Article brought to you by:

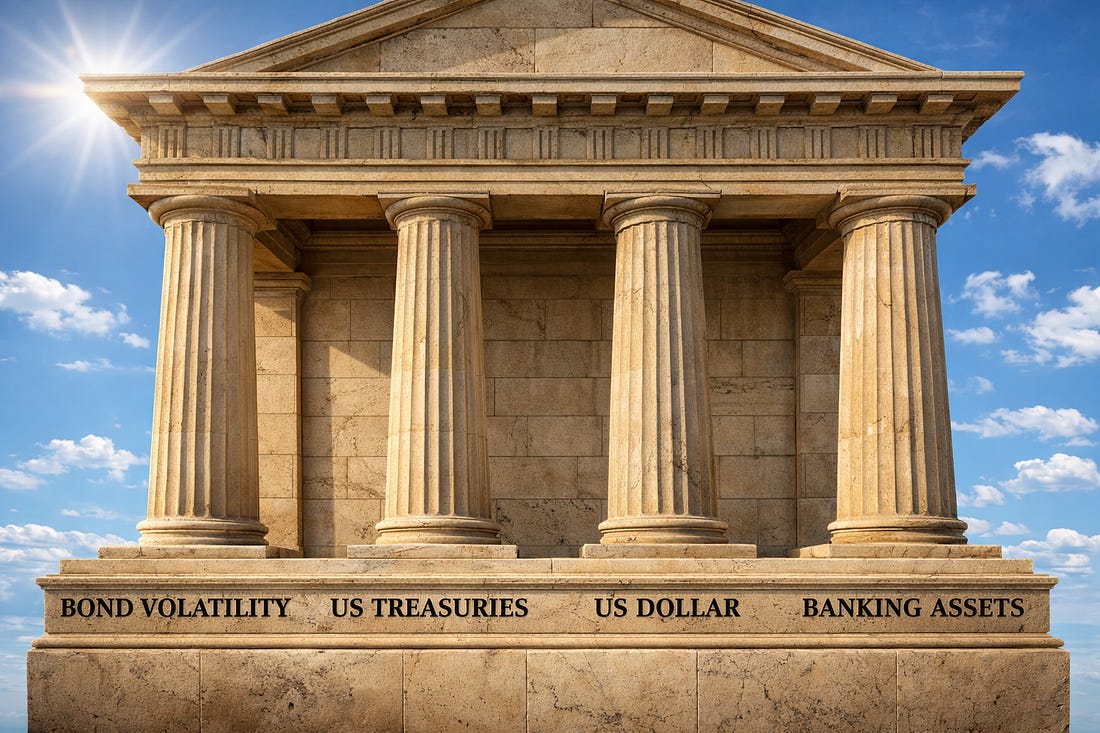

Dear Readers, Before we start, thank you. Last week we sent out some surveys, and through that process we learned a lot about what adds value to your daily lives, and what doesn’t. We are internalizing your feedback, so today I want to write something that I probably should have written months ago. We have a lot of new readers, while most of you have been here for a while. Some read the macro sections and skip past the Indicator updates, while others may have even read the words, “sell signal confirmed January 14” in a recent letter but didn’t fully understand what that meant and kept scrolling. And some of you understood it perfectly, but didn’t have your alerts turned on. In summary, we received your message that you don’t really know how to use this indicator. TBL Liquidity is the analytical engine of this entire research operation and something that separates what we do from every other bitcoin newsletter. But if we build high quality signal and then fail to make sure every single reader knows how to use it, the signal doesn’t matter. Let’s fix that. What TBL Liquidity Actually MeasuresLet me start with what it is not. TBL Liquidity is not market liquidity in the trading-volume sense. It is also not measuring how easy it is to buy or sell bitcoin on an exchange. It is not a sentiment indicator, nor a price prediction model. TBL Liquidity measures the global financial system’s capacity and willingness to extend credit at scale. That sentence is doing a lot of work, so let me unpack it. Every risk asset in the world (stocks, corporate bonds, real estate, and yes, bitcoin) trades inside a credit environment. When the system is expanding credit freely, money flows into risk assets. When the system is contracting credit or becoming unwilling to lend, money flows out. This is not a theory but a mechanical reality of how a $348 trillion global debt system operates. ($348 trillion!! For those really paying attention, you’ll know this is a new fresh high.) The question we are answering with TBL Liquidity is: today…is the global credit machine expanding or contracting? And what does that tell us about where risk assets are headed? The Four PillarsWe measure global credit conditions through four inputs. Let’s start calling them The Four Pillars to enhance the understanding.

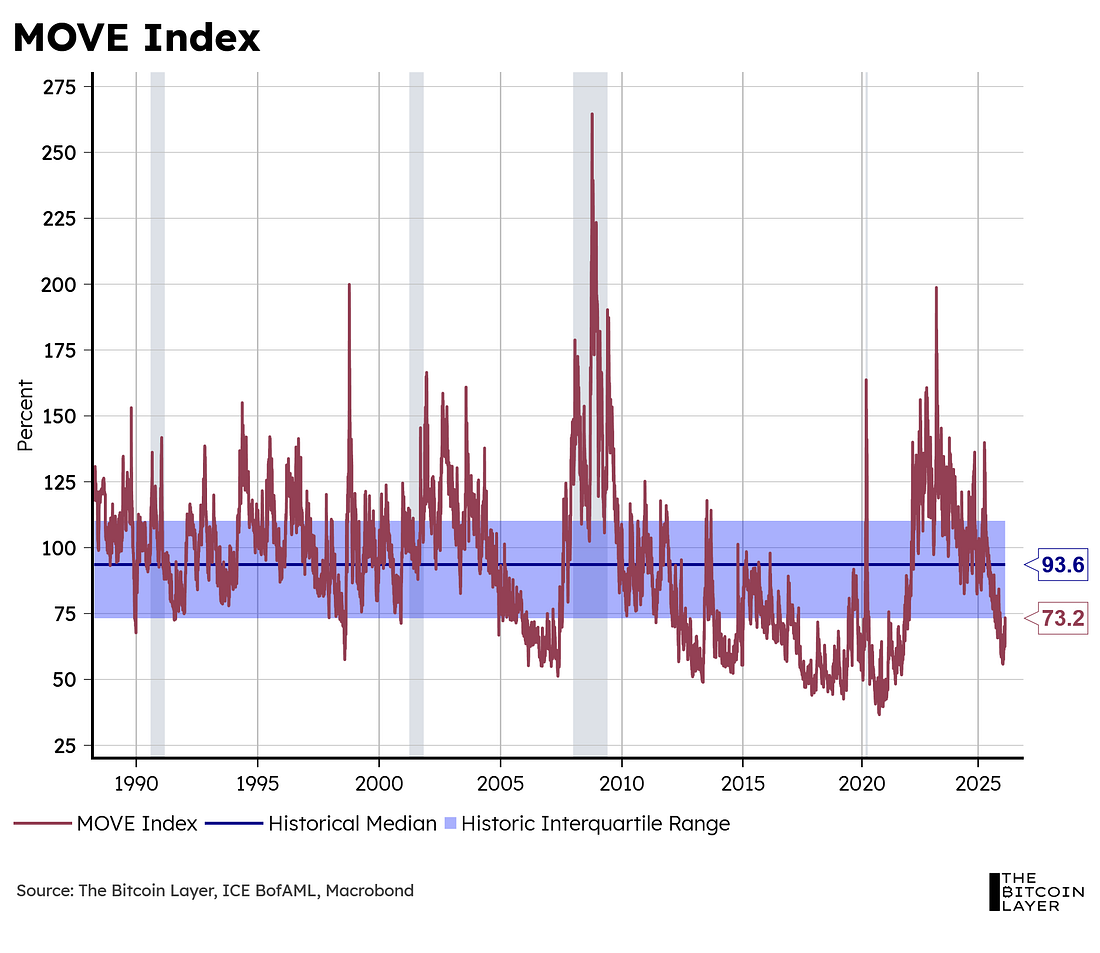

I want to walk through each one, because understanding the pillars is the difference between trusting the signal blindly and actually knowing why it is telling you what it is telling you. The MOVE Index (bond market volatility). This is the one most people skip over, but it is arguably the most important early warning system in the entire framework. MOVE measures volatility in the Treasury market. When Treasuries are volatile, the collateral that underpins the entire overnight lending system becomes unstable. MOVE itself is a calculation based on options pricing. Thinking in terms of calls and puts can make it more confusing than it actually is, so let’s just focus on puts. Puts are options that protect an investor from downside. Pay a premium and receive a put option, and you now have the option to PUT your long position to the option seller. It becomes your choice whether or not you get to hand over the security for an agreed upon price, and once the market price has fallen far enough, every rational investor EXERCISES their put option. In Treasuries, investors buy puts to guard against rising rates. If you own a put option, rising rates don’t matter because you can just hand over your position. At what price depends on your necessity for said insurance, but all in all a put option allows you to cap your losses as rates rise. When rates might rise (and in this case the duality of the fact that in a sudden flight-to-safety rates might plummet as well), options become more expensive. Put options have become much more expensive during this war, for example, as the threat of spiking oil prices threatens global inflation higher. As volatility spikes, banks pull back their market making, or their willingness to sell put options to investors looking for protection. The entire cost to hedge gets more expensive market-wide, and everything catches a cold. If you are watching one thing between letters, watch MOVE. It moves fast. Sorry, couldn’t help it.

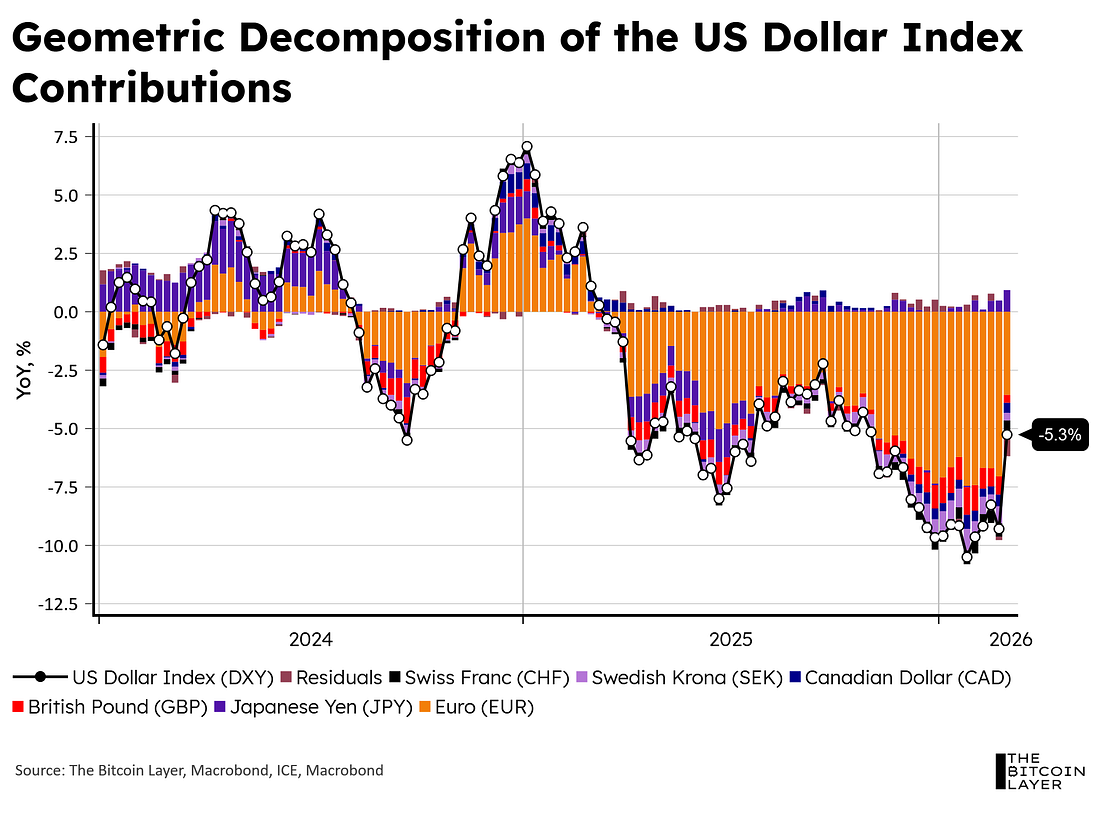

The US Dollar Index (DXY). The vast majority of global debt is denominated in US dollars. When the dollar strengthens, every borrower outside the United States effectively sees their debt burden increase, meaning global credit tightens. When the dollar weakens, the opposite happens: the system breathes easier, credit flows more freely, and risk appetite improves. DXY is also a fast mover and tends to dictate market sentiment in real time, particularly through EUR/USD, which makes up roughly 58% of the index’s weighting. The dollar is the single most important variable in the framework over a longer time horizon, although I would argue that what dominates risk price action can rotate between volatility, rates, the dollar, and banking assets depending on what type of regime markets trade. Part of what we do best is track those regime shifts really well because we are intraday chart watchers and long-term chart watchers simultaneously. It’s part of my practice as a former fixed income markets practitioner. Here’s a snapshot at how the DXY is composed.

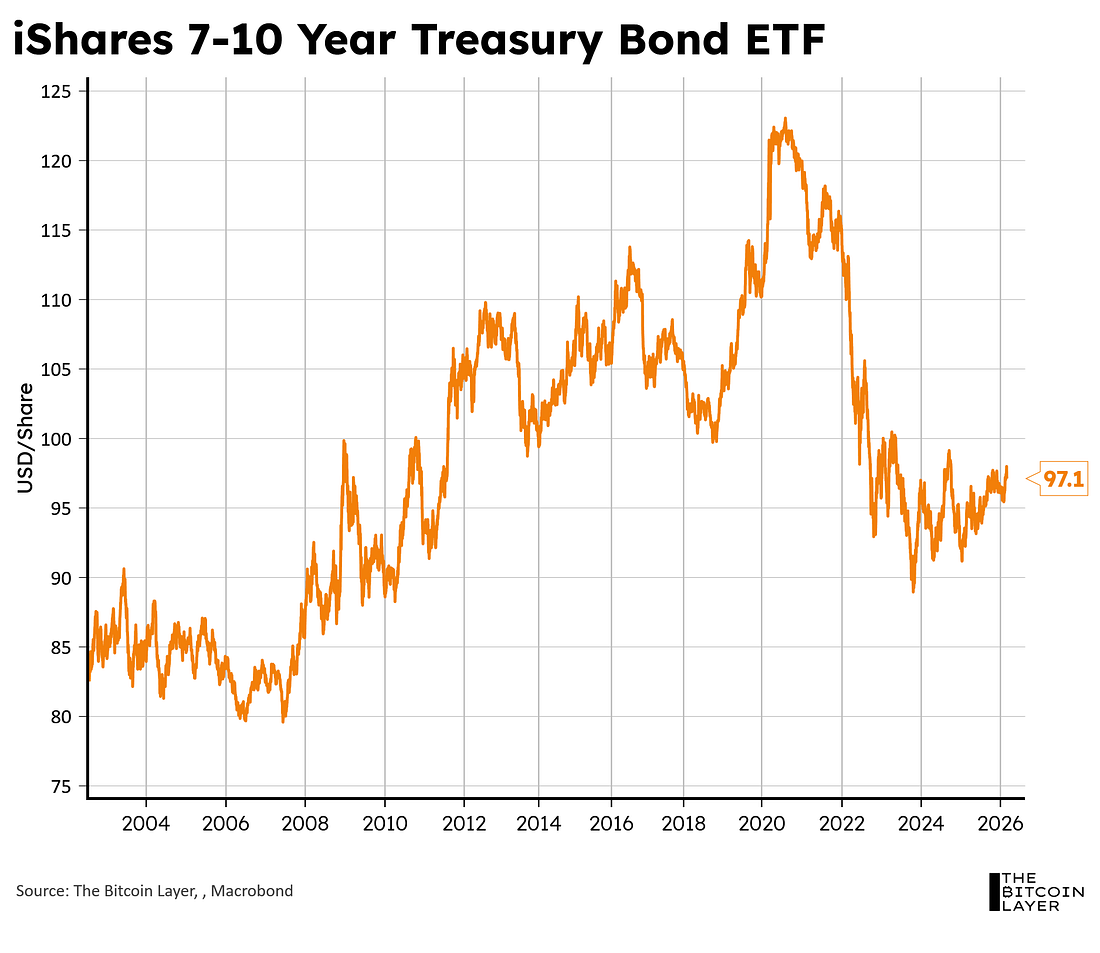

The 7-10 Year Treasury ETF (IEF). This is measuring what Treasury prices are doing, which tells us what interest rates are doing, which tells us what the cost of capital looks like across the entire economy. When Treasury prices rise (yields fall), risk appetite tends to improve. When Treasury prices fall (yields rise), duration risk increases, and credit conditions tighten at the margin. But it’s not just the cost of capital that matters when it comes to Treasury prices. Treasuries are the underlying collateral of the system, and therefore falling Treasury prices damage the entire financial industry’s ability to finance and borrow at the margin. In turn, the entire system suffers a drop in supportive conditions.

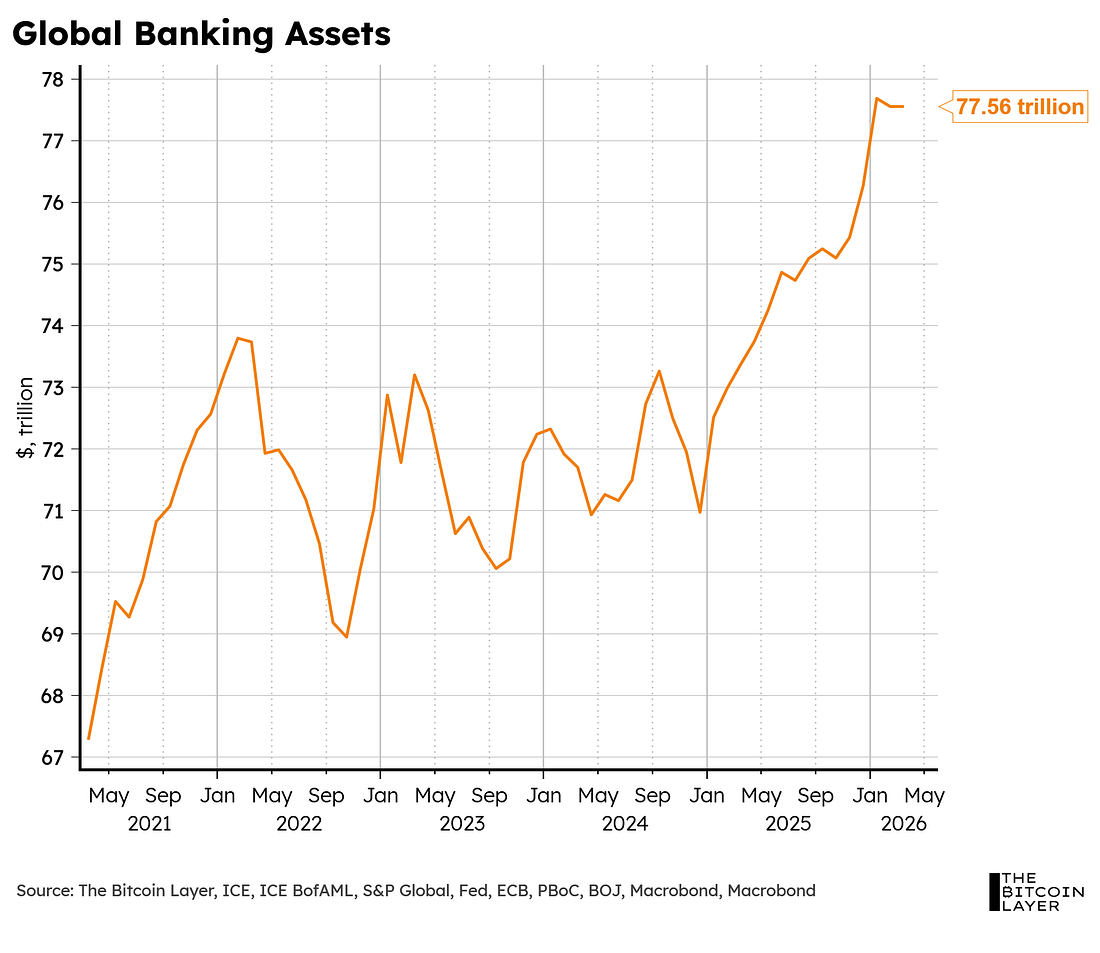

Global banking assets (ex-China). The aggregate balance sheets of major central and commercial banks (the Fed, ECB, BOJ, and associated commercial banking systems). When these balance sheets expand, the system is easing; when they contract, it is tightening. We exclude China because its financial system is mostly closed off from the global credit cycle, and including it introduces more noise than signal. We are, however, conducting a deeper study on optimal ways to measure global banking assets (what to include, what not to include). This was a proprietary judgement we made based on correlations with risk markets.

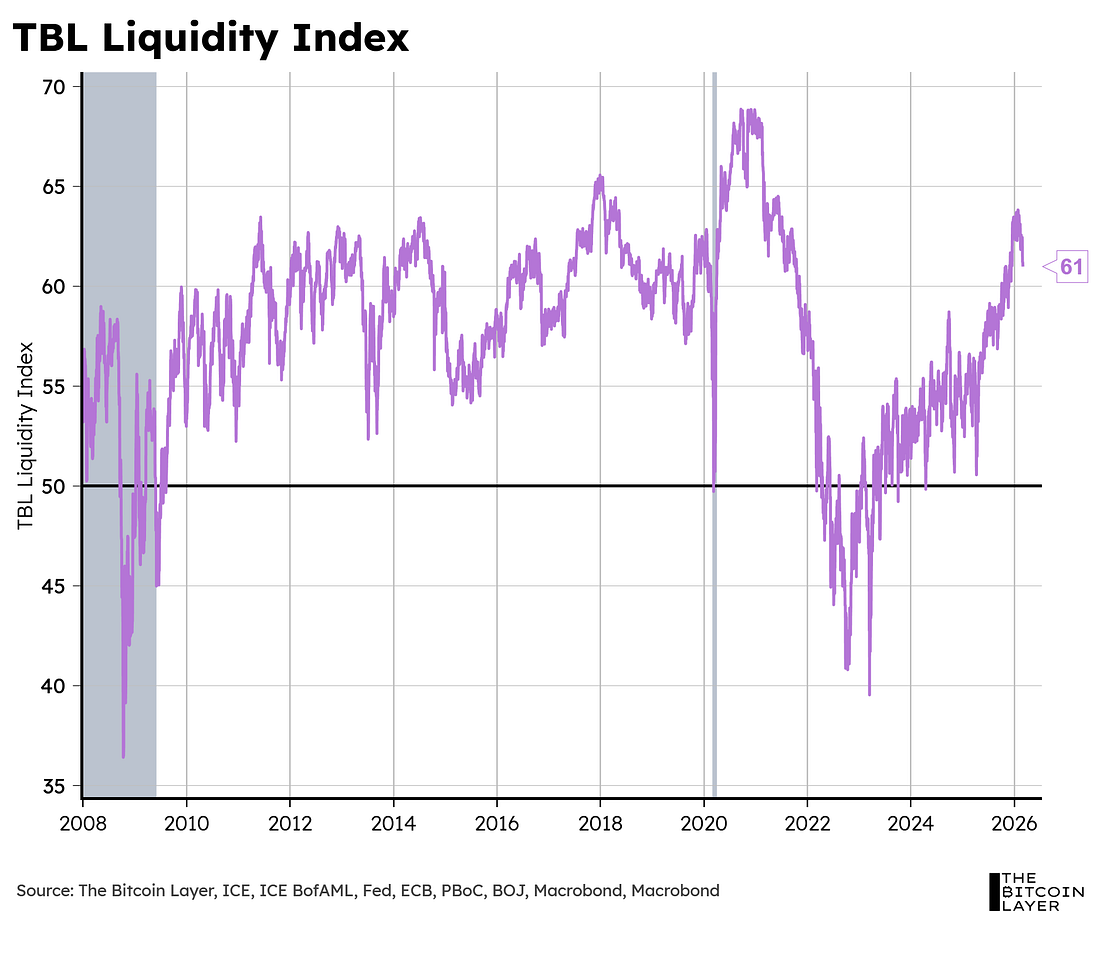

Four pillars, each one connected to the real plumbing of global credit. The Three Tools: Index, Indicator, WaveHere is where readers get lost, so let’s break it down clearly what TBL is trying to provide. We have built three distinct tools from the same underlying framework. They answer different questions and operate on different time horizons. Using one when you need another is like checking the weather forecast for next week when you need to know if it is raining right now. Tool 1: The TBL Liquidity Index. This is the broadest measure. It produces a value that tells you whether global credit conditions are in expansion or contraction. Values above 50 have historically shown expansion, while those below 50 align with major contraction periods. Over a trailing three-year period, the Index shows roughly 80% correlation with both bitcoin and the S&P 500. That is not a backtest we are cherry-picking. It is the validated, published relationship between global credit conditions and risk asset returns. The Index tells you the environment you are operating in.

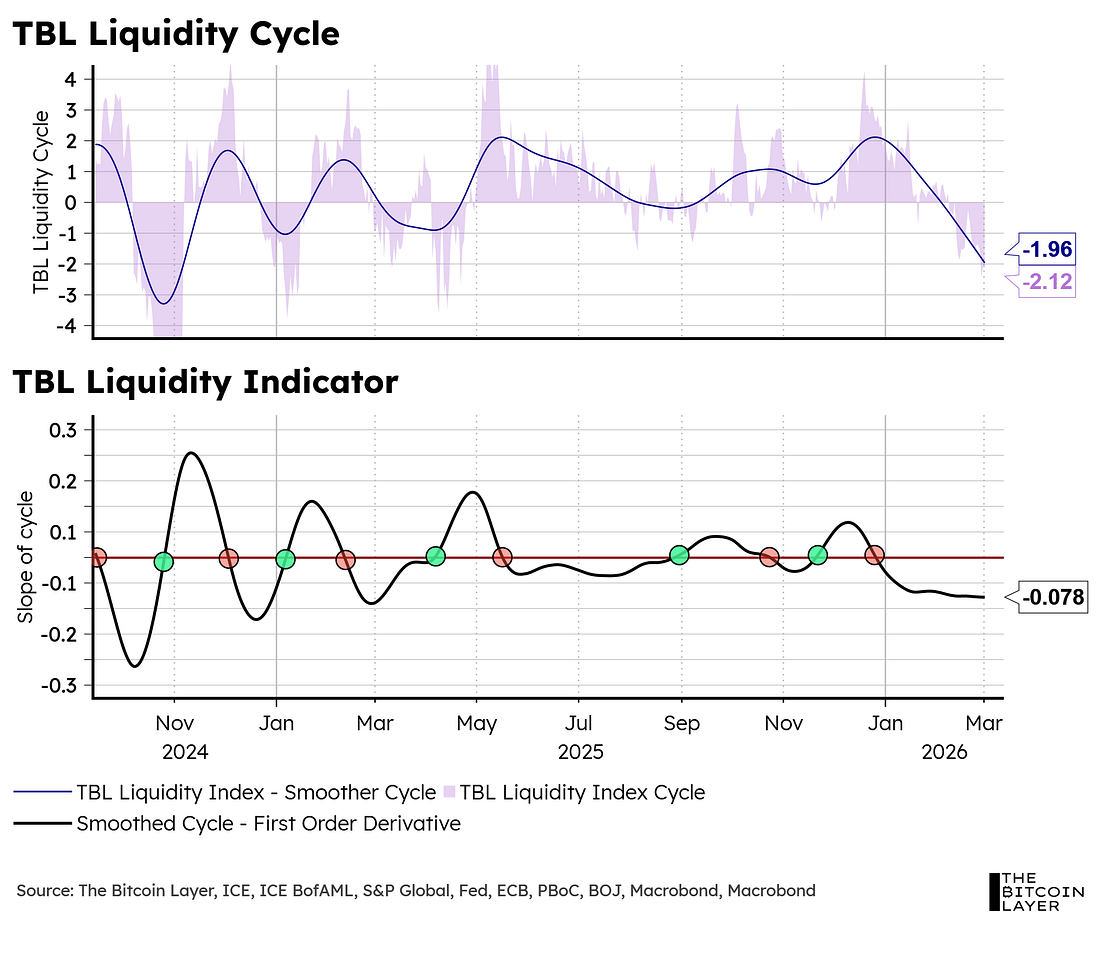

Tool 2: The TBL Liquidity Indicator. This is the signal. It is built from the first-order derivative of the TBL Liquidity Cycle, which is our way to measure the rate of change of our Index. In plain language, it measures the slope of the credit cycle. In even more plain language, our TBL Liquidity Indicator is how we score liquidity. Above zero is short-term supportive, below zero is short-term punitive. We developed this Indicator to help allocators: is now a good time or a bad time to buy bitcoin? That’s the question we try to answer. When that slope crosses above zero, meaning credit conditions are improving, the Indicator flashes a 🟢 green dot: liquidity is working as a tailwind for risk (a buy signal from a liquidity-only perspective). When it crosses below zero, meaning conditions are deteriorating, it flashes a 🔴 red dot: liquidity is working as a headwind for risk (a sell signal from a liquidity-only perspective).

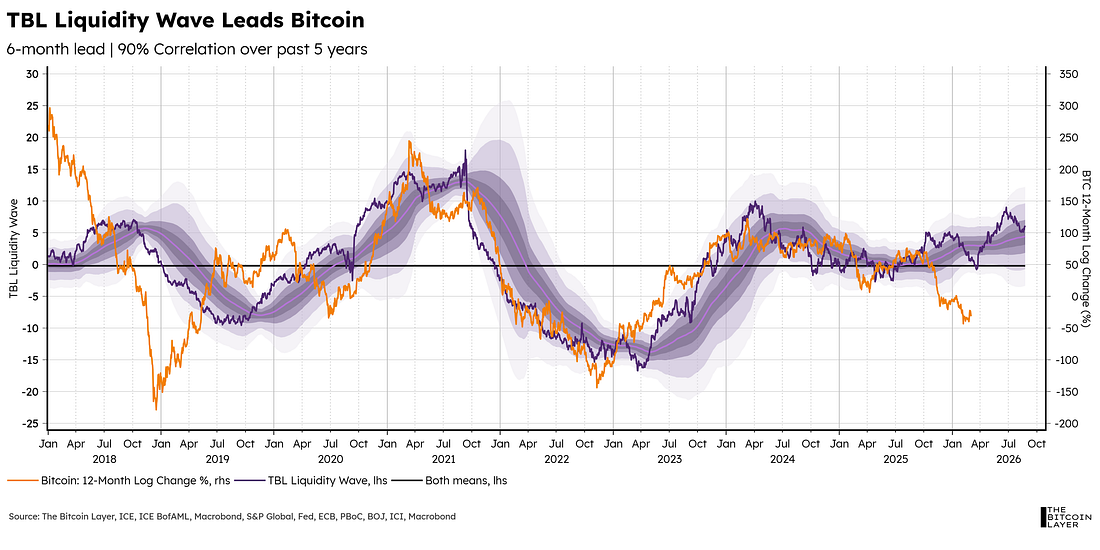

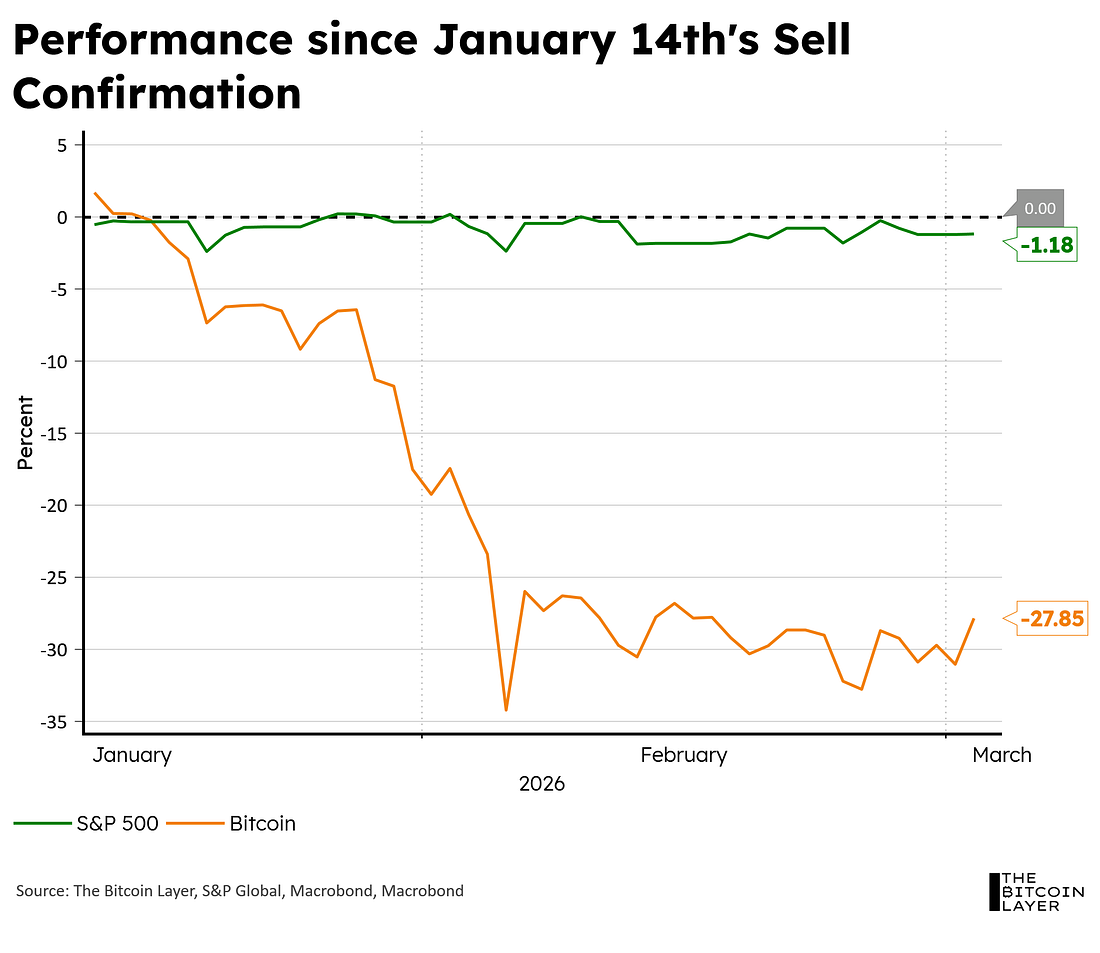

The active strategy using TBL Liquidity Indicator, which is long bitcoin on green dots and move into Treasury bills on red dots, has outperformed buy-and-hold bitcoin on one-to-three year time horizons. Our most recent 🔴 red dot on January 14th preceded bitcoin falling by 35%, but until the next 🟢 green dot triggers, we can’t celebrate anything as we don’t close the books on the Treasury bill holding in the active strategy. Interestingly, this active strategy does not outperform on five-to-seven-year horizons, and that makes sense. The Indicator is not trying to beat long-term holding. It is trying to help you avoid the worst drawdowns within a cycle. If you are managing risk within a cycle, the Indicator is the tool. Tool 3: The TBL Liquidity Wave. This is the forecast. It uses a six-month lead structure and shows roughly 90% correlation with bitcoin’s subsequent twelve-month returns over a five-year lookback. The Wave gives you confidence bands for where bitcoin is likely headed based on the current trajectory of the credit cycle. It does not tell you what to do today. It tells you what the next six to twelve months look like if credit conditions follow their current path. Banking assets are used more prominently in this Wave formulation, although the six-month lead time is inconsistent. We’re working on deriving more signal from this alternate formulation!

How the Signal Actually Works in PracticeI want to be very concrete here because this is where the gap between our communication and your experience has been widest. On December 25, 2025, we flagged a change in the Indicator’s trajectory. On January 14, 2026, we confirmed the sell signal, with bitcoin trading above $90,000. Bitcoin subsequently fell roughly 35%.

If you were a TBL Pro subscriber with your Dashboard account email alerts turned on, you received that signal in real time. You had the information to act. If you were reading the letters, you saw references to the sell signal. But I will be honest with you, in some of those January and February letters, the structural bull case for bitcoin was carrying too much weight relative to what the Indicator was actually saying. The structural case for bitcoin is always true, even though the price cycles up and down. Bitcoin as a Layer 1 monetary asset in a world of $348 trillion in debt and $620 trillion in real wealth — that thesis does not change with price. But the timing case is what the Indicator provides, and during sell signal periods, the Indicator’s voice needs to be the loudest voice in the room. In some letters, it was not. That is a calibration we have corrected, and it is part of why I am writing this today. The Cyclical GuaranteeHere is the most important thing I can tell you about the Indicator, and it is the thing that provides genuine reassurance during periods like this one: the Indicator is mathematically guaranteed to turn. It is a cyclical tool measuring the slope of a cycle. Based on the historical frequency of signal changes, sell-to-buy transitions should not take more than a few months. I cannot tell you the exact date. I can tell you it will happen, and when it does, TBL Pro subscribers will receive the alert the day it fires, whether or not they are actively using the Dashboard. What You Should Do With ThisIf you are a free trial reader, here is what I want you to take away: The TBL Liquidity framework is the analytical foundation underneath everything we publish. When I write about the dollar, about rates, about the production economy, about bitcoin’s price action, our framework is what connects all of it. If you want access to the Dashboard, the daily recalculation, and the email alerts, I’d encourage you to use our Dashboard: What I can promise you is that we will never bury a signal change in paragraph nine of a macro letter again. Until next time, Nik Thanks for reading The Bitcoin Layer — for access to all content, upgrade to paid!

|

Tuesday, March 3, 2026

How Do I Actually Use TBL Liquidity?

Subscribe to:

Post Comments (Atom)

Popular Posts

-

Bitcoin Correlations Report, June 2026 ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ...

-

Dynamic trend levels are coming down, but the bear-market work is not finished yet. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏...

-

A Flash TBL Liquidity Indicator Update ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ...

-

Bitcoin Momentum Report, June 2026 ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏...

-

Weekly Recap: Base may be the dominant Ethereum L2 now, but it's got new promising competition in Kraken's Ink. ...

No comments:

Post a Comment