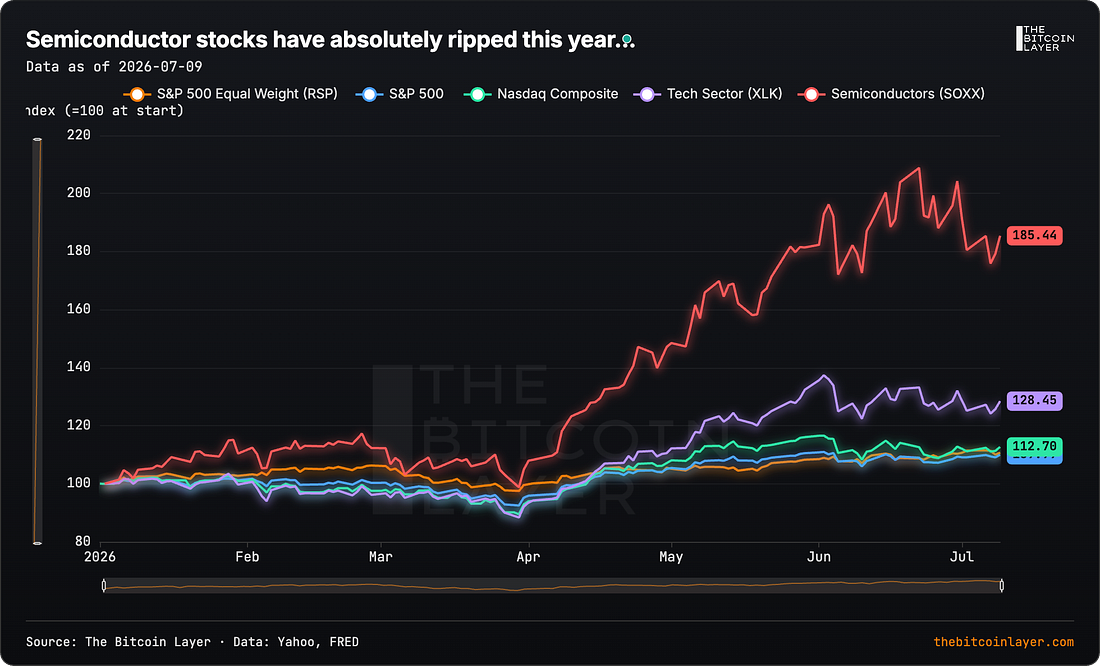

Further, semiconductor and tech investors continue to bolster returns in their respective sectors, leaving traditional indices biting even more dust this year:

In fact, if you’re watching Brent crude to get some signal on yields, you might be looking in the wrong place. A semiconductor index might be a better option:

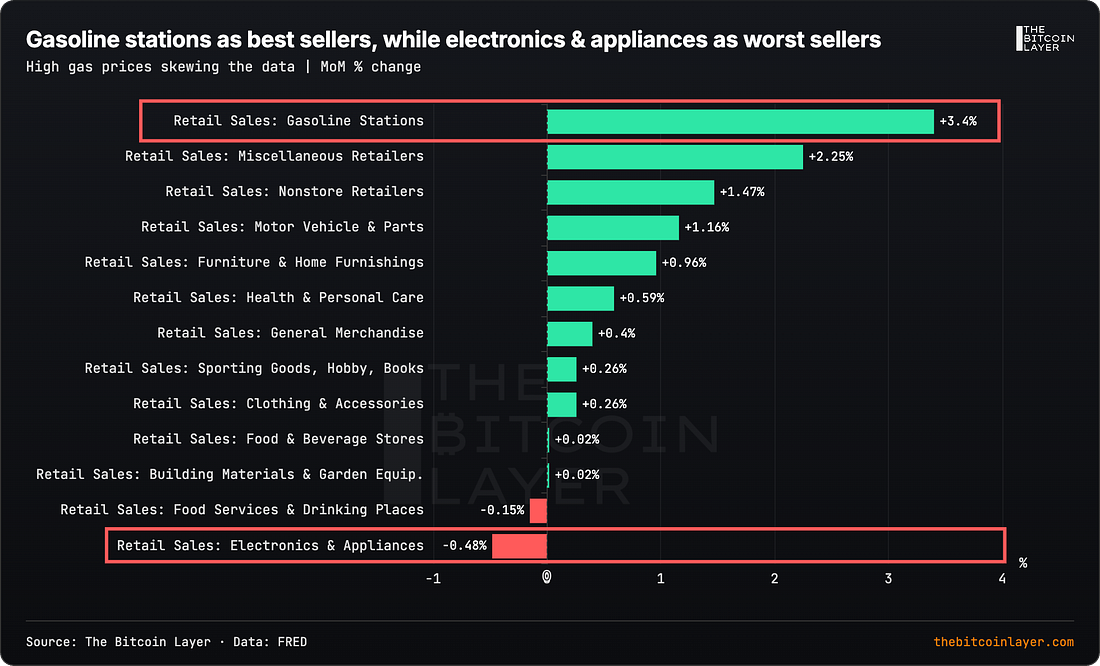

Put differently, US Treasuries are reacting to an economic outlook. Demand for tech is evident in consumers. Yes, the latest retail sales print in the US showed gasoline and electronics spending on opposite ends of the spectrum, given oil’s price spike from the war:

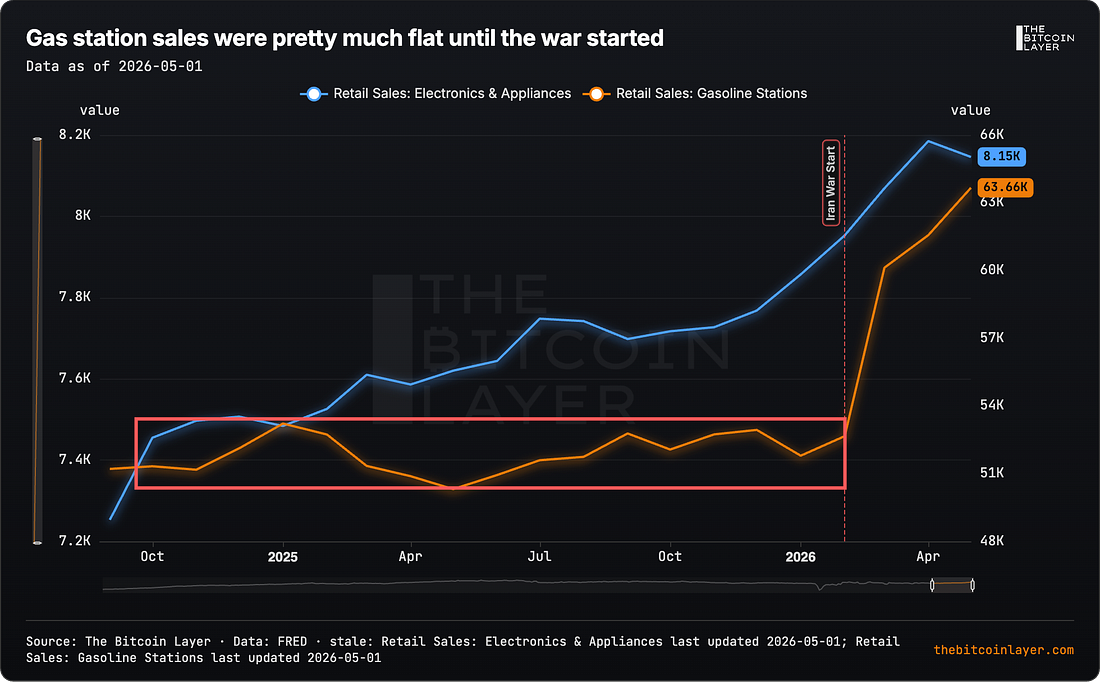

But gas station sales were pretty much flat prior to the war, which explains the sudden climb in the retail sales rankings:

Warsh wants the market to come to their own conclusions on where interest rates should go, right? Well, this is what the market is telling us:

But don’t let that fool you into believing that a major sell-off of USTs is underway given expectations of continued growth. After all, tax refunds from the One Big Beautiful Bill, as well as World Cup consumption, are somewhat behind us now, which may reflect on the data during 2H26. So, our base case is that yields at the 4% handle continue to be home sweet home:

You can also get access to our charts and data inside our TBL Pulse Dashboard:

Substack This Week

YouTube This Week

For Podcast ListenersHere are the links to our latest episode: SPOTIFY

APPLE

Our videos are on major podcast platforms—take us with you on the go! Keep up with The Bitcoin Layer by following our social media! Disclaimer The TBL Model Portfolio, TBL Liquidity Indicator, and all TBL research outputs reflect Nik Bhatia and team’s analytical positioning for the macro and bitcoin environment. They are published for educational purposes only and are not investment advice, not a solicitation to buy or sell securities, and not a recommendation tailored to any individual’s portfolio. The Bitcoin Layer is not a registered investment advisor and does not manage client money. Please consult a professional financial advisor and conduct independent due diligence before making investment decisions. Thanks for reading The Bitcoin Layer — for access to all content, upgrade to paid!

|

Saturday, July 11, 2026

TBL Weekly #176: Interest Rates Don't Care About Oil Anymore

Subscribe to:

Post Comments (Atom)

Popular Posts

-

Reflecting on bitcoin's setup for the second half of 2026, feeding off bearishness, Liquidity analysis and segmentation, and Big Tech...

-

Check out our new ticket experience ...

-

Your monthly read on Bitcoin’s cycle, from macro to flows. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ...

-

Lower leverage, modest yields, and a market that quietly gave up on faces getting ripped ͏ ͏ ͏ ͏ ͏ ͏ ͏ ...

-

A summary of TBL content from this week ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ...

No comments:

Post a Comment